Safeway 1998 Annual Report Download - page 29

Download and view the complete annual report

Please find page 29 of the 1998 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

-

41

-

42

-

43

-

44

|

|

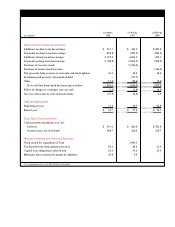

Self-Insurance The Company is primarily self-insured for

workers’ compensation, automobile and general liability costs.

The self-insurance liability is determined actuarially, based

on claims filed and an estimate of claims incurred but not yet

reported. The present value of such claims was accrued using

a discount rate of 5.5% in 1998 and 1997. The current portion

of the self-insurance liability of $107.3 million at year-end 1998

and $96.3 million at year-end 1997 is included in other accrued

liabilities in the consolidated balance sheets. The long-term

portion of $265.5 million at year-end 1998 and $230.7 million

at year-end 1997 is included in accrued claims and other liabili-

ties. Claims payments were $98.2 million in 1998, $100.0 million

in 1997 and $66.7 million in 1996. The total undiscounted liabili-

ty was $413.1 million at year-end 1998 and $365.5 million at

year-end 1997.

Income Taxes The Company provides a deferred tax expense or

benefit equal to the change in the deferred tax liability during

the year in accordance with Statement of Financial Accounting

Standards (“SFAS”) No. 109, “Accounting for Income Taxes.”

D e f e rred income taxes re p resent tax credit carry f o rw a r ds

and future net tax effects resulting from temporary diff e re n c e s

between the financial statement and tax basis of assets and

liabilities using enacted tax rates in effect for the year in which

the differences are expected to reverse.

Statement of Cash Flows Short-term investments with original

maturities of less than three months are considered to be cash

equivalents. Borrowings with original maturities of less than

three months are presented net of related repayments.

Off-Balance Sheet Financial Instruments As discussed in NoteE,

the Company has entered into interest rate swap and cap

a g reements to limit the Company’s exposure to changes in

market interest rates. Interest rate swap agreements involve

the exchange with a counterparty of fixed and floating-rate

interest payments periodically over the life of the agreements

without exchange of the underlying notional principal amounts.

The differential to be paid or received is recognized over the

life of the agreements as an adjustment to interest expense.

I n t e rest rate cap agreements lock in a maximum intere s t

rate on a notional principal amount by paying a fee to a coun-

t e r p a rty in exchange for the counterpart y ’s promise to pay

to Safeway the diff e rence between a fixed rate and a floating

rate of interest. The fee paid to the counterparty is deferre d

and amortized as an adjustment to interest expense over the

life of the agreement.

The Company’s counterparties are major financial institutions.

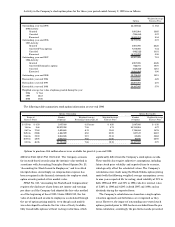

Fair Value of Financial Instruments Generally accepted accounting

principles re q u i re the disclosure of the fair value of cert a i n

financial instruments, whether or not recognized in the balance

sheet, for which it is practicable to estimate fair value.

Safeway estimated the fair values presented below using

a p p ropriate valuation methodologies and market inform a t i o n

available as of year-end. Considerable judgment is re q u i red to

develop estimates of fair value, and the estimates presented

a re not necessarily indicative of the amounts that the Company

could realize in a current market exchange. The use of diff e re n t

market assumptions or estimation methodologies could have a

material effect on the estimated fair values. Additionally, these

fair values were estimated at year-end, and current estimates of

fair value may differ significantly from the amounts presented.

The following methods and assumptions were used to esti-

mate the fair value of each class of financial instruments:

Cash and equivalents, accounts receivable, accounts payable

and short-term debt. The carrying amount of these items

approximates fair value.

Long-term debt. Market values quoted on the New York Stock

Exchange are used to estimate the fair value of publicly traded

debt. To estimate the fair value of debt issues that are not

quoted on an exchange, the Company uses those interest rates

that are currently available to it for issuance of debt with

similar terms and remaining maturities. At year-end 1998,

the estimated fair value of debt was $4.6 billion compared to a

carrying value of $4.5 billion. At year-end 1997, the estimated

fair value of debt was $3.2 billion compared to a carrying value

of $3.1 billion.

Off-balance sheet instruments. The fair value of interest rate

swap and cap agreements is the amount at which they could

be settled based on estimates obtained from dealers. At year-

end 1998 and 1997, net unrealized losses on such agre e m e n t s

w e re $7.0 million and $0.4 million.

Impairment of Long-Lived Assets When Safeway decides to

close a store or other facility, the Company accrues estimated

losses, if any, which may include lease payments or other

costs of holding the facility, net of estimated future income

(primarily sublease income) in accordance with the provisions

of SFAS No. 121, “Accounting for the Impairment of Long-

Lived Assets and for Long-Lived Assets to be Disposed of.”

Safeway had an accrued liability of $84.6 million at year- e n d

1998 and $72.0 million at year-end 1997 for the anticipated

f u t u re closure of stores and other facilities, which is included

in Accrued Claims and Other Liabilities in the Company’s

consolidated balance sheets.