Safeway 2002 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

22 SAFEWAY INC. 2002 ANNUAL REPORT

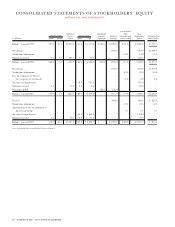

GOODWILL SFAS No. 142 became effective for Safeway in

the first quarter of 2002. Adoption of this standard changed

our method of accounting for goodwill. Goodwill is no

longer amortized and instead is reviewed for impairment on

an annual basis. Safeway recorded a $700 million charge for

the cumulative effect of adoption of SFAS No. 142 in the

first quarter of 2002 and another $1,288 million goodwill

impairment charge after completing its annual impairment

test in the fourth quarter of 2002. See Note C to the con-

solidated financial statements.

Safeway reviewed goodwill for impairment at the operat-

ing division level. All of the Company’s 2002 goodwill

impairment related to Dominick’s, which the Company is

currently planning to sell, and Randall’s, which had a

remaining goodwill balance of $452.6 million at year-end

2002. Fair value was determined by an independent third

party appraiser which primarily used the discounted cash

flow method and the guideline company method.

The annual impairment review required by SFAS No. 142

requires extensive use of accounting judgments and estimates

of future operating results. Changes in estimates or applica-

tion of alternative assumptions and definitions could produce

significantly different results. The factors that most signifi-

cantly affect the fair value calculation are market multiples

and estimates of future cash flows.

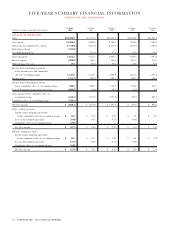

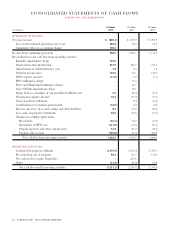

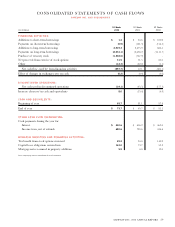

LIQUIDITY AND FINANCIAL RESOURCES

Net cash flow from operating activities was $1,938.1 million

in 2002, $2,150.0 million in 2001 and $1,909.5 million in

2000. Net cash flow from operating activities decreased in

2002 primarily due to changes in working capital. Net cash

flow from operating activities increased in 2001 largely due

to increased net income, partially offset by changes in work-

ing capital.

Cash flow used by investing activities was $1,313.1 million

in 2002, $2,131.6 million in 2001 and $1,337.0 million in

2000. Cash flow used by investing activities decreased in

2002 primarily because of cash used to acquire Genuardi’s in

2001, as well as lower capital expenditures. Cash flow used by

investing activities increased in 2001 over 2000 primarily

because of cash used to acquire Genuardi’s, as well as

increased capital expenditures. Safeway opened 71 new

stores and remodeled 191 stores in 2002. In 2001, Safeway

opened 91 new stores and remodeled 231 stores.

Cash flow used by financing activities was $597.7 mil-

lion in 2002 primarily due to cash flow from operations

being used to pay down debt. Cash flow from financing

activities was $12.1 million in 2001 primarily due to addi-

tional borrowings related to the Genuardi’s Acquisition,

almost entirely offset by cash flow from operations being

used to pay down debt.

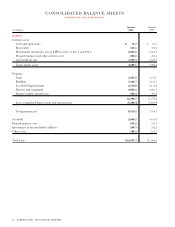

Based upon the current level of operations, Safeway

believes that cash flow from operating activities and other

sources of liquidity, including borrowing under the

Company’s commercial paper program and bank credit

agreement, will be adequate to meet anticipated require-

ments for working capital, capital expenditures, interest pay-

ments and scheduled principal payments for the foreseeable

future. There can be no assurance, however, that Safeway’s

business will continue to generate cash flow at or above cur-

rent levels or that the Company will be able to maintain its

ability to borrow under the commercial paper program and

bank credit agreement.

If the Company’s credit rating were to decline below its

current level of Baa2/BBB, the ability to borrow under the

commercial paper program would be adversely affected.

Safeway’s ability to borrow under the bank credit agreement

is unaffected by Safeway’s credit rating. However, if

Safeway’s 2002 Adjusted EBITDA (as defined in Safeway’s

bank credit agreement) to interest ratio of 7.68 to 1 were to

decline to 2.0 to 1, or if Safeway’s year-end 2002 debt to

Adjusted EBITDA ratio of 2.55 to 1 were to grow to 3.5 to

1, Safeway’s ability to borrow under the bank credit agree-

ment would be impaired.

The table below presents significant contractual obligations of the Company at year-end 2002:

(In millions) 2003 2004 2005 2006 2007 Thereafter Total

Long-term debt $780.3 $699.6 $232.5 $2,479.7 $ 785.0 $2,812.4 $7,789.5

Capital lease obligations(1) 25.2 27.1 28.6 29.3 29.2 398.1 537.5

Operating leases 341.7 332.7 317.1 299.4 279.5 2,542.7 4,113.1

Contracts for purchase of property,

equipment and construction of buildings 129.1 –––––129.1

(1) Minimum lease payments, less amounts representing interest.