Safeway 2002 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

32 SAFEWAY INC. 2002 ANNUAL REPORT

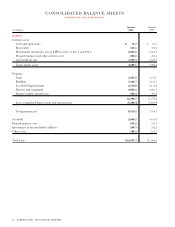

MERCHANDISE INVENTORIES Merchandise inventory of

$1,802.8 million at year-end 2002 and $1,690.4 million at

year-end 2001 is valued at the lower of cost on a last-in, first-

out (“LIFO”) basis or market value. Such LIFO inventory

had a replacement or current cost of $1,867.9 million at

year-end 2002 and $1,773.0 million at year-end 2001.

Liquidations of LIFO layers resulted in income of $5.3 mil-

lion in 2002, $1.8 million in 2001 and $2.2 million in 2000.

All remaining inventory is valued at the lower of cost on a

first-in, first-out (“FIFO”) basis or market value. The FIFO

cost of inventory approximates replacement or current cost.

PROPERTY AND DEPRECIATION Property is stated at cost.

Depreciation expense on buildings and equipment is com-

puted on the straight-line method using the following lives:

Stores and other buildings 7 to 40 years

Fixtures and equipment 3 to 15 years

Property under capital leases and leasehold improve-

ments are amortized on a straight-line basis over the shorter

of the remaining terms of the lease or the estimated useful

lives of the assets.

SELF-INSURANCE The Company is primarily self-insured

for workers’ compensation, automobile and general liability

costs. The self-insurance liability is determined actuarially,

based on claims filed and an estimate of claims incurred but

not yet reported, and is discounted using a risk-free rate of

interest. The present value of such claims was calculated

using a discount rate of 4.0% in 2002 and 5.0% in 2001.

The current portion of the self-insurance liability of $105.3

million at year-end 2002 and $85.6 million at year-end 2001

is included in other accrued liabilities in the consolidated

balance sheets. The long-term portion of $194.6 million at

year-end 2002 and $181.2 million at year-end 2001 is

included in accrued claims and other liabilities. The

Company recorded expense of $165.2 million in 2002,

$121.5 million in 2001 and $55.0 million in 2000. Claims

payments were $132.1 million in 2002, $120.1 million in

2001 and $108.2 million in 2000. The self-insurance liabili-

ty increased by $12.0 million in 2001 because of the

Genuardi’s Acquisition. The total undiscounted liability was

$341.5 million at year-end 2002 and $307.7 million at year-

end 2001.

INCOME TAXES The Company provides a deferred tax

expense or benefit equal to the change in the deferred tax

liability during the year in accordance with Statement of

Financial Accounting Standards (“SFAS”) No. 109,

“Accounting for Income Taxes.” Deferred income taxes rep-

resent tax credit carryforwards and future net tax effects

resulting from temporary differences between the financial

statement and tax basis of assets and liabilities using enact-

ed tax rates in effect for the year in which the differences are

expected to reverse.

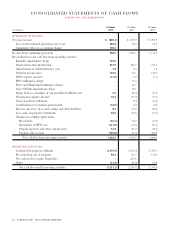

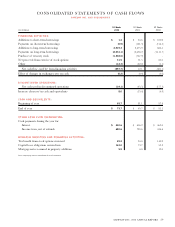

OFF-BALANCE SHEET FINANCIAL INSTRUMENTS As dis-

cussed in Note G, the Company has, from time to time,

entered into interest rate swap agreements to limit the expo-

sure of certain of its floating-rate debt to changes in market

interest rates. Interest rate swap agreements involve the

exchange with a counterparty of fixed and floating-rate

interest payments periodically over the life of the agree-

ments without exchange of the underlying notional princi-

pal amounts. The differential to be paid or received is

recognized over the life of the agreements as an adjustment

to interest expense. The Company’s counterparties have

been major financial institutions.

FAIR VALUE OF FINANCIAL INSTRUMENTS Generally

accepted accounting principles require the disclosure of the

fair value of certain financial instruments, whether or not

recognized in the balance sheet, for which it is practicable to

estimate fair value. Safeway estimated the fair values pre-

sented below using appropriate valuation methodologies and

market information available as of year-end. Considerable

judgment is required to develop estimates of fair value, and

the estimates presented are not necessarily indicative of the

amounts that the Company could realize in a current market

exchange. The use of different market assumptions or esti-

mation methodologies could have a material effect on the

estimated fair values. Additionally, these fair values were esti-

mated at year-end, and current estimates of fair value may

differ significantly from the amounts presented.

The following methods and assumptions were used to

estimate the fair value of each class of financial instruments:

Cash and Equivalents, Accounts Receivable, Accounts Payable

and Short-Term Debt. The carrying amount of these items

approximates fair value.

Long-Term Debt. Market values quoted on the New York

Stock Exchange are used to estimate the fair value of

publicly traded debt. To estimate the fair value of debt issues

that are not quoted on an exchange, the Company uses

those interest rates that are currently available to it for