Safeway 2002 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

18 SAFEWAY INC. 2002 ANNUAL REPORT

FINANCIAL REVIEW

SAFEWAY INC. AND SUBSIDIARIES

PLANNED DISPOSITION OF DOMINICK’S

In November 2002, Safeway announced its decision to sell

Dominick’s, which consists of 113 stores, and to exit the

Chicago market. In accordance with SFAS No. 144,

“Accounting for the Impairment or Disposal of Long-Lived

Assets,” Dominick’s operations are presented as a discontin-

ued operation. Accordingly, Dominick’s results are reflected separate-

ly in the Company’s consolidated financial statements and Dominick’s

information is excluded from the accompanying notes to the consolidat-

ed financial statements and the rest of the financial information includ-

ed herein, unless otherwise noted. Sales at Dominick’s were $2.4

billion in 2002, $2.5 billion in 2001 and $2.5 billion in 2000.

In accordance with SFAS No. 144, Dominick’s net assets

and liabilities have been written down to estimated fair mar-

ket value. The fair value of Dominick’s was determined by

an independent third party appraiser which primarily used

the discounted cash flow method and the guideline compa-

ny method. The final valuation of Dominick’s is dependent

upon the results of negotiations with the ultimate buyer.

Adjustment to the loss on disposition, together with any

related tax effects, will be made when additional information

is known.

STOCK REPURCHASE

In July 2002, Safeway announced that its Board of Directors

had increased the authorized level of the Company’s stock

repurchase program to $3.5 billion from the previously

announced level of $2.5 billion. During 2002, Safeway

repurchased 50.1 million shares of common stock at a cost

of $1.5 billion. From initiation of the program in 1999

through the end of 2002, Safeway had repurchased 87.0

million shares of common stock at a cost of $2.9 billion,

leaving $0.6 billion available for repurchases.

ACQUISITION OF GENUARDI’S FAMILY

MARKETS, INC. (“GENUARDI’S”)

In February 2001, Safeway acquired all of the assets of

Genuardi’s for approximately $530 million in cash (the

“Genuardi’s Acquisition”). On the acquisition date, Genuardi’s

operated 39 stores in the greater Philadelphia, Pennsylvania

area, including New Jersey and Delaware. The Genuardi’s

Acquisition was accounted for as a purchase and was funded

through the issuance of commercial paper and debentures.

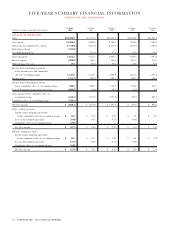

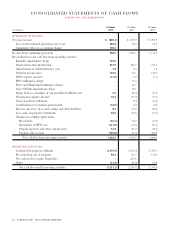

RESULTS OF OPERATIONS

CONTINUING OPERATIONS Safeway’s income from continu-

ing operations before cumulative effect of accounting

change was $568.5 million ($1.20 per share) in 2002,

$1,286.7 million ($2.51 per share) in 2001 and $1,154.2 mil-

lion ($2.26 per share) in 2000.

Safeway adopted SFAS No. 142, “Goodwill and Other

Intangible Assets,” during the first quarter of 2002 and

recorded an aggregate impairment charge of $700 million

for the cumulative effect of adopting this statement. The

charge for Dominick’s of $589 million and Randall’s of $111

million reduced the carrying value of goodwill to its implied

fair value. Impairment in both cases was due to a combina-

tion of factors including acquisition price, post-acquisition

capital expenditures and operating performance.

During the fourth quarter of 2002, Safeway performed

its annual impairment review for goodwill under SFAS No.

142. As a result of this review Safeway recorded a charge of

$704.2 million for Randall’s, which is recorded as a compo-

nent of continuing operations, and $583.8 million for

Dominick’s, which is recorded as a component of discon-

tinued operations. These charges reflect declining multiples

in the retail grocery industry and the operating perform-

ance of these divisions. Net loss after the cumulative effect

of this accounting change, discontinued operations and the

fourth-quarter goodwill impairment was $828.1 million

($1.75 per share).

In 1987, Safeway assigned a number of leases to Furr’s

Inc. (“Furr’s”) and Homeland Stores, Inc. (“Homeland”) as

part of the sale of the Company’s former El Paso, Texas and

Oklahoma City, Oklahoma divisions. Furr’s filed for Chapter

11 bankruptcy on February 8, 2001. Homeland filed for

Chapter 11 bankruptcy on August 1, 2001. Safeway is con-

tingently liable if Furr’s and Homeland are unable to contin-

ue making rental payments on these leases. In 2001, Safeway

recorded a pre-tax charge to operating and administrative

expense of $42.7 million ($0.05 per share) to recognize the

estimated lease liabilities associated with these bankruptcies

and for a single lease from

Safeway’s former Florida division.

