McDonalds 2012 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2012 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

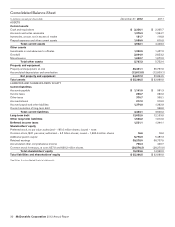

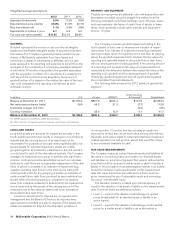

in foreign currency exchange rates, net property and equipment

increased $1.4 billion primarily due to capital expenditures, partly

offset by depreciation.

Operating income is used to compute return on average

assets, while net income is used to calculate return on average

common equity. Month-end balances are used to compute both

average assets and average common equity.

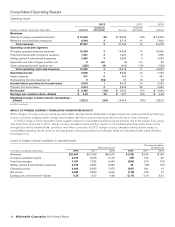

2012 2011 2010

Return on average assets 25.4% 26.0% 24.7%

Return on average common

equity 37.5 37.7 35.3

In 2012, return on average assets and return on average

common equity decreased due to the negative impact of foreign

currency translation primarily on operating income and net

income. In 2011, return on average assets and return on average

common equity benefited from strong global operating results

and the positive impact of foreign currency translation. Operating

income, as reported, does not include interest income; however,

cash balances are included in average assets. The inclusion of

cash balances in average assets reduced return on average

assets by about two percentage points for all years presented.

FINANCING AND MARKET RISK

The Company generally borrows on a long-term basis and is

exposed to the impact of interest rate changes and foreign cur-

rency fluctuations. Debt obligations at December 31, 2012

totaled $13.6 billion, compared with $12.5 billion at

December 31, 2011. The net increase in 2012 was primarily due

to net issuances of $1.2 billion.

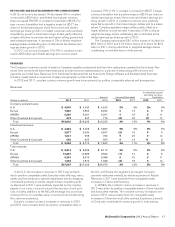

Debt highlights(1)

2012 2011 2010

Fixed-rate debt as a percent of total

debt(2,3) 74% 69% 66%

Weighted-average annual interest rate of

total debt(3) 4.0 4.2 4.3

Foreign currency-denominated debt as a

percent of total debt(2) 36 40 41

Total debt as a percent of total

Capitalization (total debt and total

Shareholders’ equity)(2) 47 46 44

Cash provided by operations as a percent

of total debt(2) 51 57 55

(1) All percentages are as of December 31, except for the weighted-average annual

interest rate, which is for the year.

(2) Based on debt obligations before the effect of fair value hedging adjustments. This

effect is excluded as these adjustments have no impact on the obligation at maturity.

See Debt financing note to the consolidated financial statements.

(3) Includes the effect of interest rate swaps.

Fitch, Standard & Poor’s and Moody’s currently rate, with a

stable outlook, the Company’s commercial paper F1, A-1 and

P-1, respectively; and its long-term debt A, A and A2,

respectively.

Certain of the Company’s debt obligations contain cross-

acceleration provisions and restrictions on Company and

subsidiary mortgages and the long-term debt of certain sub-

sidiaries. There are no provisions in the Company’s debt

obligations that would accelerate repayment of debt as a result of

a change in credit ratings or a material adverse change in the

Company’s business. Under existing authorization from the

Company’s Board of Directors, at December 31, 2012, the

Company had $5.4 billion of authority remaining to borrow funds,

including through (i) public or private offering of debt securities;

(ii) direct borrowing from banks or other financial institutions; and

(iii) other forms of indebtedness. In addition to debt securities

available through a medium-term notes program registered with

the U.S. Securities and Exchange Commission (“SEC”) and a

Global Medium-Term Notes program, the Company has $1.5 bil-

lion available under committed line of credit agreements as well

as authority to issue commercial paper in the U.S. and global

markets (see Debt Financing note to the consolidated financial

statements appearing elsewhere herein). Debt maturing in 2013

is approximately $690 million of long-term corporate debt. In

2013, the Company expects to issue commercial paper and long-

term debt to refinance this maturing debt. As of December 31,

2012, the Company also had $581 million of foreign currency

borrowings outstanding primarily under uncommitted line of

credit agreements.

The Company uses major capital markets, bank financings

and derivatives to meet its financing requirements and reduce

interest expense. The Company manages its debt portfolio in

response to changes in interest rates and foreign currency rates

by periodically retiring, redeeming and repurchasing debt, termi-

nating swaps and using derivatives. The Company does not use

derivatives with a level of complexity or with a risk higher than the

exposures to be hedged and does not hold or issue derivatives

for trading purposes. All swaps are over-the-counter instruments.

In managing the impact of interest rate changes and foreign

currency fluctuations, the Company uses interest rate swaps and

finances in the currencies in which assets are denominated. The

Company uses foreign currency debt and derivatives to hedge

the foreign currency risk associated with certain royalties, inter-

company financings and long-term investments in foreign

subsidiaries and affiliates. This reduces the impact of fluctuating

foreign currencies on cash flows and shareholders’ equity. Total

foreign currency-denominated debt was $4.9 billion and

$5.0 billion for the years ended December 31, 2012 and 2011,

respectively. In addition, where practical, the Company’s restau-

rants purchase goods and services in local currencies resulting in

natural hedges. See Summary of significant accounting policies

note to the consolidated financial statements related to financial

instruments and hedging activities for additional information

regarding the accounting impact and use of derivatives.

The Company does not have significant exposure to any

individual counterparty and has master agreements that contain

netting arrangements. Certain of these agreements also require

each party to post collateral if credit ratings fall below, or

aggregate exposures exceed, certain contractual limits. At

December 31, 2012, neither the Company nor its counterparties

were required to post collateral on any derivative position, other

than on hedges of certain of the Company’s supplemental benefit

plan liabilities where our counterparty was required to post

collateral on its liability position.

24 McDonald’s Corporation 2012 Annual Report