Safeway 1998 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 1998 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

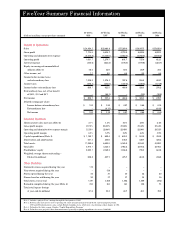

Capital Expenditure Program

A component of Safeway’s long-term strategy is its capital

expenditure program. The Company’s capital expenditure

program funds, among other things, new stores, remodels,

manufacturing plants, distribution facilities, and information

technology advances. In the last several years, Safeway man-

agement has significantly strengthened its program to select

and approve new capital investments, resulting in improved

returns on investment.

The table below reconciles cash paid for pro p e rty additions

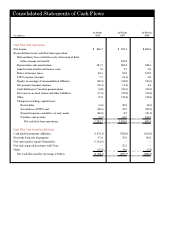

reflected in the Consolidated Statements of Cash Flows to

S a f e w a y ’s broader definition of capital expenditures, and also

details changes in the Company’s store base during such period:

Improved operations and lower project costs have raised

the return on capital projects, allowing Safeway to increase

capital expenditures to $1.2 billion in 1998 and open 46 stores,

remodel 234 stores and complete construction of the new dis-

tribution center in Maryland. In 1999, Safeway expects to

spend approximately $1.2 billion and open 55 to 60 new store s

and complete approximately 250 remodels.

(Dollars in millions) 1998 1997 1996

Cash paid for property

additions $1,075.2 $758.2 $541.8

Less: Purchases of

previously leased

properties (35.7) (28.2) (13.2)

Plus: Present value of all lease

obligations incurred 117.4 91.3 91.7

Mortgage notes assumed

in property acquisitions 32.8 0.9 –

Vons first-quarter

expenditures –7.2 –

■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■■ ■ ■ ■ ■ ■ ■

Total capital expenditures $1,189.7 $829.4 $620.3

■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■ ■■ ■ ■ ■ ■ ■ ■

Capital expenditures as

a percent of sales 4.9% 3.7% 3.6%

Dominick’s stores acquired 113 – –

Vons stores acquired –316 –

Stores opened 46 37 30

Stores closed or sold 30 37 37

Remodels (Note 1) 234 181 141

Total retail square footage

at year-end (in millions) 61.6 53.2 40.7

Note 1: Defined as store projects (other than maintenance) generally requiring

expenditures in excess of $200,000.

Performance-Based Compensation

The Company has perf o rmance-based compensation plans

that cover approximately 12,000 management and pro f e s s i o n a l

employees. Perf o rmance-based compensation plans set overall

bonus levels based upon both operating results and working

capital management. Individual bonuses are based on job

p e rf o rmance. Certain employees are covered by capital invest-

ment bonus plans which measure the performance of capital

projects based on operating performance over several years.

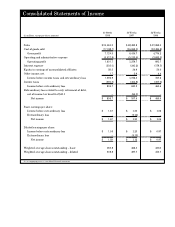

Market Risk from Financial Instruments

Safeway manages interest rate risk through the strategic

use of fixed and variable interest rate debt and, to a limited

extent, interest rate derivatives. At year-end 1998,

S a f e w a y ’s derivative instruments consisted of interest rate

cap agreements and an interest rate swap agreement. The

cap agreements expire in May 1999, and entitle Safeway

to receive the excess of LIBOR over 7% on an $850 million

notional amount. Under the swap agreement, which expires

in the year 2007, Safeway pays interest of 6.2% on a $100 mil-

lion notional amount and receives a variable interest rate

based on Federal Reserve rates quoted for commercial paper.

No derivatives are held for trading purposes.

The following table provides information by year of maturi-

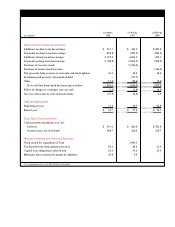

ty about the Company’s other financial instruments that are

sensitive to interest rate changes:

(Dollars in millions) 1999 2000 2001 2002 2003 Thereafter

C o m m e rcial paper:

P r i n c i p a l – – – $1 , 7 4 5 . 1 – –

Weighted a v e r a g e

interest rate – – – 5 . 9 9 % – –

Bank borro w i n g s :

P r i n c i p a l $ 1 6 1 . 8 – – $ 8 9 . 1 – –

Weighted average

interest rate 5 . 8 0 % – – 5 . 5 7 % – –

L o n g - t e rm debt:*

P r i n c i p a l $ 1 1 8 . 0 $ 4 2 7 . 5 $ 5 4 9 . 6 $ 3 7 . 8 $ 3 7 7 . 6 $1 , 0 1 5 . 9

Weighted average

interest rate 8 . 9 7 % 5 . 9 3 % 6 . 8 8 % 8 . 9 5 % 6 . 2 8 % 7 . 2 2 %

*Primarily fixed rate debt