Safeway 1998 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 1998 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

s t o res and completed construction of a new distri-

bution center in Maryland. During 1999 we plan

to invest approximately $1.2 billion and open 55

to 60 new stores while completing some 250

remodels. As in the recent past, about thre e -

q u a rters of our capital expenditures in the com-

ing year is budgeted for new stores and re m o d e l s .

Continued Growth Through Acquisitions

While improving our store system in existing

markets will remain the central focus of our capi-

tal expenditure program, our long-term gro w t h

strategy remains focused on acquisitions.

In November 1998 we acquired Dominick’s

Supermarkets, Inc., the second largest super-

market operator in the Chicago metropolitan

area with 114 stores and sales of $2.4 billion in

fiscal 1998. As with the Vons merger in 1997,

the combination with Dominick’s enables us to

extend our geographic reach and to benefit from

the exchange of best practices. Dominick’s has an

excellent reputation in the Chicago market and

operates attractive stores in good locations. We

are confident we can build on that success.

The pending acquisition of Carr- G o t t s t e i n

Foods Co., Alaska’s leading food and drug retail-

er, is expected to result in considerable synergies

for our own Alaskan operations. In support of its

49 stores, Carrs operates the state’s largest food

warehouse and freight network.

The U.S. supermarket industry, historically

highly fragmented, is becoming increasingly con-

solidated. Whereas the top five chains had a com-

bined market share of only 19% in 1992, their

s h a re had risen to 24% in

1997, should expand to

36% this year as a result

of pending mergers and,

we believe, is likely to

increase further. Growth

through acquisition will

continue to be a key part

of our strategy.

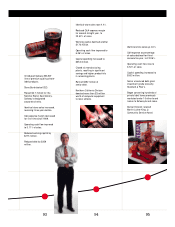

Review and Outlook

During the past six years, our total market capi-

talization has increased to approximately $29.9

billion from just $1.3 billion in 1992. No other

publicly traded supermarket chain has achieved

even half that growth rate over the same period.

Many of you have participated in this gro w t h .

As illustrated on the facing page, $1,000 invested

in Safeway stock at the beginning of 1993 had

increased in value to $18,750 by year-end 1998.

We are proud of our achievements. T h e y

reflect the dedication and hard work of 170,000

Safeway employees, many of whom are stock-

holders themselves. On their behalf, let me

a s s u re you that all of us on the Safeway team are

committed to building on our past success and

making continued progress in 1999 and beyond.

Steven A. Burd

Chairman, President and

Chief Executive Officer

March 5, 1999