Safeway 1998 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 1998 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

|

|

In August 1998, Safeway and Carrs signed a definitive

m e rger agreement in which Safeway will acquire all of the

outstanding shares of Carrs for $12.50 cash per share, or a total

of approximately $110 million. In addition, Carrs has appro x i-

mately $220 million of debt. The acquisition will be accounted

for as a purchase and will be funded initially through the

issuance of commercial paper.

The acquisition of Carrs is subject to a number of condi-

tions, including the approval of the holders of a majority of

Carrs’ outstanding shares, court approval of a consent decree

with the state of Alaska requiring the sale of six Safeway

stores and one Carrs store, and other customary closing condi-

tions. Carrs expects to schedule a shareholder meeting to vote

on the transaction in April 1999. Assuming satisfaction of all

conditions, Safeway and Carrs expect to close the transaction

shortly after receiving shareholder approval and final court

approval of the consent decree.

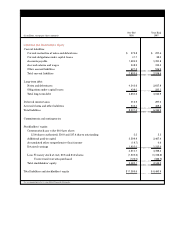

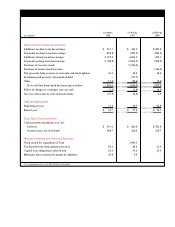

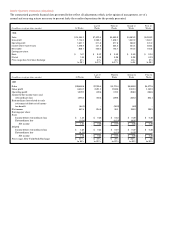

Note C: Financing

Notes and debentures were composed of the following at

year-end (in millions):

1998 1997

Commercial paper $ 1,745.0 $1,473.5

Bank credit agreement, unsecured 89.1 238.2

9.30% Senior Secured Debentures

due 2007 24.3 24.3

6.85% Senior Notes due 2004,

unsecured 200.0 200.0

7.00% Senior Notes due 2007,

unsecured 250.0 250.0

7.45% Senior Debentures due 2027,

unsecured 150.0 150.0

5.75% Notes due 2000, unsecured 400.0 –

5.875% Notes due 2001, unsecured 400.0 –

6.05% Notes due 2003, unsecured 350.0 –

6.50% Notes due 2008, unsecured 250.0 –

9.35% Senior Subordinated Notes

due 1999, unsecured 66.7 66.7

10% Senior Subordinated Notes

due 2001, unsecured 79.9 79.9

9.65% Senior Subordinated

Debentures due 2004, unsecured 81.2 81.2

9.875% Senior Subordinated

Debentures due 2007, unsecured 24.2 24.2

10% Senior Notes due 2002,

unsecured 6.1 6.1

Mortgage notes payable, secured 115.9 150.8

Other notes payable, unsecured 102.7 114.8

Medium-term notes, unsecured 25.5 25.5

Short-term bank borrowings,

unsecured 161.8 210.0

■ ■ ■ ■ ■ ■ ■ ■ ■

4,522.4 3,095.2

■ ■ ■ ■ ■ ■ ■ ■ ■

Less current maturities (279.8) (277.4)

■ ■ ■ ■ ■ ■ ■ ■ ■

Long-term portion $ 4,242.6 $2,817.8

■ ■ ■ ■ ■ ■ ■ ■ ■

Commercial Paper The amount of commercial paper borro w i n g s

is limited to the unused borrowing capacity under the bank

c redit agreement. Commercial paper is classified as long-term

because the Company intends to and has the ability to re f i-

nance these borrowings on a long-term basis through either

continued commercial paper borrowings or utilization of the

bank credit agreement, which matures in 2002. The weighted

average interest rate on commercial paper borrowings was

5.75% during 1998 and 5.99% at year-end 1998.

Bank Credit Agreement S a f e w a y ’s total borrowing capacity

under the bank credit agreement is $2.9 billion. Of the $2.9 bil-

lion credit line, $2.0 billion matures in 2002 and has two one-

year extension options, and $0.9 million is renewable annually

t h rough 2004. The restrictive covenants of the bank cre d i t

a g reement limit Safeway with respect to, among other things,

c reating liens upon its assets and disposing of material

amounts of assets other than in the ordinary course of busi-

ness. Safeway is also required to meet certain financial tests

under the bank credit agreement. At year-end 1998, the

Company had total unused borrowing capacity under the bank

c redit agreement of $ 2.7 billion ($1.0 billion excluding that por-

tion of the bank credit agreement re s e r ved to back up commer-

cial paper borrowings).

U.S. borrowings under the bank credit agreement carry

interest at one of the following rates selected by the Company:

(i) the prime rate; (ii) a rate based on rates at which Euro d o l l a r

deposits are off e red to first-class banks by the lenders in the

bank credit agreement plus a pricing margin based on the

C o m p a n y ’s debt rating or interest coverage ratio (the “Pricing

Margin”); or (iii) rates quoted at the discretion of the lenders.

Canadian borrowings denominated in U.S. dollars carry inter-

est at one of the following rates selected by the Company:

(a) the Canadian base rate; or (b) the Canadian Eurodollar rate

plus the Pricing Margin. Canadian borrowings denominated in

Canadian dollars carry interest at one of the following rates

selected by the Company: (i) the Canadian prime rate or (ii) the

rate for Canadian bankers acceptances plus the Pricing Marg i n .

The weighted average interest rate on borrowings under

the bank credit agreement was 6.69% during 1998 and 5.57%

at year-end 1998.