Safeway 1998 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 1998 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

|

|

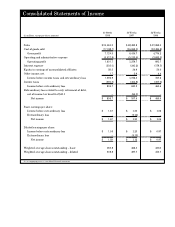

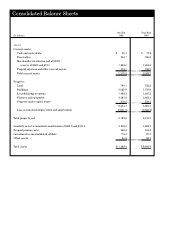

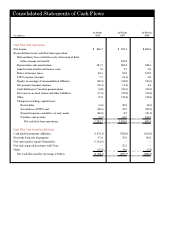

Goodwill Goodwill was $3.3 billion at year-end 1998 and $1.8 bil-

lion at year-end 1997, and is being amortized on a straight-line

basis over its estimated useful life. If it became probable that

the projected future undiscounted cash flows of acquired assets

w e re less than the carrying value of the goodwill, Safeway

would recognize an impairment loss in accordance with the

provisions of SFAS No. 121.

Goodwill amortization was $56.3 million in 1998, $41.8 mil-

lion in 1997 and $10.4 million in 1996. Goodwill and re l a t e d

a m o rtization has increased due to the Vons Merger and

Dominick’s Acquisition as discussed in Note B.

Stock-Based Compensation Safeway accounts for stock-based

a w a rds to employees using the intrinsic value method in

accordance with Accounting Principles Board Opinion No. 25,

“Accounting for Stock Issued to Employees.” The disclosure

re q u i rements of SFAS No. 123, “Accounting for Stock-Based

Compensation” are set forth in Note F.

New Accounting Standards In 1998, Safeway adopted the

American Institute of Certified Public Accountants’ (“AICPA ” )

Statement of Position 98-1 (“SOP 98-1”), “Accounting for the

Costs of Computer Software Developed or Obtained for

I n t e rnal Use.” SOP 98-1 defines the types of computer software

p roject costs that may be capitalized. All other costs must be

expensed in the period incurred. In order for costs to be capital-

ized, the computer software project must be intended to cre a t e

a new system or add identifiable functionality to an existing

system. Adoption of this statement did not have a material

impact on the Company’s consolidated financial statements.

In June 1998, the Financial Accounting Standards Board

issued SFAS No. 133, “Accounting for Derivative Instru m e n t s

and Hedging Activities,” which defines derivatives, requires

that derivatives be carried at fair value, and provides for

hedge accounting when certain conditions are met. This state-

ment is effective for Safeway beginning in the year 2000.

Although Safeway has not fully assessed the implications of

this new statement, the Company believes adoption of this

statement will not have a material impact on its consolidated

financial statements.

In April 1998, the AICPA finalized SOP 98-5, “Report i n go n

the Costs of Start-Up Activities,” which re q u i res that costs

i n c u rred for start-up activities, such as store openings, be

expensed as incurred. This SOP, which is effective in the first

quarter of 1999, is not expected to have a material impact on

Safeway’s consolidated financial statements.

Note B: Acquisitions

In November 1998, Safeway completed its acquisition of all of

the outstanding shares of Dominick’s for $49 cash per share ,

or a total of approximately $1.2 billion. The Dominick’s acqui-

sition was accounted for as a purchase and resulted in addi-

tional goodwill of $1.6 billion which is being amortized over

40 years. Safeway funded the Dominick’s Acquisition, includ-

ing the repayment of approximately $560 million of debt and

lease obligations, with a combination of bank borrowings and

c o m m e rcial paper.

In April 1997, Safeway completed the Vons Merger pur-

suant to which the Company issued 83.2 million shares of

Safeway common stock valued at $1.7 billion for all of the

s h a res of Vons common stock that it did not already own. The

Vons Merger was accounted for as a purchase and resulted in

additional goodwill of $1.5 billion which is being amortized over

40 years. In connection with the Vons Merger, Safeway repur-

chased 64.0 million shares of its common stock from a partner-

ship affiliated with KKR & Co., L.L.C. (“KKR”) at $21.50 per

share, for an aggregate purchase price of $1.376 billion.

Safeway funded the repurchase with bank borrowings.

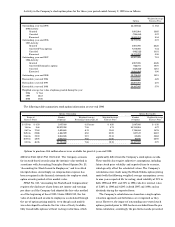

The following unaudited pro forma combined summary

financial information is based on the historical consolidated

results of operations of Safeway, Vons and Dominick’s, as if

the Vons Merger and the Dominick’s Acquisition had occurre d

as of the beginning of each year presented. This pro form a

financial information is presented for informational purposes

only and may not be indicative of what the actual consolidated

results of operations would have been if the acquisitions had

been effective as of the beginning of the years presented. Pro

forma adjustments were applied to the respective historical

financial statements to account for the Vons Merger and

the Dominick’s Acquisition as purchases. Under purc h a s e

accounting, the purchase price is allocated to acquired assets

and liabilities based on their estimated fair values at the date

of acquisition, and any excess is allocated to goodwill.

For Dominick’s, such allocations are subject to adjustment

when additional analysis concerning asset and liability balances

is finalized. The preliminary allocation of the purchase price to

the assets and liabilities acquired was based in part upon an

independent valuation which, in turn, was based upon certain

estimates and cash flow information provided by management.

Management does not expect the final allocations to differ

materially from the amounts presented herein.

Pro Forma

52 Weeks 53 Weeks

(In millions, expect per-share amounts) 1998 1997

Sales $26,487.6 $26,315.9

Income before extraordinary loss 742.1 510.6

Net income 742.1 423.1

Diluted earnings per share:

Income before extraord i n a ry l o s s $ 1.46 $ 1.01

Net income 1.46 0.84