Kohl's 2012 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2012 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

19

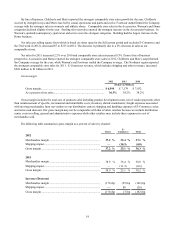

By line of business, Children's and Men's reported the strongest comparable store sales growth for the year. Children's

was led by strength in toys and Men's was led by casual sportswear and pants and active. Footwear outperformed the Company

average with the strongest sales in women's and athletic shoes. Comparable store sales in the Accessories, Women's and Home

categories declined slightly for the year. Sterling silver jewelry reported the strongest increase in the Accessories business. In

Women's, updated/contemporary sportswear and active were the strongest categories. Bedding had the largest increase in the

Home business.

Net sales per selling square foot (which is based on stores open for the full current period and excludes E-Commerce and

the 53rd week in 2012), decreased $7 to $213 in 2012. The decrease is primarily due to a 2% decrease in sales at our

comparable stores.

Net sales for 2011 increased 2.2% over 2010 and comparable store sales increased 0.5%. From a line of business

perspective, Accessories and Home reported the strongest comparable store sales in 2011. Children's and Men’s outperformed

the Company average for the year, while Women's and Footwear trailed the Company average. The Northeast region reported

the strongest comparable store sales for 2011. E-Commerce revenue, which includes shipping and other revenues, increased

$269 million to $1 billion in 2011.

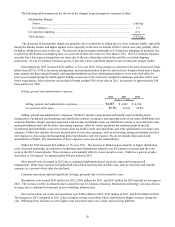

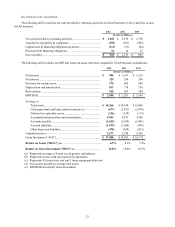

Gross margin.

2012 2011 2010

(Dollars in Millions)

Gross margin........................................................................................ $ 6,990 $ 7,179 $ 7,032

As a percent of net sales...................................................................... 36.3% 38.2% 38.2%

Gross margin includes the total cost of products sold, including product development costs, net of vendor payments other

than reimbursement of specific, incremental and identifiable costs; inventory shrink; markdowns; freight expenses associated

with moving merchandise from our vendors to our distribution centers; shipping and handling expenses of E-Commerce sales;

and terms cash discount. Our gross margin may not be comparable with that of other retailers because we include distribution

center costs in selling, general and administrative expenses while other retailers may include these expenses in cost of

merchandise sold.

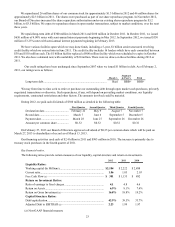

The following table summarizes gross margin as a percent of sales by channel:

Stores E-

Commerce Total

2012

Merchandise margin....................................................................... 37.2 % 35.4 % 37.1 %

Shipping impact.............................................................................. —(10.3)(0.8)

Gross margin .................................................................................. 37.2 % 25.1 % 36.3 %

2011

Merchandise margin....................................................................... 38.9 % 36.4 % 38.8 %

Shipping impact.............................................................................. —(11.3)(0.6)

Gross margin .................................................................................. 38.9 % 25.1 % 38.2 %

Increase (Decrease)

Merchandise margin....................................................................... (176) bp (95) bp (166) bp

Shipping impact.............................................................................. —88 (26)

Gross margin .................................................................................. (176) bp (7) bp (192) bp