Cabela's 2008 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

48

Furthermore, poor performance of WFB’s securitized credit card loans, including increased delinquencies and

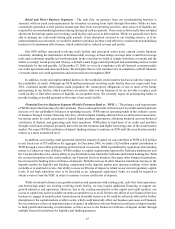

credit losses, lower payment rates, or a decrease in excess spreads below certain thresholds, could result in a downgrade

or withdrawal of the ratings on the outstanding securities issued in WFB’s securitization transactions, cause early

amortization of these securities, or result in higher required credit enhancement levels. On February 19, 2009, Moody’s

Investors Service announced that it had downgraded the ratings on 21 classes of asset-backed notes issued by the

trust of our Financial Services business. Downgrades could negatively impact the ability of our Financial Services

business to complete other securitization transactions on acceptable terms or at all and force our Financial Services

business to rely on other potentially more expensive funding sources, to the extent available, which would decrease

our profitability. We do not believe that this downgrade will have a significant impact on the ability of our Financial

Services business to complete other securitization transactions on acceptable terms or to access financing.

The proposed amendments issued by the Financial Accounting Standards Board to FAS 140 and FASB

Interpretation No. 46R, if adopted, could require us to consolidate the assets and liabilities of our bank subsidiary’s

securitization trusts. This could cause us to breach certain financial covenants in our revolving credit facility and

unsecured notes. This could also have a significant effect on our financial condition and ability to meet the capital

maintenance requirements of our bank subsidiary, as affected off-balance sheet loans would be recorded on our

consolidated balance sheet and could be subject to regulatory capital requirements. If the proposed amendments are

adopted, we may have to contribute capital to WFB, which may require us to raise additional debt or equity capital and/

or divert capital from our Retail and Direct businesses, which in turn could significantly alter our growth initiatives.

Operating, Investing and Financing Activities

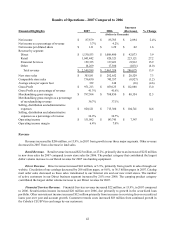

The following table presents changes in our cash and cash equivalents for the years ended:

2008 2007 2006

(In Thousands)

Net cash derived from operating activities $ 154,968 $ 31,828 $ 54,957

Net cash used in investing activities (98,211)(331,493) (144,696)

Net cash provided by financing activities 222,165 257,944 175,719

2008 versus 2007

Operating Activities – Cash derived from operating activities increased $123 million for 2008 compared to

2007. Inventory balances decreased $91 million at the end of 2008 over 2007, resulting in a net improvement in cash

due to a net change in cash flows of $210 million between years in inventory. We focused on inventory reduction in

2008 compared to 2007 in which we opened eight new stores. Cash derived from operating activities also included a

$63 million net increase between years related to WFB’s proceeds from securitization transactions, net of originations

of credit card loans. For 2008, WFB received cash on a net basis for credit card originations (net of cash received from

collections, proceeds from new securitizations, and changes in retained interests) of $21 million compared to $42

million of net cash used in 2007. In addition, land held for sale or development increased $12 million compared to

2007 as we increased our holdings in land investment. Partially offsetting these improvements in cash was a decrease

in accounts payable and accrued expenses of $94 million between years, mostly due to the reduction in inventory in

2008 compared to 2007, as the accounts payable and accrued expenses balances decreased $108 million at the end

of 2008 compared to 2007. The net change in the liability for gift instruments and credit card reward points was a

decrease of $39 million over 2007 from increased sales of gift cards in the prior year compared to 2008. In addition,

the net change in current and deferred income taxes payable was a decrease of $33 million in 2008 compared to 2007

due to nearly $56 million paid in 2008 for federal and state income taxes.

Investing Activities – Cash used in investing activities decreased $233 million for 2008 compared to 2007.

This net decrease was primarily due to less expenditures related to the development and construction of the new

retail stores in 2008 compared to 2007. For 2008, cash paid for property and equipment additions totaled $91 million

compared to $336 million for 2007. We opened our Scarborough, Maine, store in May 2008, and our Rapid City,