Electronic Arts 2007 Annual Report Download - page 147

Download and view the complete annual report

Please find page 147 of the 2007 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

|

|

FIN No. 48 are treated as the cumulative effect of a change in accounting principle. We are evaluating what

impact the adoption of FIN No. 48 will have on our Consolidated Financial Statements. This impact could be

material and our future effective tax rates could be more volatile.

In September 2006, the FASB issued SFAS No. 157, “Fair Value Measurements”. SFAS No. 157 defines fair

value, establishes a framework for measuring fair value in generally accepted accounting principles and

expands disclosures about fair value measurements. Fair value refers to the price that would be received to sell

an asset or paid to transfer a liability in an orderly transaction between market participants in the market in

which the reporting entity transacts. SFAS No. 157 establishes a fair value hierarchy that prioritizes the

information used to develop those assumptions. Fair value measurements would be separately disclosed by

level within the fair value hierarchy. The provisions of SFAS No. 157 are effective for financial statements

issued for fiscal years beginning after November 15, 2007, and interim periods within those fiscal years. We

do not expect the adoption of SFAS No. 157 to have a material impact on our Consolidated Financial

Statements.

In February 2007, the FASB issued SFAS No. 159, “The Fair Value Option for Financial Assets and Financial

Liabilities — Including an amendment of FASB Statement No. 115”. SFAS No. 159 permits entities to choose

to measure many financial instruments and certain other items at fair value that are not currently required to

be measured at fair value. It also establishes presentation and disclosure requirements designed to facilitate

comparisons between entities that choose different measurement attributes for similar types of assets and

liabilities. The provisions of SFAS No. 159 are effective for financial statements issued for fiscal years

beginning after November 15, 2007. This Statement should not be applied retrospectively to fiscal years

beginning prior to the effective date, except as permitted with early adoption. We are evaluating if we will

adopt SFAS No. 159 and what impact the adoption will have on our Consolidated Financial Statements if we

adopt. If we adopt SFAS No. 159, it may have a material impact on our Consolidated Financial Statements.

In March 2007, the EITF issued a tentative conclusion on EITF 07-03, “Accounting for Advance Payments for

Goods or Services to Be Used in Future Research and Development” and the FASB ratified the tentative

conclusion. The FASB exposed the EITF tentative conclusion for public comment. The comment period was

expected to end in May 2007. EITF 07-03 addresses the diversity which exists with respect to the accounting

for the non-refundable portion of a payment made by a research and development entity for future research

and development activities. Under this tentative conclusion, an entity would defer and capitalize non-

refundable advance payments made for research and development activities until the related goods are

delivered or the related services are performed. If a final consensus is reached on this tentative conclusion,

EITF 07-03 would be effective for interim or annual reporting periods in fiscal years beginning after

December 15, 2007. We do not expect the adoption of EITF 07-03 to have a material impact on our

Consolidated Financial Statements if ratified by the FASB as currently proposed.

(2) FINANCIAL INSTRUMENTS

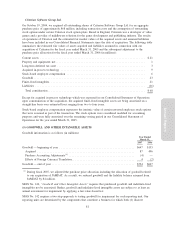

(a) Fair Value of Financial Instruments

Cash, cash equivalents, receivables, accounts payable and accrued and other liabilities are valued at their

carrying amounts as they approximate their fair value due to the short maturity of these financial instruments.

Annual Report

73