Kohl's 2012 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 2012 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

29

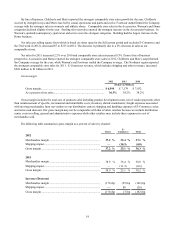

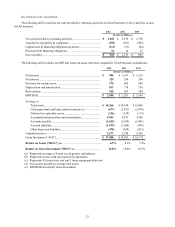

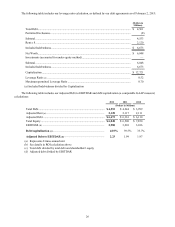

could also have an impact on estimated reserves. Historically, our actuarial estimates have not been materially different from

actual results.

We are fully self-insured for employee-related health care benefits, a portion of which is paid by our associates. We use a

third-party actuary to estimate the liability for incurred, but not reported, health care claims. This estimate uses historical claims

information as well as estimated health care trends. As of February 2, 2013, we had recorded approximately $14 million for

medical, pharmacy and dental claims which were incurred in 2012 and expected to be paid in 2013. Historically, our actuarial

estimates have not been materially different from actual results.

Effective January 1, 2012, we are self-insured for a portion of our property losses. Reserves related to property losses

were not significant as of February 2, 2013.

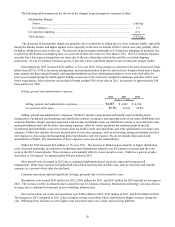

Impairment of Assets

As of February 2, 2013, our investment in buildings and improvements, before accumulated depreciation, was $14

billion. We review these buildings and improvements for impairment when an event or changes in circumstances, such as

decisions to close a store or significant operating losses, indicate the carrying value of the asset may not be recoverable.

For operating stores, a potential impairment has occurred if the fair value of a specific store is less than the net carrying

amount of the assets. If required, we would record an impairment loss equal to the amount by which the carrying amount of the

asset exceeds its fair value.

Identifying impaired assets and quantifying the related impairment loss, if any, requires significant estimates by

management. The most significant of these estimates is the cash flow expected to result from the use and eventual disposition

of the asset. When determining the stream of projected future cash flows associated with an individual store, management

estimates future store performance including sales growth rates, gross margin and controllable expenses, such as store payroll

and occupancy expense. Projected cash flows must be estimated for future periods throughout the remaining life of the

property, which may be as many as 40 years in the future. The accuracy of these estimates will be impacted by a number of

factors including general economic conditions, changes in competitive landscape and our ability to effectively manage the

operations of the store.

We have not historically experienced any significant impairment of long-lived assets. Additionally, impairment of an

individual building and related improvements, net of accumulated depreciation, would not generally be material to our financial

results.

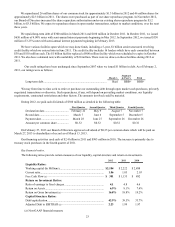

Income Taxes

We regularly evaluate the likelihood of realizing the benefit for income tax positions we have taken in various federal and

state filings by considering all relevant facts, circumstances and information available to us. If we believe it is more likely than

not that our position will be sustained, we recognize a benefit at the largest amount which we believe is cumulatively greater

than 50% likely to be realized. Our unrecognized tax benefit, excluding accrued interest and penalties, was $108 million as of

February 2, 2013 and $101 million as of January 28, 2012.

Unrecognized tax benefits require significant management judgment regarding applicable statutes and their related

interpretation, the status of various income tax audits and our particular facts and circumstances. Also, as audits are completed

or statutes of limitations lapse, it may be necessary to record adjustments to our taxes payable, deferred tax assets, tax reserves

or income tax expense. Although we believe we have adequately reserved for our uncertain tax positions, no assurance can be

given that the final tax outcome of these matters will not be different.

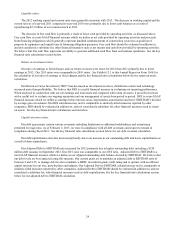

Operating Leases

As of February 2, 2013, 739 of our 1,146 retail stores were subject to either a ground or building lease. Accounting for

leased properties requires compliance with technical accounting rules and significant judgment by management. Application of

these accounting rules and assumptions made by management will determine whether we are considered the owner for

accounting purposes or whether the lease is accounted for as a capital or operating lease in accordance with ASC 840,

“Leases.”

If we are considered the owner for accounting purposes or the lease is considered a capital lease, we record the property

and a related financing or capital lease obligation on our balance sheet. The asset is then depreciated over its expected lease

term. Rent payments for these properties are recognized as interest expense and a reduction of the financing or capital lease

obligation.