Safeway 2002 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

SAFEWAY INC. 2002 ANNUAL REPORT 31

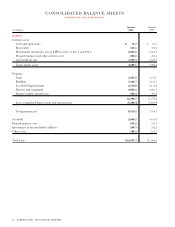

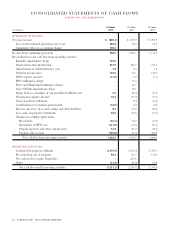

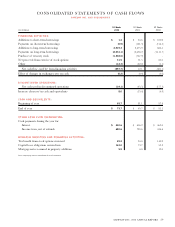

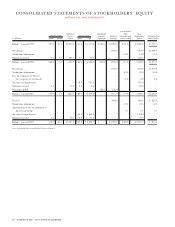

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

SAFEWAY INC. AND SUBSIDIARIES

NOTE A: THE COMPANY AND

SIGNIFICANT ACCOUNTING POLICIES

THE COMPANY Safeway Inc. (“Safeway” or the “Company”)

is one of the largest food and drug retailers in North

America, with 1,695 continuing stores and 113 Dominick’s

stores which are held for sale at year-end 2002. See Note N.

Safeway’s U.S. retail operations are located principally in

California, Oregon, Washington, Alaska, Colorado, Arizona,

Texas and the Mid-Atlantic region. The Company’s

Canadian retail operations are located principally in British

Columbia, Alberta and Manitoba/Saskatchewan. In sup-

port of its retail operations, the Company has an extensive

network of distribution, manufacturing and food process-

ing facilities.

In February 2001, Safeway acquired all of the assets of

Genuardi’s for approximately $530 million in cash (the

“Genuardi’s Acquisition”). The Genuardi’s Acquisition was

accounted for as a purchase and resulted in goodwill of

approximately $521 million. Safeway funded the acquisition

through the issuance of commercial paper and debentures.

Safeway’s 2001 statement of operations includes 47 weeks of

Genuardi’s operating results.

The Company also has a 49% ownership interest in Casa

Ley, S.A. de C.V. (“Casa Ley”), which operates 102 food and

general merchandise stores in western Mexico.

In addition, Safeway has a strategic alliance with and a

52.5% ownership interest in GroceryWorks Holdings, Inc.,

an Internet grocer.

BASIS OF CONSOLIDATION The consolidated financial state-

ments include Safeway Inc., a Delaware corporation, and all

majority-owned subsidiaries. All significant intercompany

transactions and balances have been eliminated in consoli-

dation. The Company’s investment in Casa Ley is reported

using the equity method and is recorded on a one-month

delay basis because financial information for the latest

month is not available from Casa Ley in time to be included

in Safeway’s consolidated earnings until the following

reporting period.

FISCAL YEAR The Company’s fiscal year ends on the

Saturday nearest December 31. The last three fiscal years

consist of the 52-week periods ended December 28, 2002,

December 29, 2001 and December 30, 2000.

REVENUE RECOGNITION Revenue is recognized at the point

of sale for retail sales. Discounts provided to customers in

connection with loyalty cards are accounted for as a reduc-

tion of sales.

COST OF GOODS SOLD Cost of goods sold includes cost of

inventory sold during the period, including purchase and

distribution costs. Advertising and promotional expenses

are also included as a component of cost of goods sold.

Such costs are expensed in the period the advertisement

occurs. Advertising and promotional expenses totaled

$350.4 million in 2002, $384.1 million in 2001 and $377.0

million in 2000.

Vendor allowances that relate to the Company’s buying

and merchandising activities consist primarily of promo-

tional allowances and advertising allowances and, to a less-

er extent, slotting allowances. Promotional and advertising

allowances are recognized as a reduction in cost of goods

sold when the related expense is incurred or the related per-

formance is completed. Safeway recognizes slotting

allowances as a reduction in cost of goods sold when the

product is first stocked, which is generally when all the relat-

ed expenses have been incurred. Lump-sum payments

received for multi-year contracts are amortized over the life

of the contracts. Vendor allowances totaled $2.1 billion in

2002 and 2001 and $1.9 billion in 2000.

USE OF ESTIMATES The preparation of financial state-

ments in conformity with accounting principles generally

accepted in the United States of America requires manage-

ment to make estimates and assumptions that affect the

reported amounts of assets and liabilities and disclosure of

contingent assets and liabilities at the date of the financial

statements, and the reported amounts of revenues and

expenses during the reporting period. Actual results could

differ from those estimates.

TRANSLATION OF FOREIGN CURRENCIES Assets and liabili-

ties of the Company’s Canadian subsidiaries and Casa Ley

are translated into U.S. dollars at year-end rates of exchange,

and income and expenses are translated at average rates dur-

ing the year. Adjustments resulting from translating financial

statements into U.S. dollars are reported, net of applicable

income taxes, as a separate component of comprehensive

income in the consolidated statements of stockholders’ equity.

CASH AND CASH EQUIVALENTS Short-term investments

with original maturities of less than three months are con-

sidered to be cash equivalents.