Cabela's 2008 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

10

There are various federal and Nebraska laws and regulations relating to minimum regulatory capital requirements

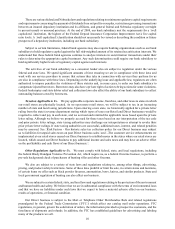

and requirements concerning the payment of dividends from net profits or surplus, restrictions governing transactions

between an insured depository institution and its affiliates, and general federal and Nebraska regulatory oversight

to prevent unsafe or unsound practices. At the end of 2008, our bank subsidiary met the requirements for a “well

capitalized” institution, the highest of the Federal Deposit Insurance Corporation Improvement Act’s five capital

ratio levels. A “well capitalized” classification should not necessarily be viewed as describing the condition or future

prospects of a depository institution, including our bank subsidiary.

Subject to certain limitations, federal bank agencies may also require banking organizations such as our bank

subsidiary to hold regulatory capital against the full risk-weighted amount of its retained securitization interests. We

understand that these federal bank agencies continue to analyze interests in securitization transactions under their

rules to determine the appropriate capital treatment. Any such determination could require our bank subsidiary to

hold significantly higher levels of regulatory capital against such interests.

The activities of our bank subsidiary as a consumer lender also are subject to regulation under the various

federal and state laws. We spend significant amounts of time ensuring we are in compliance with these laws and

work with our service providers to ensure that actions they take in connection with services they perform for us

are also in compliance with these laws. Depending on the underlying issue and applicable law, regulators are often

authorized to impose penalties for violations of these statutes and, in some cases, to order our bank subsidiary to

compensate injured borrowers. Borrowers may also have a private right of action to bring actions for some violations.

Federal bankruptcy and state debtor relief and collection laws also affect the ability of our bank subsidiary to collect

outstanding balances owed by borrowers.

Taxation Applicable to Us. We pay applicable corporate income, franchise, and other taxes to states in which

our retail stores are physically located. As we open more retail stores, we will be subject to tax in an increasing

number of state and local taxing jurisdictions. Upon entering a new state, we historically applied for a private letter

ruling from the state’s revenue department stating which types of taxes our Retail and Direct businesses would be

required to collect and pay in such state, and we accrued and remitted the applicable taxes based upon the private

letter ruling. Although we believe we properly accrued for these taxes based on our interpretation of the tax code

and prior private letter rulings, state taxing authorities may challenge our interpretation or attempt to revoke their

prior private letter rulings. If state taxing authorities are successful, additional taxes, interest, and related penalties

may be assessed. See “Risk Factors - Our historic sales tax collection policy for our Direct business may subject

us to liabilities for unpaid sales taxes on past Direct business sales” and “-The customer service enhancements we

implemented at our retail stores caused our Direct business to establish nexus in the states where our retail stores are

located, which caused our Direct business to pay additional income and sales taxes and may have an adverse effect

on the profitability and cash flows of our Direct business.”

Other Regulations Applicable to Us. We must comply with federal, state, and local regulations, including

the federal Brady Handgun Violence Prevention Act, which require us, as a federal firearms licensee, to perform a

pre-sale background check of purchasers of hunting rifles and other firearms.

We also are subject to a variety of state laws and regulations relating to, among other things, advertising,

pricing, and product safety/restrictions. Some of these laws prohibit or limit the sale, in certain states and locations,

of certain items we offer such as black powder firearms, ammunition, bows, knives, and similar products. State and

local government regulation of hunting can also affect our business.

We are subject to certain federal, state, and local laws and regulations relating to the protection of the environment

and human health and safety. We believe that we are in substantial compliance with the terms of environmental laws

and that we have no liabilities under such laws that we expect to have a material adverse effect on our business,

results of operations, or financial condition.

Our Direct business is subject to the Mail or Telephone Order Merchandise Rule and related regulations

promulgated by the Federal Trade Commission (“FTC”) which affect our catalog mail order operations. FTC

regulations, in general, govern the solicitation of orders, the information provided to prospective customers, and the

timeliness of shipments and refunds. In addition, the FTC has established guidelines for advertising and labeling

many of the products we sell.