Electronic Arts 2005 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2005 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

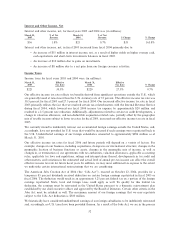

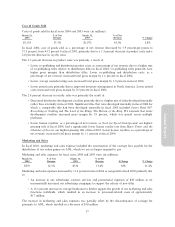

Income Taxes

Income taxes for Ñscal years 2004 and 2003 were (in millions):

March 31, EÅective March 31, EÅective

2004 Tax Rate 2003 Tax Rate % Change

$220 27.5% $143 31.0% 53.3%

Our eÅective income tax rate reÖected tax beneÑts derived from signiÑcant operations outside the U.S., which

are generally taxed at rates lower than the U.S. statutory rate of 35 percent. The eÅective income tax rate was

27.5 percent for Ñscal 2004 and 31.0 percent for Ñscal 2003. The reduced eÅective income tax rate in Ñscal

2004 primarily reÖected the resolution of certain tax-related matters with the Internal Revenue Service in the

fourth quarter of Ñscal 2004, which lowered our income tax expense by $20 million and resulted in a

2.5 percent rate reduction, and also reÖected a change in the geographic mix of taxable income subject to

lower tax rates.

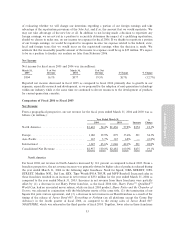

Net Income

Net income for Ñscal years 2004 and 2003 was (in millions):

March 31, % of Net March 31, % of Net

2004 Revenue 2003 Revenue $ Change % Change

$577 19.5% $317 12.8% $260 82.1%

Reported net income increased in Ñscal 2004 compared to Ñscal 2003 primarily due to the reasons discussed

above. Although the dollar amount of our expenses increased in Ñscal 2004 as compared to Ñscal 2003, net

income as a percentage of net revenue increased to 19.5 percent as compared to 12.8 percent in Ñscal 2003 as

expenses, including our cost of goods sold, grew at a slower rate than did our net revenue.

Impact of Recently Issued Accounting Standards

In March 2004, the Financial Accounting Standards Board (""FASB'') ratiÑed the other-than-temporary

impairment measurement and recognition guidance and certain disclosure requirements for impaired securi-

ties as described in EITF Issue No. 03-1, ""The Meaning of Other-Than-Temporary Impairment and Its

Application to Certain Investments''. In September 2004, the FASB issued a proposed StaÅ Position (""FSP'')

EITF Issue No. 03-1-a, ""Implementation Guidance for the Application of Paragraph 16 of EITF 03-1''. The

proposed FSP will provide measurement and recognition guidance with respect to debt securities that are

impaired solely due to interest rates and/or sector spreads. In October 2004, the FASB delayed the eÅective

date for the other-than-temporary impairment measurement and recognition guidance contained in

Annual Report

paragraphs 10-20 of EITF Issue No. 03-1 until FSP Issue No. 03-1-a is issued. However, this delay does not

suspend the requirement to recognize other-than-temporary impairments as required by existing authoritative

literature; nor does it delay the required disclosures about unrealized losses that have not been recognized as

other-than-temporary impairments in paragraphs 21-22 of EITF Issue No. 03-1. See Note 2 of the Notes to

Consolidated Financial Statements. Management is unable to determine what impact the adoption of the

measurement and recognition guidance in EITF Issue No. 03-1 will have on our consolidated Ñnancial

statements.

In November 2004, the FASB issued SFAS No. 151, ""Inventory Costs Ì an amendment of ARB No. 43,

Chapter 4''. SFAS No. 151 amends the guidance in Accounting Research Bulletin (""ARB'') No. 43,

Chapter 4, ""Inventory Pricing'', to clarify the accounting for abnormal amounts of idle facility expense, freight,

handling costs, and wasted material (spoilage) and requires that those items be recognized as current-period

charges. SFAS No. 151 also requires that allocation of Ñxed production overheads to the costs of conversion

be based on the normal capacity of the production facilities. SFAS No. 151 is eÅective for inventory costs

incurred during Ñscal years beginning after June 15, 2005. Management believes the adoption of

SFAS No. 151 will not have a material impact on our consolidated Ñnancial statements.

In December 2004, the FASB issued SFAS No. 153, ""Exchange of Non-monetary Assets Ì an amendment

of APB Opinion No. 29''. SFAS No. 153 amends Accounting Principles Board (""APB'') No. 29, ""Accounting

41