Cabela's 2008 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

54

Furthermore, poor performance of WFB’s securitized credit card loans, including increased delinquencies

and credit losses, lower payment rates, or a decrease in excess spreads below certain thresholds, could result in a

downgrade or withdrawal of the ratings on the outstanding securities issued in WFB’s securitization transactions, cause

early amortization of these securities, or result in higher required credit enhancement levels. On February 19, 2009,

Moody’s Investors Service announced that it had downgraded the ratings on 21 classes of asset-backed notes issued

by WFB’s securitization trust. Downgrades could negatively impact WFB’s ability to complete other securitization

transactions on acceptable terms or at all and force WFB to rely on other potentially more expensive funding sources,

to the extent available, which would decrease our profitability. We do not believe that this downgrade will have a

significant impact on the ability of our Financial Services business to complete other securitization transactions on

acceptable terms or to access financing.

Certificates of Deposit

WFB utilizes brokered and non-brokered certificates of deposit to partially finance its operating activities.

WFB issues certificates of deposit in a minimum amount of one hundred thousand dollars in various maturities. As

of December 27, 2008, WFB had $486 million of certificates of deposit outstanding with maturities ranging from

January 2009 to April 2016 and with a weighted average effective annual fixed rate of 4.64%. This outstanding balance

compares to $161 million at December 29, 2007, with a weighted average effective annual fixed rate of 5.01%.

Impact of Inflation

We do not believe that our operating results have been materially affected by inflation during the preceding

three years. We cannot assure, however, that our operating results will not be adversely affected by inflation in the

future.

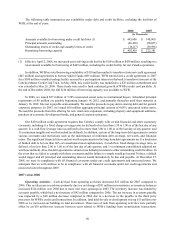

Contractual Obligations and Other Commercial Commitments

The following tables provide summary information concerning our future contractual obligations at the end

of 2008.

2009 2010 2011 2012 2013 Thereafter Total

(In Thousands)

Long-term debt (1) $ 588 $7,087 $663 $28,842 $8,889 $320,297 $366,366

Interest payments (2) 20,805 20,778 20,750 20,426 19,807 52,313 154,879

Capital lease obligations 1,075 1,000 1,000 1,000 1,000 22,500 27,575

Operating leases 5,616 5,090 4,604 4,167 4,167 83,902 107,546

Time deposits by

maturity 178,817 82,357 115,230 34,912 74,683 200 486,199

Obligations under new

store and expansion

arrangements (3) 14,159 81,969 680 1,701 735 4,578 103,822

Purchase obligations (4) 427,969 14,974 9,047 6,257 4,988 - 463,235

Deferred compensation 2,759 2,433 - - - - 5,192

Unrecognized tax

benefits - - - - - 3,076 3,076

Total $651,788 $215,688 $151,974 $97,305 $114,269 $486,866 $1,717,890

(1) Includes $20 million owed under our $430 million credit agreement, and $6 million owed under our $15 million

credit agreement for operations in Canada. Excludes amounts owed under capital lease obligations.

(2) These amounts do not include estimated interest payments due under our revolving credit facilities because the

amount that will be borrowed under these facilities in future years is uncertain.