Cabela's 2008 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2008 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

|

|

45

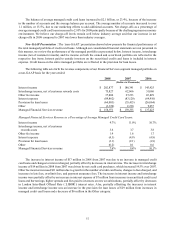

Bank Asset Quality

Overview

We securitize a majority of our credit card loans. On a quarterly basis, we transfer eligible credit card loans

into a securitization trust. We are required to own at least a minimum twenty day average of 5% of the interests in

the securitization trust. This required amount is our transferor’s interest that totaled $143 million at the end of 2008.

Accordingly, retained credit card loans have the same characteristics as credit card loans sold to outside investors.

Certain accounts are ineligible for securitization for reasons such as: 1) they are delinquent, 2) they originated

from sources other than Cabela’s CLUB Visa credit cards, or 3) various other requirements. Loans ineligible for

securitization totaled $11 million at the end of 2008 compared to $15 million at the end of 2007.

The quality of our managed credit card loan portfolio at any time reflects, among other factors: 1) the

creditworthiness of cardholders, 2) general economic conditions, 3) the success of our account management and

collection activities, and 4) the life-cycle stage of the portfolio. During periods of economic weakness, delinquencies

and net charge-offs are more likely to increase. We have mitigated periods of economic weakness by selecting a

customer base that is very creditworthy. The median FICO score of our credit cardholders was 786 at the end of 2008

and at the end of 2007.

We believe that as our credit card accounts mature, they are less likely to result in a charge-off and less likely

to be closed. The following table shows our managed credit card loans outstanding at the end of 2008 and 2007

segregated by the number of months passed since the accounts were opened.

2008 2007

Months Since Account Opened Loans

Outstanding Percentage

of Total Loans

Outstanding Percentage

of Total

(Dollars in Thousands)

6 months or less $ 121,603 5.2% $ 138,021 6.7%

7 – 12 months 151,201 6.5 131,988 6.4

13 – 24 months 330,973 14.1 272,830 13.3

25 – 36 months 278,318 11.9 243,092 11.8

37 – 48 months 239,563 10.2 205,909 10.0

49 – 60 months 200,463 8.5 194,066 9.4

61 – 72 months 188,233 8.0 196,949 9.6

73 – 84 months 190,425 8.1 200,461 9.7

More than 84 months 646,444 27.5 474,918 23.1

Total $2,347,223 100.0% $ 2,058,234 100.0%

Delinquencies

We consider the entire balance of an account, including any accrued interest and fees, delinquent if the minimum

payment is not received by the payment due date. Our aging method is based on the number of completed billing

cycles during which a customer has failed to make a required payment. The following chart shows the percentage of

our managed credit card loans that were delinquent at year end:

Number of days delinquent 2008 2007 2006

Greater than 30 days 1.68%0.97%0.75%

Greater than 60 days 0.97 0.57 0.44

Greater than 90 days 0.47 0.28 0.18