Microsoft 2012 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2012 Microsoft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

|

|

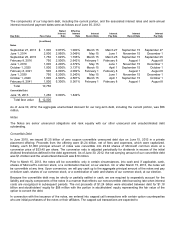

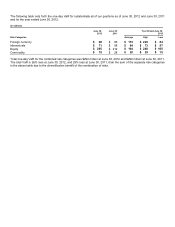

The components of our long-term debt, including the current portion, and the associated interest rates and semi-annual

interest record and payment dates were as follows as of June 30, 2012:

Due Date

Face Value

Stated

Interest

Rate

Effective

Interest

Rate

Interest

Record Date

Interest

Pay Date

Interest

Record Date

Interest

Pay Date

(In millions)

Notes

September 27, 2013

$

1,000

0.875%

1.000%

March 15

March 27

September 15

September 27

June 1, 2014

2,000

2.950%

3.049%

May 15

June 1

November 15

December 1

September 25, 2015

1,750

1.625%

1.795%

March 15

March 25

September 15

September 25

February 8, 2016

750

2.500%

2.642%

February 1

February 8

August 1

August 8

June 1, 2019

1,000

4.200%

4.379%

May 15

June 1

November 15

December 1

October 1, 2020

1,000

3.000%

3.137%

March 15

April 1

September 15

October 1

February 8, 2021

500

4.000%

4.082%

February 1

February 8

August 1

August 8

June 1, 2039

750

5.200%

5.240%

May 15

June 1

November 15

December 1

October 1, 2040

1,000

4.500%

4.567%

March 15

April 1

September 15

October 1

February 8, 2041

1,000

5.300%

5.361%

February 1

February 8

August 1

August 8

Total

10,750

Convertible Debt

June 15, 2013

1,250

0.000%

1.849%

Total face value

$

12,000

As of June 30, 2012, the aggregate unamortized discount for our long-term debt, including the current portion, was $56

million.

Notes

The Notes are senior unsecured obligations and rank equally with our other unsecured and unsubordinated debt

outstanding.

Convertible Debt

In June 2010, we issued $1.25 billion of zero coupon convertible unsecured debt due on June 15, 2013 in a private

placement offering. Proceeds from the offering were $1.24 billion, net of fees and expenses, which were capitalized.

Initially, each $1,000 principal amount of notes was convertible into 29.94 shares of Microsoft common stock at a

conversion price of $33.40 per share. The conversion ratio is adjusted periodically for dividends in excess of the initial

dividend threshold as defined in the debt agreement. As of June 30, 2012, the net carrying amount of our convertible debt

was $1.2 billion and the unamortized discount was $19 million.

Prior to March 15, 2013, the notes will be convertible, only in certain circumstances, into cash and, if applicable, cash,

shares of Microsoft’s common stock, or a combination thereof, at our election. On or after March 15, 2013, the notes will

be convertible at any time. Upon conversion, we will pay cash up to the aggregate principal amount of the notes and pay

or deliver cash, shares of our common stock, or a combination of cash and shares of our common stock, at our election.

Because the convertible debt may be wholly or partially settled in cash, we are required to separately account for the

liability and equity components of the notes in a manner that reflects our nonconvertible debt borrowing rate when interest

costs are recognized in subsequent periods. The net proceeds of $1.24 billion were allocated between debt for $1.18

billion and stockholders’ equity for $58 million with the portion in stockholders’ equity representing the fair value of the

option to convert the debt.

In connection with the issuance of the notes, we entered into capped call transactions with certain option counterparties

who are initial purchasers of the notes or their affiliates. The capped call transactions are expected to