America Online 2015 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2015 America Online annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

and equity of a group of guideline companies as of the valuation

date. Accordingly, our discount rate incorporated our estimate of

the expected return a marketplace participant would have required

as of the valuation date, including the risk premium associated with

the current and expected economic conditions as of the valuation

date. The terminal value growth rate represented our estimate of the

marketplace’s long-term growth rate.

In 2014 and 2013, we performed a qualitative impairment assess-

ment to determine whether it is more likely than not that the fair

value of our wireless licenses was less than the carrying amount. As

part of our assessment we considered several qualitative factors

including the business enterprise value of Wireless, macroeconomic

conditions (including changes in interest rates and discount rates),

industry and market considerations (including industry revenue and

EBITDA margin projections), the projected financial performance of

Wireless, as well as other factors. Based on our assessment in 2014

and 2013, we qualitatively concluded that it was more likely than not

that the fair value of our wireless licenses significantly exceeded

their carrying value and therefore, did not result in an impairment.

Goodwill

At December31, 2015, the balance of our goodwill was approx-

imately $25.3billion, of which $18.4billion was in our Wireless

reporting unit, $4.3billion was in our Wireline reporting unit and

$2.6billion was in our other reporting unit. Determining whether an

impairment has occurred requires the determination of fair value of

each respective reporting unit. The fair value of our reporting units

exceeded the carrying values. Accordingly, our annual impairment

tests for 2015, 2014 and 2013 did not result in an impairment. In

the event of a 10% decline in the fair value of any of our reporting

units, the fair value would have still exceeded the book value of the

reporting unit and no impairment charge would be recorded.

The fair value of the reporting unit is calculated using a market

approach and a discounted cash flow method. The market

approach includes the use of comparative multiples to corroborate

discounted cash flow results. The discounted cash flow method

is based on the present value of two components — projected

cash flows and a terminal value. The terminal value represents the

expected normalized future cash flows of the reporting unit beyond

the cash flows from the discrete projection period. The fair value

of the reporting unit is calculated based on the sum of the present

value of the cash flows from the discrete period and the present

value of the terminal value. The discount rate represented our

estimate of the WACC, or expected return, that a marketplace par-

ticipant would have required as of the valuation date.

• We maintain benefit plans for most of our employees, including, for

certain employees, pension and other postretirement benefit plans.

At December31, 2015, in the aggregate, pension plan benefit obliga-

tions exceeded the fair value of pension plan assets, which will result

in higher future pension plan expense. Other postretirement benefit

plans have larger benefit obligations than plan assets, resulting

in expense. Significant benefit plan assumptions, including the

discount rate used, the long-term rate of return on plan assets, the

determination of the substantive plan and health care trend rates are

periodically updated and impact the amount of benefit plan income,

expense, assets and obligations. Changes to one or more of these

assumptions could significantly impact our accounting for pension

and other postretirement benefits. A sensitivity analysis of the

impact of changes in these assumptions on the benefit obligations

and expense (income) recorded, as well as on the funded status due

to an increase or a decrease in the actual versus expected return on

plan assets as of December31, 2015 and for the year then ended

pertaining to Verizon’s pension and postretirement benefit plans is

provided in the table below.

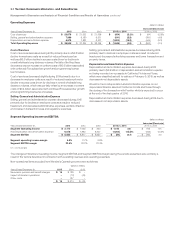

(dollars in millions)

Percentage

point

change

Increase

(decrease) at

December31,

2015*

Pension plans discount rate +0.50 $ (1,195)

−0.50 1,333

Rate of return on pension plan assets +1.00 (175)

−1.00 175

Postretirement plans discount rate +0.50 (1,565)

−0.50 1,761

Rate of return on postretirement plan assets +1.00 (21)

−1.00 21

Health care trend rates +1.00 3,074

−1.00 (2,516)

* In determining its pension and other postretirement obligation, the Company used a

weighted- average discount rate of 4.6%. The rate was selected to approximate the

composite interest rates available on a selection of high- quality bonds available in

themarket at December31, 2015. The bonds selected had maturities that coincided

with thetime periods during which benefits payments are expected to occur, were

non- callable and available in sufficient quantities to ensure marketability (at least

$0.3billion par outstanding).

The annual measurement date for both our pension and other

postretirement benefits is December 31st. Effective January1, 2016,

we adopted the full yield curve approach to estimate the interest

cost component of net periodic benefit cost for pension and other

postretirement benefits. We will account for this change as a

change in accounting estimate and, accordingly, will account for

it prospectively beginning in the first quarter of 2016. Prior to this

change, we estimated the interest cost component utilizing a single

weighted- average discount rate derived from the yield curve used to

measure the benefit obligation at the beginning of the period.

The full yield curve approach refines our estimate of interest cost

by applying the individual spot rates from a yield curve composed

of the rates of return on several hundred high- quality, fixed income

corporate bonds available at the measurement date. These indi-

vidual spot rates align with the timing of each future cash outflow for

benefit payments and therefore provide a more precise estimate of

interest cost.

This change in accounting estimate does not affect the measure-

ment of our total benefit obligations at year end or our annual net

periodic benefit cost as the change in the interest cost is offset in

the actuarial gain or loss recorded at year end. Accordingly, this

change in accounting estimate has no impact on our annual con-

solidated GAAP results. We estimate the impact of this change on

our consolidated GAAP results for the first quarter of 2016 will be

a reduction of the interest cost component of net periodic benefit

cost and an increase to Net income by approximately $0.1billion.

However, at this time the estimated impact of this change on the

remaining 2016 interim periods and for annual 2016 results cannot

be reasonably estimated because it is possible that in the future

there may be changes to underlying assumptions, including an

interim remeasurement of our benefit obligations, which could result

in different estimates. Our non-GAAP measure for segment EBITDA

is unaffected because net periodic benefit costs are not included

in our segment results. For additional discussion of Non-GAAP

measures and non- operational items see “Consolidated Results of

Operations”.

33Verizon Communications Inc. and Subsidiaries

Management’s Discussion and Analysis ofFinancialCondition and Results of Operations continued