Cabela's 2007 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2007 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

38

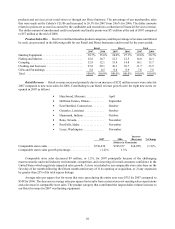

The quality of our managed credit card loan portfolio at any time reflects, among other factors: 1) the

creditworthiness of cardholders, 2) general economic conditions, 3) the success of our account management and

collection activities, and 4) the life-cycle stage of the portfolio. During periods of economic weakness, delinquencies

and net charge-offs are more likely to increase. We have mitigated periods of economic weakness by selecting a

customer base that is very creditworthy. The median FICO scores of our securitized loans were 787 in 2007 and 785

in 2006.

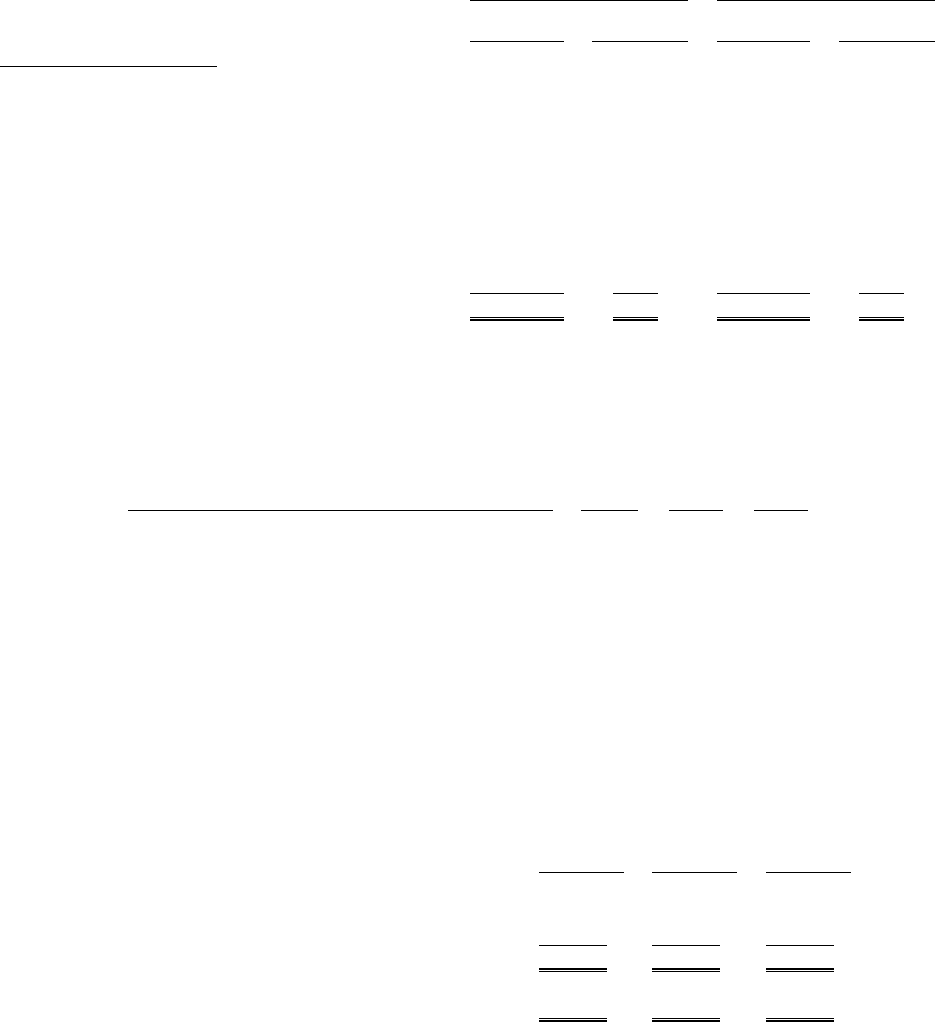

We believe that as our credit card accounts mature, they are less likely to result in a charge-off and less likely

to be closed. The following table shows our managed credit card loans outstanding at the end of 2007 and 2006

segregated by the number of months passed since the accounts were opened.

2007 2006

Loans

Outstanding

Percentage of

Total

Loans

Outstanding

Percentage of

Total

Months Since Account Opened (Dollars in Thousands)

6 months or less . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 138,021 6.7% $ 105,101 6.3%

7 – 12 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 131,988 6.4 105,296 6.3

13 – 24 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272,830 13.3 223,209 13.3

25 – 36 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243,092 11.8 193,384 11.6

37 – 48 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205,909 10.0 186,078 11.1

49 – 60 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 194,066 9.4 191,372 11.4

61 – 72 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 196,949 9.6 197,928 11.8

73 – 84 months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 200,461 9.7 247,771 14.8

85 + months . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 474,918 23.1 223,925 13.4

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $2,058,234 100.0% $1,674,064 100.0%

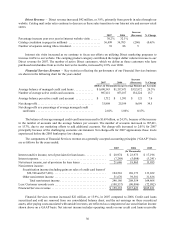

Delinquencies

We consider the entire balance of an account, including any accrued interest and fees, delinquent if the minimum

payment is not received by the payment due date. Our aging method is based on the number of completed billing

cycles during which a customer has failed to make a required payment. The following chart shows the percentage of

our managed credit card loans that have been delinquent at year end:

Number of days delinquent 2007 2006 2005

Greater than 30 days ................................................... 0.97% 0.75% 0.67%

Greater than 60 days ................................................... 0.57 0.44 0.38

Greater than 90 days ................................................... 0.28 0.18 0.16

Charge-offs

Charge-offs consist of the uncollectible principal, interest, and fees on a customer’s account. Recoveries are

the amounts collected on previously charged-off accounts. Most bankcard issuers charge-off accounts at 180 days.

Beginning in June 2007, we began charging off credit card loans on a daily basis after an account becomes at a

minimum 130 days contractually delinquent to allow us to manage the collection process more efficiently. Accounts

relating to cardholder bankruptcies, cardholder deaths, and fraudulent transactions are charged off earlier. Prior

to June 2007, we charged-off credit card loans on the 24th day of the month after an account became 115 days

contractually delinquent resulting in a 129-day average for charging-off an account. Our charge-off activity for the

managed portfolio is summarized below for the years ended:

2007 2006 2005

(Dollars in Thousands)

Charge-offs ................................. $42,853 $31,068 $27,829

Recoveries .................................. 8,955 5,869 4,227

Net charge-offs .............................. $33,898 $25,199 $23,602

Net charge-offs as a percentage of

average managed credit card loans ............ 2.01% 1.86% 2.15%