GE 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 GE annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

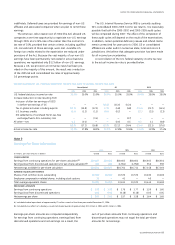

The effect on operations of principal retiree benefit plans follows.

COST OF PRINCIPAL RETIREE BENEFIT PLANS

(In millions) 2006 2005 2004

Expected return on plan assets $(127) $ (138) $(149)

Service cost for benefi ts earned 229 243 210

Interest cost on benefi t obligation 455 507 518

Prior service cost 363 326 298

Net actuarial loss recognized 64 70 60

Retiree benefit plans cost $ 984 $1,008 $ 937

ACTUARIAL ASSUMPTIONS. The discount rates at December 31

were used to measure the year-end benefit obligations and the

earnings effects for the subsequent year. Actuarial assumptions

used to determine benefit obligations and earnings effects for

principal retiree benefit plans follow.

ACTUARIAL ASSUMPTIONS

December 31 2006 2005 2004 2003

Discount rate(a) 5.75% 5.25% 5.75% 6.00%

Compensation increases 5.00 5.00 5.00 5.00

Expected return on assets 8.50 8.50 8.50 8.50

Initial healthcare trend rate

(b) 9.20 10.00 10.30 10.50

(a) Weighted average discount rates of 5.90% and 6.40% were used for determination

of costs in 2004 and 2003, respectively.

(b) For 2006, gradually declining to 5% for 2013 and thereafter.

To determine the expected long-term rate of return on retiree

life plan assets, we consider the current and expected asset

allocations, as well as historical and expected returns on various

categories of plan assets. We apply our expected rate of return

to a market-related value of assets, which stabilizes variability in

assets to which we apply that expected return.

We amortize experience gains and losses, as well as the

effects of changes in actuarial assumptions and plan provisions,

over a period no longer than the average future service of

employees.

FUNDING POLICY. We fund retiree health benefits on a pay-as-

you-go basis. We expect to contribute approximately $700 million

in 2007 to fund such benefits. We fund retiree life insurance

benefits at our discretion.

Changes in the accumulated postretirement benefi t obligation

for retiree benefit plans follow.

ACCUMULATED POSTRETIREMENT BENEFIT OBLIGATION (APBO)

(In millions) 2006 2005

Balance at January 1 $9,084 $9,250

Service cost for benefi ts earned 229 243

Interest cost on benefi t obligation 455 507

Participant contributions 43 41

Actuarial gain (707) (55)

Benefi ts paid(a) (810) (856)

Other (32) (46)

Balance at December 31(b) $8,262 $9,084

(a) Net of Medicare Part D subsidy of $75 million in 2006.

(b) The APBO for the retiree health plans was $6,001 million and $6,713 million at

year-end 2006 and 2005, respectively.

Increasing or decreasing the healthcare cost trend rates by one

percentage point would have had an insignificant effect on the

December 31, 2006, accumulated postretirement benefi t obliga-

tion and the annual cost of retiree health plans. Our principal

retiree benefit plans are collectively bargained and have provisions

that limit our per capita costs.

Changes in the fair value of assets for retiree benefi t plans

follow.

FAIR VALUE OF PLAN ASSETS

(In millions) 2006 2005

Balance at January 1 $1,619 $1,652

Actual gain on plan assets 222 107

Employer contributions 636 675

Participant contributions 43 41

Benefi ts paid(a) (810) (856)

Balance at December 31 $1,710 $1,619

(a) Net of Medicare Part D subsidy of $75 million in 2006.

Plan assets are held in trust, as follows:

PLAN ASSET ALLOCATION

2006 2005

Target Actual Actual

December 31 allocation allocation allocation

U.S. equity securities 35–55% 44% 51%

Non-U.S. equity securities 15–25 22 19

Debt securities 15–30 18 20

Real estate 1–10 4 2

Private equities 1–11 3 1

Other 1–13 9 7

Total 100% 100%

Plan fiduciaries set investment policies and strategies for the trust.

Long-term strategic investment objectives include preserving

the funded status of the plan and balancing risk and return.

The plan fiduciaries oversee the investment allocation process,

which includes selecting investment managers, setting long-term

strategic targets and monitoring asset allocations. Target alloca-

tion ranges are guidelines, not limitations, and occasionally plan

fiduciaries will approve allocations above or below a target range.

80 ge 2006 annual report