America Online 2015 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2015 America Online annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

|

|

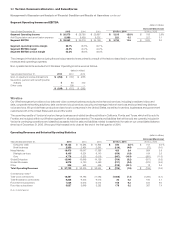

Cross Currency Swaps

Verizon Wireless previously entered into cross currency swaps des-

ignated as cash flow hedges to exchange approximately $1.6billion

of British Pound Sterling and Euro- denominated debt into U.S. dollars

and to fix our future interest and principal payments in U.S. dollars, as

well as to mitigate the impact of foreign currency transaction gains or

losses. In June 2014, we settled $0.8billion of these cross currency

swaps and the gains with respect to these swaps were not material. In

December 2015, we settled $0.6billion of these cross currency swaps

on maturity.

During the first quarter of 2014, we entered into cross currency

swaps designated as cash flow hedges to exchange approximately

$5.4billion of Euro and British Pound Sterling denominated debt into

U.S. dollars. During the second quarter of 2014, we entered into cross

currency swaps designated as cash flow hedges to exchange approx-

imately $1.2billion of British Pound Sterling denominated debt into

U.S. dollars. During the fourth quarter of 2014, we entered into cross

currency swaps designated as cash flow hedges to exchange approxi-

mately $3.0billion of Euro denominated debt into U.S. dollars and to fix

our future interest and principal payments in U.S. dollars. Each of these

cross currency swaps was entered into in order to mitigate the impact

of foreign currency transaction gains or losses.

A portion of the gains and losses recognized in Other comprehensive

income was reclassified to Other income and (expense), net to offset

the related pre-tax foreign currency transaction gain or loss on the

underlying debt obligations. The fair value of the outstanding swaps

was $1.6billion and $0.6billion, which was primarily included within

Other liabilities on our consolidated balance sheets at December31,

2015 and 2014, respectively. At December31, 2015, the total notional

amount of the cross currency swaps was $9.7billion. During 2015

and 2014, a pre-tax loss of $1.2billion and a pre-tax loss of $0.1billion,

respectively, was recognized in Other comprehensive income with

respect to these swaps.

Net Investment Hedges

We entered into foreign currency forward contracts that are des-

ignated as net investment hedges to mitigate foreign exchange

exposure related to non-U.S. dollar net investments in certain foreign

subsidiaries against changes in foreign exchange rates. During

the third quarter of 2015, we entered into net investment hedges

with a total notional value of $0.9billion with the contract tenor

maturing in 2018. The fair value of these contracts was not material at

December31, 2015.

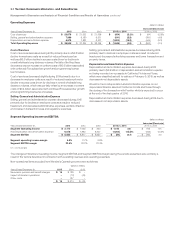

Critical Accounting Estimates and

Recently Issued Accounting Standards

Critical Accounting Estimates

A summary of the critical accounting estimates used in preparing our

financial statements is as follows:

• Wireless licenses and Goodwill are a significant component of

our consolidated assets. Both our wireless licenses and goodwill

are treated as indefinite-lived intangible assets and, therefore are

not amortized, but rather are tested for impairment annually in the

fourth fiscal quarter, unless there are events requiring an earlier

assessment or changes in circumstances during an interim period

that indicate these assets may not be recoverable. We believe our

estimates and assumptions are reasonable and represent appro-

priate marketplace considerations as of the valuation date. Although

we use consistent methodologies in developing the assumptions

and estimates underlying the fair value calculations used in our

impairment tests, these estimates are uncertain by nature and can

vary from actual results. It is possible that in the future there may be

changes in our assumptions, including estimated cash flow projec-

tions, margins, growth rates and discount rate, which could result in

different fair value estimates and an impairment charge.

Wireless Licenses

The carrying value of our wireless licenses was approximately

$86.6billion as of December31, 2015. We aggregate our wireless

licenses into one single unit of accounting, as we utilize our wireless

licenses on an integrated basis as part of our nationwide wireless

network. Our wireless licenses provide us with the exclusive right

to utilize certain radio frequency spectrum to provide wireless

communication services. There are currently no legal, regulatory,

contractual, competitive, economic or other factors that limit the

useful life of our wireless licenses.

In 2015, our quantitative impairment test consisted of comparing the

estimated fair value of our aggregate wireless licenses to the aggre-

gated carrying amount as of the test date. If the estimated fair value

of our aggregated wireless licenses is less than the aggregated

carrying amount of the wireless licenses then an impairment charge

would have been recognized. Our quantitative impairment test for

2015 indicated that the fair value significantly exceeded the carrying

value and, therefore, did not result in an impairment.

In 2015, using a quantitative assessment, we estimated the fair

value of our wireless licenses using the Greenfield approach.

The Greenfield approach is an income based valuation approach

that values the wireless licenses by calculating the cash flow

generating potential of a hypothetical start-up company that goes

into business with no assets except the wireless licenses to be

valued. A discounted cash flow analysis is used to estimate what

a marketplace participant would be willing to pay to purchase

the aggregated wireless licenses as of the valuation date. As a

result, we were required to make significant estimates about future

cash flows specifically associated with our wireless licenses, an

appropriate discount rate based on the risk associated with those

estimated cash flows and assumed terminal value and growth rates.

We considered current and expected future economic conditions,

current and expected availability of wireless network technology

and infrastructure and related equipment and the costs thereof as

well as other relevant factors in estimating future cash flows. The

discount rate represented our estimate of the weighted- average

cost of capital (WACC), or expected return, that a marketplace par-

ticipant would have required as of the valuation date. We developed

the discount rate based on our consideration of the cost of debt

32 Verizon Communications Inc. and Subsidiaries

Management’s Discussion and Analysis ofFinancialCondition and Results of Operations continued