McDonalds 2012 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2012 McDonalds annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

|

|

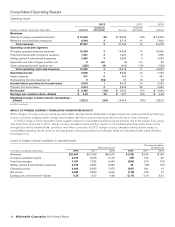

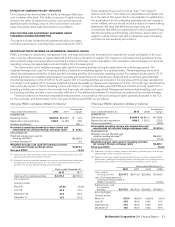

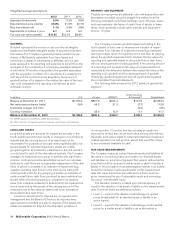

The Company’s net asset exposure is diversified among a

broad basket of currencies. The Company’s largest net asset

exposures (defined as foreign currency assets less foreign cur-

rency liabilities) at year end were as follows:

Foreign currency net asset exposures

In millions of U.S. Dollars 2012 2011

Euro $6,692 $5,905

Australian Dollars 2,450 2,409

Canadian Dollars 1,319 1,224

British Pounds Sterling 1,117 726

Russian Ruble 651 594

The Company prepared sensitivity analyses of its financial

instruments to determine the impact of hypothetical changes in

interest rates and foreign currency exchange rates on the

Company’s results of operations, cash flows and the fair value of

its financial instruments. The interest rate analysis assumed a one

percentage point adverse change in interest rates on all financial

instruments, but did not consider the effects of the reduced level

of economic activity that could exist in such an environment. The

foreign currency rate analysis assumed that each foreign currency

rate would change by 10% in the same direction relative to the

U.S. Dollar on all financial instruments; however, the analysis did

not include the potential impact on revenues, local currency prices

or the effect of fluctuating currencies on the Company’s antici-

pated foreign currency royalties and other payments received in

the U.S. Based on the results of these analyses of the Company’s

financial instruments, neither a one percentage point adverse

change in interest rates from 2012 levels nor a 10% adverse

change in foreign currency rates from 2012 levels would materi-

ally affect the Company’s results of operations, cash flows or the

fair value of its financial instruments.

LIQUIDITY

The Company has significant operations outside the United

States where we earn over 60% of our operating income. A sig-

nificant portion of these historical earnings are considered to be

indefinitely reinvested in foreign jurisdictions where the Company

has made, and will continue to make, substantial investments to

support the ongoing development and growth of our international

operations. Accordingly, no U.S. federal or state income taxes

have been provided on the undistributed foreign earnings. The

Company’s cash and equivalents held by our foreign subsidiaries

totaled approximately $2.1 billion as of December 31, 2012. We

do not intend, nor do we foresee a need, to repatriate these funds.

Consistent with prior years, we expect existing domestic cash

and equivalents, domestic cash flows from operations, annual

repatriation of a portion of the current period’s foreign earnings,

and the issuance of domestic debt to continue to be sufficient to

fund our domestic operating, investing, and financing activities.

We also continue to expect existing foreign cash and equivalents

and foreign cash flows from operations to be sufficient to fund

our foreign operating, investing, and financing activities.

In the future, should we require more capital to fund activities

in the United States than is generated by our domestic oper-

ations and is available through the issuance of domestic debt, we

could elect to repatriate a greater portion of future periods’ earn-

ings from foreign jurisdictions. This could also result in a higher

effective tax rate in the future.

While the likelihood is remote, to the extent foreign cash is

available, the Company could also elect to repatriate earnings

from foreign jurisdictions that have previously been considered to

be indefinitely reinvested. Upon distribution of those earnings in

the form of dividends or otherwise, the Company may be subject

to additional U.S. income taxes (net of an adjustment for foreign

tax credits) which could result in a use of cash. This could also

result in a higher effective tax rate in the period in which such a

determination is made to repatriate prior period foreign earnings.

Refer to the Income Taxes note to the consolidated financial

statements appearing elsewhere herein for further information

related to our income taxes and the undistributed earnings of the

Company’s foreign subsidiaries.

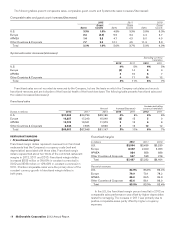

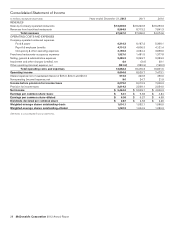

CONTRACTUAL OBLIGATIONS AND COMMITMENTS

The Company has long-term contractual obligations primarily in

the form of lease obligations (related to both Company-operated

and franchised restaurants) and debt obligations. In addition, the

Company has long-term revenue and cash flow streams that

relate to its franchise arrangements. Cash provided by operations

(including cash provided by these franchise arrangements) along

with the Company’s borrowing capacity and other sources of

cash will be used to satisfy the obligations. The following table

summarizes the Company’s contractual obligations and their

aggregate maturities as well as future minimum rent payments

due to the Company under existing franchise arrangements as of

December 31, 2012. See discussions of cash flows and financial

position and capital resources as well as the Notes to the con-

solidated financial statements appearing elsewhere herein for

further details.

Contractual cash outflows Contractual cash inflows

In millions Operating

leases Debt

obligations(1) Minimum rent under

franchise arrangements

2013 $ 1,352 $ 2,562

2014 1,259 $ 659 2,484

2015 1,130 1,168 2,382

2016 1,020 2,437 2,261

2017 918 1,053 2,130

Thereafter 6,844 8,273 17,047

Total $12,523 $13,590 $28,866

(1) The maturities reflect reclassifications of short-term obligations to long-term obliga-

tions of $1.5 billion, as they are supported by a long-term line of credit agreement

expiring in November 2016. Debt obligations do not include $42 million of noncash

fair value hedging adjustments or $217 million of accrued interest.

The Company maintains certain supplemental benefit plans

that allow participants to (i) make tax-deferred contributions and

(ii) receive Company-provided allocations that cannot be made

under the qualified benefit plans because of IRS limitations. At

December 31, 2012, total liabilities for the supplemental plans

were $493 million, and total liabilities for gross unrecognized tax

benefits were $482 million.

There are certain purchase commitments that are not recog-

nized in the consolidated financial statements and are primarily

related to construction, inventory, energy, marketing and other

service related arrangements that occur in the normal course of

business. The amounts related to these commitments are not

significant to the Company’s financial position. Such commit-

ments are generally shorter term in nature and will be funded

from operating cash flows.

McDonald’s Corporation 2012 Annual Report 25