Cabela's 2008 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

89

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

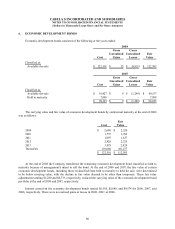

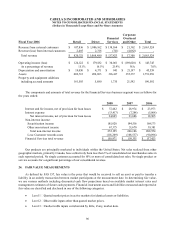

17. REGULATORY CAPITAL REQUIREMENTS

WFB is subject to various regulatory capital requirements administered by the FDIC and the Nebraska State

Department of Banking and Finance. Under capital adequacy guidelines and the regulatory framework for prompt

corrective action, WFB must meet specific capital guidelines that involve quantitative measures of WFB’s assets,

liabilities, and certain off-balance sheet items as calculated under regulatory accounting practices. WFB’s capital

amounts and classification are also subject to qualitative judgment by the regulators with respect to components, risk

weightings, and other factors.

The quantitative measures established by regulation to ensure capital adequacy require that WFB maintain

minimum amounts and ratios (defined in the regulations) as set forth in the following table. WFB exceeded the

minimum requirements for the well-capitalized category under the regulatory framework for prompt corrective

action provisions for both periods presented.

As of December 31, 2008 and 2007, the most recent notification from the FDIC categorized WFB as well

capitalized under the regulatory framework for prompt corrective action. To be categorized as well capitalized WFB

must maintain certain amounts and ratios as set forth in the following table. There are no conditions or events since

that notification that management believes have changed the institution’s category.

2008

Ratio Required to be Considered

Actual Adequately-Capitalized Well-Capitalized

Amount Ratio Amount Ratio Amount Ratio

Total Capital to Risk-Weighted Assets $ 166,611 28.1% $ 47,460 8.0% $ 59,325 10.0%

Tier I Capital to Risk-Weighted Assets 140,886 23.8 23,730 4.0 35,595 6.0

Tier I Capital to Average Assets 140,886 23.6 23,842 4.0 29,803 5.0

2007

Ratio Required to be Considered

Actual Adequately-Capitalized Well-Capitalized

Amount Ratio Amount Ratio Amount Ratio

Total Capital to Risk-Weighted Assets $ 118,030 16.8% $ 56,102 8.00% $ 70,127 10.0%

Tier I Capital to Risk-Weighted Assets 114,336 16.3 28,051 4.0 42,076 6.0

Tier I Capital to Average Assets 114,336 27.6 16,568 4.0 20,710 5.0

In December 2008, WFB received $25,000 from Cabela’s in exchange for 250,000 shares of WFB convertible

participating preferred stock. If management elected to covert the participating preferred stock to WFB common

stock, the $25,000 would qualify as Tier 1 capital.

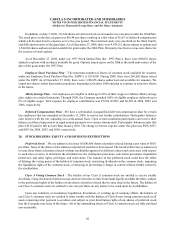

18. STOCK BASED COMPENSATION AND STOCK OPTION PLANS

Under the provisions of FAS 123R, we recorded share-based compensation expense of $6,535 ($4,222 after-tax,

or $.06 per diluted share), $4,944 ($3,115 after-tax, or $0.05 per diluted share), and $3,615 ($2,259 after-tax, or $.03

per diluted share) for 2008, 2007, and 2006, respectively. Compensation expense related to our share-based payment

awards is recorded in selling, distribution, and administrative expenses in the consolidated statements of income.

During 2006, share-based compensation expense was recorded for awards granted since 2004 but not yet vested

as of January 1, 2006. For these awards, we recognized compensation expense using the accelerated or graded method

of amortization. Compensation cost for awards granted after the adoption date is recognized using a straight-line