Cabela's 2008 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

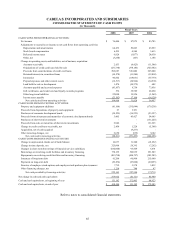

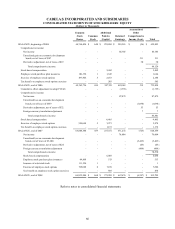

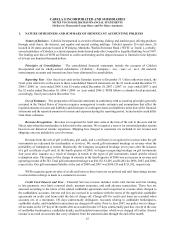

74

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

In March 2008, the FASB issued FAS No. 161, Disclosures about Derivative Instruments and Hedging

Activities—an amendment of FASB Statement No. 133. This statement changes the existing disclosure requirements in

FASB Statement No. 133, Accounting for Derivative Instruments and Hedging Activities. FAS 161 requires enhanced

disclosures about an entity’s derivative and hedging activities. This statement is effective for financial statements

issued for fiscal years and interim periods beginning after November 15, 2008, with early application encouraged.

Since the provisions of this statement are disclosure related, we do not believe that the adoption of this statement will

have a material effect on our financial position or results of operations.

On September 15, 2008, the FASB issued two exposure drafts proposing amendments to FAS 140, Accounting

for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities and FASB Interpretation No. 46R,

Consolidation of Variable Interest Entities. Currently, the transfers of our bank subsidiary’s credit card receivables in

securitization transactions qualify for sale accounting treatment. The trusts used in our bank subsidiary’s securitizations

are not consolidated with us for financial reporting purposes because the trusts are qualifying special purpose

entities. Because the transfers qualify as sales and the trusts are not subject to consolidation, the assets and liabilities

of the trusts are not reported on our consolidated balance sheet under generally accepted accounting principles.

Under the proposed amendments, the concept of a QSPE would be eliminated and would modify the consolidation

model for variable interest entities and require continual reassessment of consolidation conclusions. As proposed,

these amendments would be effective for us at the beginning of our 2010 fiscal year. The proposed amendments, if

adopted, could require us to consolidate the assets and liabilities of our bank subsidiary’s securitization trusts. This

could cause us to breach certain financial covenants in our credit agreements and unsecured notes. This could have

a significant effect on our financial condition and ability to meet the regulatory capital maintenance requirements

of our bank subsidiary, as affected off-balance sheet loans would be recorded on our consolidated balance sheet and

may be subject to regulatory capital requirements. Additionally, if WFB does not meet the requirements for the well-

capitalized category under the regulatory framework for prompt corrective action, the ability to obtain certificates

of deposit could be affected.

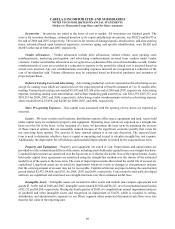

On December 11, 2008, the FASB issued FASB Staff Position No. FAS 140-4 and FIN 46(R)-8, Disclosures

by Public Entities (Enterprises) about Transfers of Financial Assets and Interests in Variable Interest Entities. As a

result of the new FSP issuers must provide additional disclosures about transfers of financial assets and involvement

with variable interest entities. The requirements apply to transferors, sponsors, servicers, primary beneficiaries, and

holders of significant variable interests in a variable interest entity or qualifying special purpose entity. The Staff

Position is effective for the first interim period or fiscal year ending after December 15, 2008, and each interim and

annual period thereafter until the effective date of the amendments to FAS 140 and Interpretation 46R, which are still

being deliberated. The new requirements include disclosure objectives as well as required specified disclosures. The

specified disclosures focus both on continuing involvement with transferred financial assets, including involvement

related to securitizations or asset-backed financing arrangements, and on a company’s involvement with VIEs. The

Company has included the required disclosures below in Note 4. The adoption of FSP FAS 140-4 did not have any

impact on our financial position or results of operations.

On January 12, 2009, the FASB issued FASB Staff Position No. EITF 99-20-1, Amendments to the Impairment

Guidance of EITF Issue No. 99-20. The FSP eliminates the requirement that a holder’s best estimate of cash flows

be based upon those “that a market participant” would use. Instead, the FSP requires that an other-than-temporary

impairment be recognized through earnings when it is probable that there has been an adverse change in the holder’s

estimated cash flows from the cash flows previously projected. The Staff Position is effective for the first interim

period or fiscal year ending after December 15, 2008, and each interim and annual period thereafter. Retroactive

application to a prior interim period is not permitted. The adoption of FSP EITF 99-20-1 did not have any impact on

our financial position or results of operations.