Safeway 2002 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2002 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

|

|

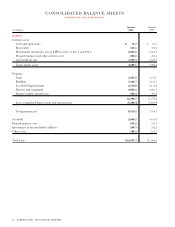

SAFEWAY INC. 2002 ANNUAL REPORT 33

issuance of debt with similar terms and remaining maturi-

ties. At year-end 2002, the estimated fair value of debt was

$8.3 billion compared to a carrying value of $7.8 billion. At

year-end 2001, the estimated fair value of debt was $7.1 bil-

lion compared to carrying value of $6.9 billion.

Off-Balance Sheet Instruments. The fair value of interest rate

swap agreements are the amounts at which they could be

settled based on estimates obtained from dealers. At year-

end 2002 and 2001, no such agreements were outstanding.

STORE CLOSING AND IMPAIRMENT CHARGES Safeway con-

tinually reviews its stores’ operating performance and assess-

es its plans for certain store and plant closures. In

accordance with SFAS No. 144, “Accounting for the

Impairment or Disposal of Long-Lived Assets,” losses relat-

ed to the impairment of long-lived assets are recognized

when expected future cash flows are less than the asset’s car-

rying value. At the time a store is closed or because of

changes in circumstances that indicate the carrying value of

an asset may not be recoverable, the Company evaluates the

carrying value of the asset in relation to its expected future

cash flows. If the carrying value is greater than the future

cash flows, a provision is made for the impairment of the

assets to write the assets down to estimated fair value. Fair

value is determined by estimating net future cash flows, dis-

counted using a risk-adjusted rate of return. The Company

calculates its liability for impairment on a store-by-store

basis. These provisions are recorded as a component of

operating and administrative expense and are disclosed in

Note D.

For stores to be closed that are under long-term leases, the

Company records a liability for the future minimum lease

payments and related ancillary costs, from the date of closure

to the end of the remaining lease term, net of estimated cost

recoveries that may be achieved through subletting properties

or through favorable lease terminations, discounted using a

risk-adjusted rate of interest. This liability is recorded at the

time the store is closed. Activity included in the reserve for

store lease exit costs is disclosed in Note D.

STOCK-BASED COMPENSATION Safeway accounts for stock-

based awards to employees using the intrinsic value method

in accordance with Accounting Principles Board Opinion

No. 25, “Accounting for Stock Issued to Employees.” The

following table illustrates the effect on net (loss) income and

(loss) earnings per share as if the Company had applied the

fair value recognition provisions of SFAS No. 123:

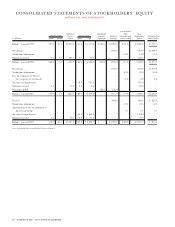

(in millions, except per-share amounts) 2002 2001 2000

Net (loss) income – as reported $(828.1) $1,253.9 $1,091.9

Less:

Total stock-based employee

compensation expense

determined under fair value-

based method for all awards,

net of related tax effects (49.6) (45.0) (30.4)

Net (loss) income – pro forma $(877.7) $1,208.9 $1,061.5

Basic (loss) earnings per share:

As reported $ (1.77) $ 2.49 $ 2.19

Pro forma $ (1.88) $ 2.40 $ 2.13

Diluted (loss) earnings per share:

As reported $ (1.75) $ 2.44 $ 2.13

Pro forma $ (1.85) $ 2.36 $ 2.07

NEW ACCOUNTING STANDARDS SFAS No. 142, “Goodwill

and Other Intangible Assets,” addresses the initial recogni-

tion and measurement of intangible assets acquired outside

of a business combination and the accounting for goodwill

and other intangible assets subsequent to their acquisition.

SFAS No. 142 provides that intangible assets with finite use-

ful lives be amortized and that goodwill and intangible

assets with indefinite lives not be amortized, but be tested at

least annually for impairment. Under the provisions of

SFAS No. 142, any impairment loss identified upon adop-

tion of this standard is recognized as a cumulative effect of

a change in accounting principle. Any impairment loss

incurred subsequent to initial adoption of SFAS No. 142 is

recorded as a charge to current period earnings.

The Company adopted SFAS No. 142 on December 30,

2001. Under the transitional provisions of SFAS No. 142,

the Company’s goodwill was tested for impairment as of

December 30, 2001. Each of the Company’s reporting

units was tested for impairment by comparing the fair value

of each reporting unit with its carrying value. Fair value

was determined based on a valuation study performed by

an independent third party appraiser which primarily con-

sidered the discounted cash flow, guideline company and

similar transaction methods. As a result of the Company’s

impairment test, the Company recorded an impairment loss

at Dominick’s of $589 million and Randall’s of $111 million

to reduce the carrying value of goodwill to its implied fair

value. Impairment in both cases was due to a combination of

factors including acquisition price, post-acquisition capital

expenditures and operating performance. In accordance

with SFAS No. 142, the impairment charge was reflected as