Electronic Arts 2005 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2005 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

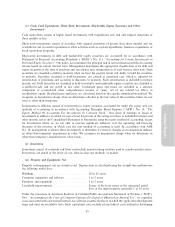

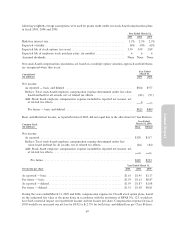

(l) Sales Returns and Allowances and Bad Debt Reserves

We estimate potential future product returns, price protection and stock-balancing programs related to current

period product revenue. We analyze historical returns, current sell-through of channel partner inventory of our

products, current trends in the software games business segment and the overall economy, changes in

customer demand and acceptance of our products and other related factors when evaluating the adequacy of

the sales returns and price protection allowances. In addition, we monitor the volume of sales to our channel

partners and monitor their inventories as substantial overstocking in the distribution channel could result in

high returns or higher price protection costs in subsequent periods.

Similarly, signiÑcant judgment is required to estimate our allowance for doubtful accounts in any accounting

period. We analyze customer concentrations, customer credit-worthiness and current economic trends when

evaluating the adequacy of the allowance for doubtful accounts.

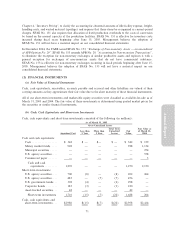

(m) Advertising Costs

We generally expense advertising costs as incurred, except for production costs associated with media

campaigns which are recognized as prepaid assets (to the extent paid in advance) and expensed at the Ñrst run

of the advertisement. Cooperative advertising with our channel partners is accrued when revenue is recognized

and such amounts are included in marketing and sales expense if there is a separate identiÑable beneÑt for

which we can reasonably estimate the fair value of the beneÑt identiÑed. Otherwise, they are recognized as a

reduction of net revenue. We then reimburse the channel partner when qualifying claims are submitted. For

the Ñscal years ended March 31, 2005, 2004 and 2003, advertising expenses totaled approximately $174 mil-

lion, $183 million and $152 million, respectively. We sometimes receive vendor reimbursements for

advertising costs from our vendors, and such amounts are recognized as a reduction of marketing and sales

expense if there is a separate identiÑable beneÑt for which we can reasonably estimate the fair value of the

beneÑt identiÑed. Otherwise, they are recognized as a reduction of cost of goods sold. Included in marketing

and sales expense are vendor reimbursements of advertising expenses of $42 million, $45 million, and

$28 million for the Ñscal years ended March 31, 2005, 2004, and 2003, respectively.

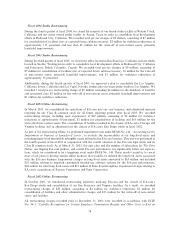

(n) Software Development Costs

Research and development costs, which consist primarily of software development costs, are expensed as

incurred. SFAS No. 86, ""Accounting for the Cost of Computer Software to be Sold, Leased, or Otherwise

Marketed'', provides for the capitalization of certain software development costs incurred after technological

feasibility of the software is established or for development costs that have alternative future uses. Under our

current practice of developing new products, the technological feasibility of the underlying software is not

established until substantially all product development is complete, which generally includes the development

of a working model. The software development costs that have been capitalized to date have been

insigniÑcant.

(o) Stock-based Compensation

We account for stock-based awards to employees using the intrinsic value method in accordance with APB

No. 25, ""Accounting for Stock Issued to Employees''. We have adopted the disclosure-only provisions of

SFAS No. 123, ""Accounting for Stock-Based Compensation'', as amended.

Had compensation cost for our stock-based compensation plans been measured based on the estimated fair

value at the grant dates in accordance with the provisions of SFAS No. 123, we estimate that our reported net

income and net income per share would have been the pro forma amounts indicated below. The fair value of

each option grant is estimated on the date of grant using the Black-Scholes option-pricing model. The

68