Kohl's 2012 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2012 Kohl's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

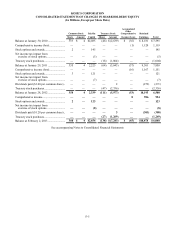

KOHL’S CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

F-13

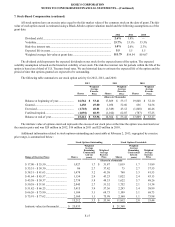

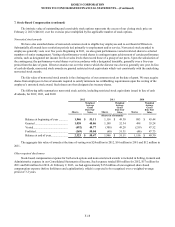

2. Debt (continued)

In October 2011, we issued $650 million of 4.00% notes with semi-annual interest payments beginning May 2012. The

notes mature on November 1, 2021. In anticipation of this debt issuance, we entered into interest rate hedges in December 2010

and May 2011 to hedge our exposure to the risk of increases in interest rates on $400 million of debt. In conjunction with the

debt issuance, we paid $48 million, the fair market value of the hedges, to settle the hedges. The unrealized loss on the hedges

is recognized as interest expense at a rate of $5 million per year over the ten-year life of the debt.

We have various facilities upon which we may draw funds, including a five-year, $1 billion senior unsecured revolving

credit facility which we entered into in June 2011. The credit facility includes 16 lenders which have each committed between

$30 million and $110 million. We also have a demand note with availability of $30 million. There were no draws on these

facilities during 2012 or 2011.

Our debt agreements contain various covenants including limitations on additional indebtedness and certain financial

tests. As of February 2, 2013, we were in compliance with all covenants of the debt agreements.

We also have outstanding trade letters of credit and stand-by letters of credit totaling approximately $76 million at

February 2, 2013, issued under uncommitted lines with two banks.

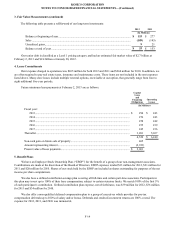

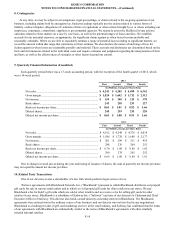

3. Fair Value Measurements

ASC No. 820, “Fair Value Measurements and Disclosures,” requires fair value measurements be classified and disclosed

in one of the following pricing categories:

Level 1: Financial instruments with unadjusted, quoted prices listed on active market exchanges.

Level 2:

Financial instruments lacking unadjusted, quoted prices from active market exchanges, including over-the-

counter traded financial instruments. The prices for the financial instruments are determined using prices

for recently traded financial instruments with similar underlying terms as well as directly or indirectly

observable inputs, such as interest rates and yield curves that are observable at commonly quoted intervals.

Level 3:

Financial instruments that are not actively traded on a market exchange. This category includes situations

where there is little, if any, market activity for the financial instrument. The prices are determined using

significant unobservable inputs or valuation techniques.

Our cash and cash equivalents are classified as a Level 1 pricing category. The carrying value of our cash and cash

equivalents approximates fair value because maturities are three months or less.

Our long-term investments consist primarily of investments in auction rate securities (“ARS”). The par value of our

long-term investments was $84 million as of February 2, 2013 and $193 million as of January 28, 2012. The estimated fair

value of these securities was $53 million as of February 2, 2013 and $153 million as of January 28, 2012.

All ARS are classified as a Level 3 pricing category. The fair value for our ARS were based on third-party pricing

models which utilized a discounted cash flow model for each of the securities as there was no recent activity in the secondary

markets in these types of securities. This model used a combination of observable inputs which were developed using publicly

available market data obtained from independent sources and unobservable inputs that reflect our own estimates of the

assumptions that market participants would use in pricing the investments. Observable inputs include interest rate currently

being paid, maturity and credit ratings.

Unobservable inputs include expected redemption date and discount rate. We assumed a seven-year redemption period

in valuing our ARS. We intend to hold our ARS until maturity or until we can liquidate them at par value. Based on our other

sources of income, we do not believe we will be required to sell them before recovery of par value. In some cases, holding the

security until recovery may mean until maturity, which ranges from 2037 to 2039. The discount rate was calculated using the

closest match available for other insured asset backed securities. Discount rates ranged from 8.13% to 10.83%. The weighted-

average discount rate was 9.12%. A market failure scenario was employed as recent successful auctions of these securities

were very limited. Assuming a longer redemption period and a higher discount rate would result in a lower fair market value.

Similarly, assuming a shorter redemption period and a lower discount rate would result in a higher fair market value.