Ford 2013 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2013 Ford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Ford Motor Company | 2013 Annual Report 83

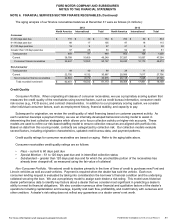

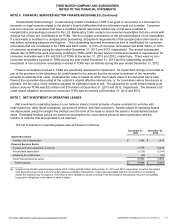

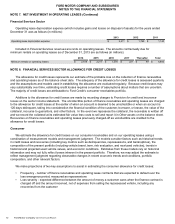

FORD MOTOR COMPANY AND SUBSIDIARIES

NOTES TO THE FINANCIAL STATEMENTS

NOTE 4. FAIR VALUE MEASUREMENTS (Continued)

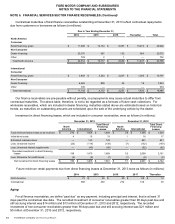

The fair value of collateral for retail receivables is calculated based on the number of contracts multiplied by the loss

severity and the probability of default (“POD”) percentage, or the outstanding receivable balances multiplied by the

average recovery value (“ARV”) percentage to determine the fair value adjustment.

The fair value of collateral for dealer loans is determined by reviewing various appraisals, which include total adjusted

appraised value of land and improvements, alternate use appraised value, broker's opinion of value, and purchase offers.

The fair value adjustment is calculated by comparing the net carrying value of the dealer loan and the estimated fair value

of collateral.

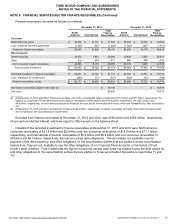

The fair value of retail and dealer loans measured on a non-recurring basis was $61 million and $80 million at

December 31, 2013 and December 31, 2012, respectively. Changes in the significant unobservable inputs will not

materially affect the fair value of these loans. The fair value adjustment recorded to expense for these receivables was

$20 million, $25 million and $37 million in 2013, 2012 and 2011, respectively.

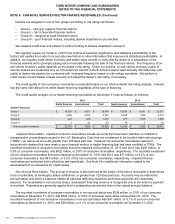

Debt. We measure debt at fair value for purposes of disclosure (see Note 15) using quoted prices for our own debt

with approximately the same remaining maturities, where possible. Where quoted prices are not available, we estimate

fair value using discounted cash flows and market-based expectations for interest rates, credit risk, and the contractual

terms of the debt instruments. For certain short-term debt with an original maturity date of one year or less, we assume

that book value is a reasonable approximation of the debt’s fair value. The fair value of debt is categorized within Level 2

of the hierarchy.

For more information visit www.annualreport.ford.com