Electronic Arts 2007 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2007 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

|

|

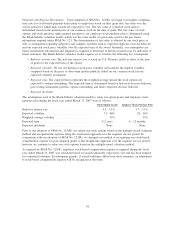

The following table summarizes stock-based compensation expense resulting from stock options, restricted

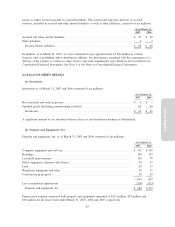

stock, restricted stock units and our employee stock purchase plan included in our Consolidated Statements of

Operations (in millions):

2007 2006 2005

Year Ended March 31,

Cost of goods sold ................................................... $ 2 $— $—

Marketing and sales .................................................. 17 — —

General and administrative ............................................. 37 1 —

Research and development ............................................. 77 2 6

Stock-based compensation expense ..................................... 133 3 6

Benefit from income taxes.............................................. (26) (1) (2)

Stock-based compensation expense, net of tax ............................. $107 $ 2 $ 4

As of March 31, 2007, our total unrecognized compensation cost related to stock options was $153 million

and is expected to be recognized over a weighted-average service period of 1.6 years. As of March 31, 2007,

our total unrecognized compensation cost related to restricted stock and restricted stock units was $82 million

and is expected to be recognized over a weighted-average service period of 2.3 years.

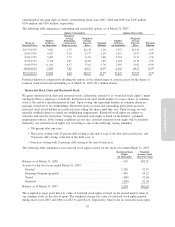

The adoption of SFAS No. 123(R), using the fair value method, had the following adverse impact on our pre-

tax income, net income, and basic and diluted net income per share as compared to what would have been

reported under APB No. 25 using the intrinsic value method, which was the method used prior to our adoption

for the year ended March 31, 2007 (in millions, except per share data):

Fair Value

Method

(As Reported)

Intrinsic

Value

Method

Adverse

Impact

of Change

Income before provision for income taxes and minority interest ........ $138 $237 $ (99)

Net income .............................................. $ 76 $153 $ (77)

Net income per share:

Basic ................................................. $0.25 $0.50 $(0.25)

Diluted ................................................ $0.24 $0.48 $(0.24)

APIC Pool. In November 2005, the FASB issued FASB Staff Position (“FSP”) No. Financial Accounting

Standard (“FAS”) 123(R)-3, “Transition Election Related to Accounting for the Tax Effects of Share-Based

Payment Awards”. The FASB allows for a practical exception in calculating the additional paid-in capital pool

(“APIC pool”) of excess tax benefits upon adoption that is available to absorb tax deficiencies recognized

subsequent to the adoption of SFAS No. 123(R). For employee stock-based compensation awards that are

outstanding upon adoption of SFAS No. 123(R), the alternative transition method provides a simplified method

to establish the beginning balance of the APIC pool related to the tax effects of employee stock-based

compensation. It also provides a simplified method to determine the subsequent impact on the APIC pool and

Consolidated Statements of Cash Flows for the tax effects of employee stock-based compensation awards. We

elected to adopt the alternative transition method provided in FSP No. FAS 123(R)-3 for calculating the tax

effects of stock-based compensation pursuant to SFAS No. 123(R).

Cash Flow Impact. Prior to our adoption of SFAS No. 123(R), cash retained as a result of tax deductions

relating to stock-based compensation was presented in operating cash flows along with other tax cash flows.

SFAS No. 123(R) requires a classification change in the statement of cash flows. As a result, tax benefits

relating to excess stock-based compensation deductions, which had been included in operating cash flow

activities, are now presented as financing cash flow activities (total cash flows remain unchanged). For the

fiscal year ended March 31, 2007, we recognized $34 million of tax benefit from the exercise of stock options;

of this amount, $36 million of excess tax benefit related to stock-based compensation reported in financing

activities. For the fiscal year ended March 31, 2006, we recognized $133 million of tax benefit from exercise

of stock options reported in operating activities.

Annual Report

95