Cabela's 2007 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2007 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

41

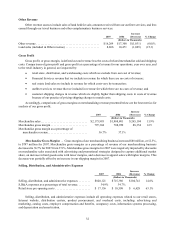

The following table summarizes our availability under debt and credit facilities, excluding the bank’s facilities,

at the end of years:

2007 2006

(In Thousands)

Amounts available for borrowing under credit facilities ......................... $ 340,000 $ 325,000

Principal amounts outstanding ............................................. (58,023) —

Outstanding letters of credit and standby letters of credit ........................ (59,596) (54,582)

Remaining borrowing capacity . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 222,381 $ 270,418

In addition, the bank has total borrowing availability of $185 million under its transferor’s interest credit

agreement and agreements to borrow federal funds. Our bank entered into a credit agreement in 2007 for a $100

million variable funding facility secured by a participation interest in the bank’s transferor’s interest of the Cabela’s

Master Credit Card Trust. These funds were used to fund continued growth of the bank’s credit card portfolio. At

the end of 2007, $100 million was outstanding under the bank’s transferor’s interest credit agreement, leaving $85

million of borrowing capacity remaining at the end of 2007.

In 2007, we issued $60 million aggregate principal amount of 6.08% senior unsecured notes. We used the

proceeds from this offering for new retail store expansion, including property and equipment additions, purchase of

economic development bonds, and general corporate purposes.

On January 16, 2008, we issued and sold $57 million of 7.20% unsecured notes to institutional buyers. The

notes have a final maturity of 10 years and an average life of seven years. We intend to use the proceeds to pay down

existing debt and for general corporate purposes.

2006 versus 2005

Operating Activities – Cash provided by operating activities decreased $18 million for 2006 compared to

2005. This net decrease was primarily due to a $51 million net decrease between years related to the bank’s funding

from securitization transactions. For 2006, the bank used cash for credit card originations (net of cash received from

collections, proceeds from new securitizations, and changes in retained interests) of $71 million compared to $20

million in 2005. Cash used for inventory increased $4 million over 2005 as we added four new retail stores. Cash

used for income taxes payable also increased by $7 million over 2005 due to the timing of federal and state income

tax payments and our increased profitability.

In addition, increases totaling $17 million comparing 2006 over 2005 relate to the use of cash from accounts

receivable, land held for sale and other assets. Partially offsetting these decreases to cash from operating activities

was a net increase of $41 million in net income adjusted for non-cash expenditures for deferred income taxes,

depreciation and amortization, stock-based compensation, and other items. Cash provided from prepaid expenses

and deferred catalog costs increased by $12 million over 2005 primarily due to the timing of catalog production

costs. Cash was also provided from various liabilities and accruals that increased by a net of $4 million over 2005.

In addition, accounts payable increased by $5 million from 2005 due to net increases in inventory payables of $10

million over 2005, partially offset by decreases of $4 million in the payable to the third party processor for the

bank’s credit card transactions and $1 million in payables for catalog costs. The decreases were related to third party

processor timing issues from 2005 and the timing in the catalog production work.

Investing Activities – Cash used in investing activities increased $64 million in 2006 compared to 2005.

The net increase in cash used was primarily due to the purchases, net of maturities, of short-term investments of

$124 million during 2006 compared to 2005. Partially offsetting this increase were net decreases in the purchases

of economic development bonds of $42 million and in property and equipment expenditures of $15 million. The

decrease in the purchases of economic development bonds related to the timing on the opening of certain new retail

stores and the incentives related to those stores. In 2006, $53 million in bonds we owned related to our Wheeling,

West Virginia, retail store and distribution center were retired in connection with a transaction whereby we took a

subordinate position on the remaining bonds we held related to this location.