During 2002, the accrual was

reduced by $12.0 million as cash

was paid out. In addition, Furr’s

began the liquidation process and

Homeland emerged from bank-

ruptcy in 2002 and, based on the

resolution of various leases,

Safeway reversed $12.1 million of

the accrual, leaving a balance of

$18.6 million at year-end 2002.

Safeway is unable to determine

its maximum potential obligation

with respect to other divested

operations, should there be any

similar defaults, because informa-

tion about the total number of

leases from these divestitures that

are still outstanding is not avail-

able. Based on an internal assess-

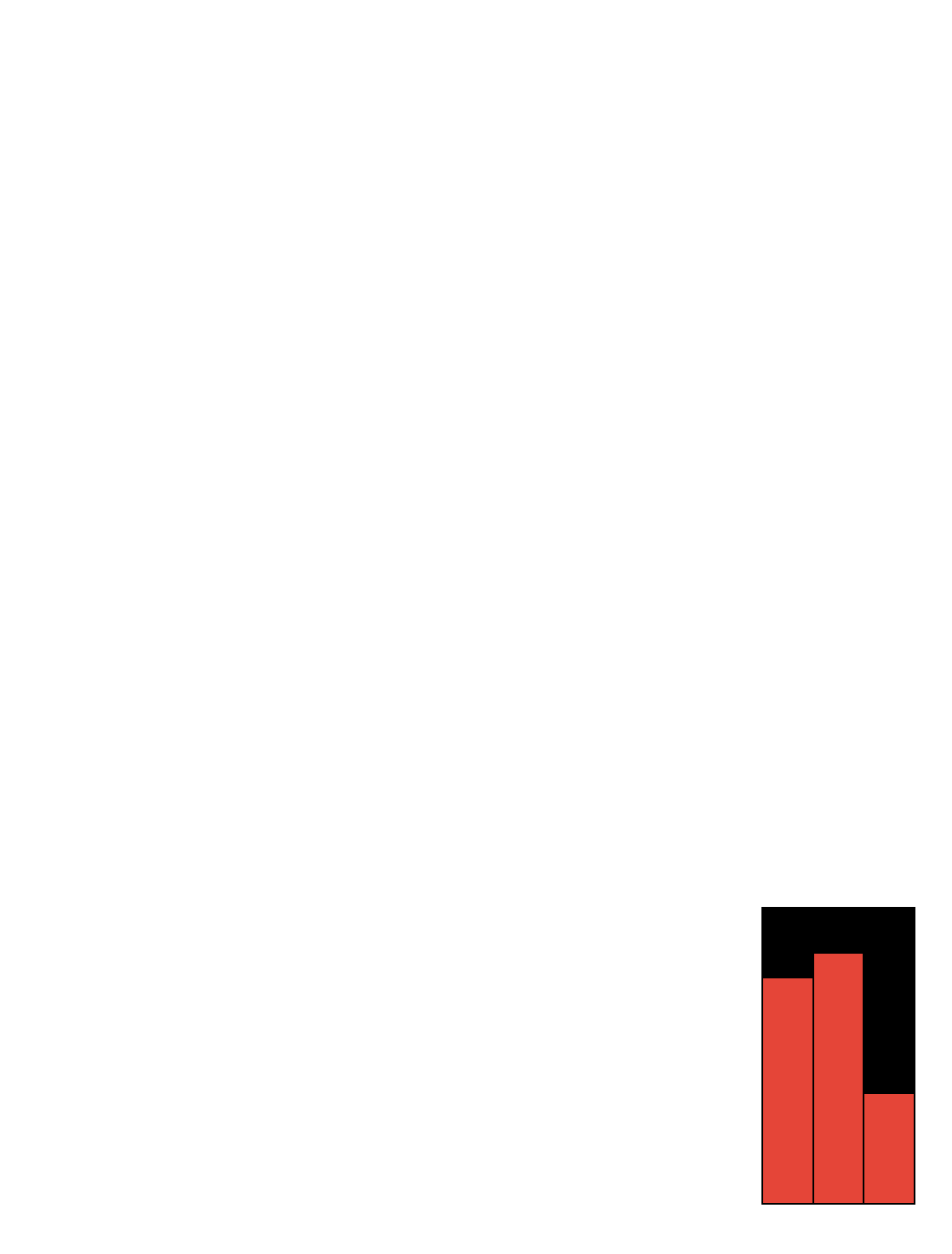

Income From

Continuing Operations

(In Millions)

00

$1,154.2

01

$1,286.7

02

$568.5