GE 2006 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2006 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

We amortize the cost of other intangibles over their estimated

useful lives unless such lives are deemed indefi nite. Amortizable

intangible assets are tested for impairment based on undiscounted

cash flows and, if impaired, written down to fair value based

on either discounted cash flows or appraised values. Intangible

assets with indefinite lives are tested annually for impairment

and written down to fair value as required.

GECS investment contracts, insurance liabilities and

insurance annuity benefits

Certain SPEs, which we consolidate, provide guaranteed invest-

ment contracts to states, municipalities and municipal authorities.

Our insurance activities also include providing insurance and

reinsurance for life and health risks and providing certain annuity

products. Three product groups are provided: traditional insurance

contracts, investment contracts and universal life insurance

contracts. Insurance contracts are contracts with signifi cant

mortality and/or morbidity risks, while investment contracts are

contracts without such risks. Universal life insurance contracts

are a particular type of long-duration insurance contract whose

terms are not fixed and guaranteed.

For short-duration insurance contracts, including accident and

health insurance, we report premiums as earned income over the

terms of the related agreements, generally on a pro-rata basis.

For traditional long-duration insurance contracts including term,

whole life and annuities payable for the life of the annuitant, we

report premiums as earned income when due.

Premiums received on investment contracts (including annui-

ties without significant mortality risk) and universal life contracts

are not reported as revenues but rather as deposit liabilities.

We recognize revenues for charges and assessments on these

contracts, mostly for mortality, contract initiation, administration

and surrender. Amounts credited to policyholder accounts are

charged to expense.

Liabilities for traditional long-duration insurance contracts

represent the present value of such benefits less the present value

of future net premiums based on mortality, morbidity, interest

and other assumptions at the time the policies were issued or

acquired. Liabilities for investment contracts and universal life

policies equal the account value, that is, the amount that accrues

to the benefit of the contract or policyholder including credited

interest and assessments through the financial statement date.

Liabilities for unpaid claims and claims adjustment expenses

represent our best estimate of the ultimate obligations for

reported and incurred-but-not-reported claims and the related

estimated claim settlement expenses. Liabilities for unpaid claims

and claims adjustment expenses are continually reviewed and

adjusted through current operations.

Accounting changes

We adopted Financial Accounting Standards Board (FASB)

Statement of Financial Accounting Standards (SFAS) 123 (Revised

2004), Share-Based Payment (SFAS 123R) and related FASB Staff

Positions (FSPs), effective January 1, 2006. Among other things,

SFAS 123R requires expensing the fair value of stock options,

a previously optional accounting method that we adopted

voluntarily in 2002, and classification of excess tax benefi ts

associated with share-based compensation deductions as cash

from financing activities rather than cash from operating activities.

We chose the modified prospective transition method, which

requires that the new guidance be applied to the unvested portion

of all outstanding stock option grants as of January 1, 2006, and

to new grants after that date. We further applied the alternative

transition method provided in FSP FAS 123(R) –3, Transition

Election Related to Accounting for the Tax Effects of Share-Based

Payment Awards. The transitional effects of SFAS 123R and

related FSPs consisted of a reduction in net earnings of $10 million

for the year ended December 31, 2006, to expense the unvested

portion of options granted in 2001; and classification of $173 million

related to excess tax benefits from share-based compensation

deductions as cash from financing activities in our Statement of

Cash Flows beginning in 2006, which previously would have

been included in cash from operating activities.

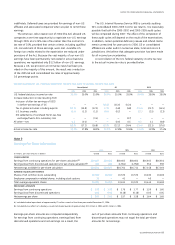

A comparison of reported net earnings for 2006, 2005 and

2004, and pro-forma net earnings for 2005 and 2004, including

effects of expensing stock options, follows.

(In millions; per-share amounts in dollars) 2006 2005 2004

Net earnings, as reported $20,829 $16,711 $17,160

Earnings per share, as reported

Diluted 2.00 1.57 1.64

Basic 1.65

Stock option expense

included in net earnings

2.01 1.58

96 106 93

Total stock option expense(a) 96 191 245

PRO-FORMA EFFECTS

(b)

Net earnings, on pro-forma basis 16,626 17,008

Earnings per share, on pro-forma basis

Diluted 1.57 1.63

(b)

(b)

Basic 1.57 1.64

Other share-based compensation expense recognized in net earnings amounted to

$130 million, $87 million and $95 million in 2006, 2005 and 2004, respectively.

The total income tax benefit recognized in earnings for all share-based compensation

arrangements amounted to $117 million, $115 million and $101 million in 2006, 2005

and 2004, respectively.

(a) As if we had applied SFAS 123R to expense stock options in all periods. Included

amounts we actually recognized in earnings.

(b) Not applicable. As of January 1, 2006, total stock option expense is included in

net earnings.

SFAS 158, Employers’ Accounting for Defi ned Benefi t Pension

and Other Postretirement Plans, became effective for us as of

December 31, 2006, and requires recognition of an asset or

liability in the statement of financial position reflecting the funded

status of pension and other postretirement benefit plans such as

retiree health and life, with current-year changes in the funded

status recognized in shareowners’ equity. SFAS 158 did not

change the existing criteria for measurement of periodic benefi t

costs, plan assets or benefi t obligations.

ge 2006 annual report 77