Safeway 2002 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

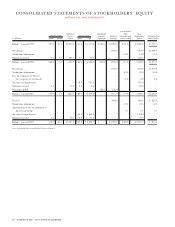

24 SAFEWAY INC. 2002 ANNUAL REPORT

In January 2003, FIN No. 46, “Consolidation of Variable

Interest Entities,” was issued. This interpretation requires a

company to consolidate variable interest entities (“VIE”) if

the enterprise is a primary beneficiary (holds a majority of

the variable interest) of the VIE and the VIE possess specif-

ic characteristics. It also requires additional disclosure for

parties involved with VIEs. The provisions of this interpre-

tation are effective in 2003. Adoption of this interpretation

will not have a material effect on the Company’s financial

statements.

FORWARD-LOOKING STATEMENTS

This Annual Report contains certain forward-looking state-

ments within the meaning of Section 27A of the Securities Act

of 1933 and Section 21E of the Securities Exchange Act of

1934. Such statements relate to, among other things, capital

expenditures, acquisitions, the valuation of Safeway’s invest-

ments, operating improvements and costs, tax rate and gross

profit improvement, and are indicated by words or phrases such

as “continuing,” “ongoing,” “expects,” and similar words or

phrases. The following are among the principal factors that

could cause actual results to differ materially from the forward-

looking statements: general business and economic conditions

in our operating regions, including the rate of inflation, con-

sumer spending levels, population, employment and job growth

in our markets; pricing pressures and competitive factors, which

could include pricing strategies, store openings and remodels by

our competitors; results of our programs to control or reduce

costs, improve buying practices and control shrink; results of

our programs to increase sales, including private-label sales, and

our promotional programs; results of our programs to improve

capital management; the ability to integrate any companies we

acquire and achieve operating improvements at those compa-

nies; changes in financial performance of or our equity invest-

ments; increases in labor costs and relations with union

bargaining units representing our employees or employees of

third-party operators of our distribution centers; changes in

state or federal legislation or regulation; the cost and stability of

power sources; opportunities, acquisitions or dispositions that

we pursue; the rate of return on our pension assets; and the

availability and terms of financing. Consequently, actual events

and results may vary significantly from those included in or con-

templated or implied by such statements. The Company under-

takes no obligation to update forward-looking statements to

reflect developments or information obtained after the date

hereof and disclaims any obligation to do so.

In December 2002, the FASB issued SFAS No. 148,

“Accounting for Stock-Based Compensation – Transition and

Disclosure.” SFAS No. 148 amends SFAS No. 123,

“Accounting for Stock-Based Compensation,” to provide alter-

native methods of transition for a voluntary change to the fair

value based method of accounting for stock-based employee

compensation. In addition, SFAS No. 148 amends the disclo-

sure requirements of SFAS No. 123 to require prominent

disclosures in both annual and interim financial statements

about the method of accounting for stock-based employee

compensation and the effect of the method used on reported

results. The provisions of SFAS No. 148 are effective for

financial statements for fiscal years ending after December 15,

2002. The Company accounts for stock-based employee com-

pensation arrangements in accordance with the provisions of

Accounting Principles Board Opinion No. 25, “Accounting

for Stock Issued to Employees,” and complies with the disclo-

sure provisions of SFAS No. 123 and SFAS No. 148.

EITF Issue No. 02-16, “Accounting by a Reseller for

Cash Consideration Received from a Vendor,” provides that

cash consideration received from a vendor is presumed to be

a reduction of the prices of the vendor’s products or servic-

es and should, therefore, be characterized as a reduction in cost

of sales unless it is a payment for assets or services delivered to

the vendor, in which case the cash consideration should be

characterized as revenue, or it is a reimbursement of costs

incurred to sell the vendor’s products, in which case the cash

consideration should be characterized as a reduction of that

cost. EITF No. 02-16 becomes effective for the Company in the

first quarter of 2003. The Company is currently analyzing the

effect that adoption of EITF No. 02-16 will have on its

financial statements.

In November 2002, FASB Interpretation (“FIN”) No. 45,

“Guarantor’s Accounting and Disclosure Requirements

for Guarantees, Including Indirect Guarantees and

Indebtedness of Others,” was issued. This interpretation

requires the initial measurement and recognition, on a

prospective basis only, to guarantees issued or modified after

December 31, 2002. Additionally, certain disclosure require-

ments are effective for financial statements ending after

December 15, 2002. The Company complies with the dis-

closure provisions of FIN No. 45 and is currently assessing

the impact that adoption of FIN No. 45 will have on the

Company’s financial statements.