Safeway 2004 Annual Report Download - page 27

Download and view the complete annual report

Please find page 27 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

SAFEWAY INC. 2004 ANNUAL REPORT 25

SAFEWAY INC. AND SUBSIDIARIES

the date of closure to the end of the remaining lease term,

net of estimated cost recoveries. In both cases, fair value is

determined by estimating net future cash flows and

discounting them using a risk-adjusted rate of interest.

The Company estimates future cash flows based on its

experience and knowledge of the market in which the

closed store is located and, when necessary, uses real

estate brokers. However, these estimates project future

cash flow several years into the future and are affected by

variable factors such as inflation, real estate markets and

economic conditions.

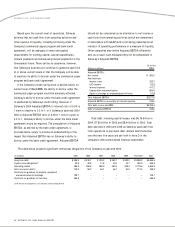

EMPLOYEE BENEFIT PLANS The determination of

Safeway’s obligation and expense for pension and other post-

retirement benefits is dependent, in part, on the Company’s

selection of certain assumptions used by its actuaries in

calculating these amounts. These assumptions are disclosed

in Note I to the consolidated financial statements and

include, among other things, the discount rate, the expected

long-term rate of return on plan assets and the rates of

compensation and health care costs. In accordance with

generally accepted accounting principles, actual results that

differ from the Company’s assumptions are accumulated and

amortized over future periods and, therefore, affect its

recognized expense and recorded obligation in such future

periods. While Safeway believes its assumptions are

appropriate, significant differences in Safeway’s actual

experience or significant changes in the Company’s

assumptions may materially affect Safeway’s pension and

other post-retirement obligations and its future expense.

When not considering other changes in assumptions or

actual return on plan assets, a 100-basis-point reduction in

the year-end 2004 discount rate alone would negatively

impact 2005 U.S. pension expense by approximately $28

million, and a 50-basis-point reduction in expected return on

plan assets alone would negatively impact 2005 U.S.

pension expense by approximately $8 million.

Not considering any changes in assumptions, a $100

million reduction in plan assets in 2004 would impact 2005

U.S. pension expense by approximately $18 million. The fair

value of plan assets can vary significantly from year to year.

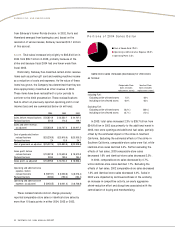

GOODWILL Safeway accounts for goodwill in accordance

with SFAS No. 142, “Goodwill and Other Intangible Assets.”

As required by SFAS No. 142, Safeway tests for goodwill

annually using a two-step approach with extensive use of

accounting judgments and estimates of future operating

results. Changes in estimates or application of alternative

assumptions and definitions could produce significantly

different results. The factors that most significantly affect

the fair value calculation are market multiples and

estimates of future cash flows. Fair value is determined

by an independent third-party appraiser who primarily

used the discounted cash flow method and the guideline

company method.

Liquidity and Financial Resources

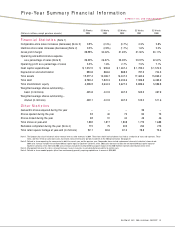

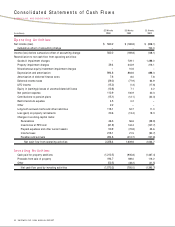

Net cash flow from operating activities was $2,226.4 million

in 2004, $1,609.6 million in 2003, and $2,034.7 million in

2002. Net cash flow from operating activities increased in

2004 largely due to increased net income and changes in

working capital. Net cash flow from operating activities

decreased in 2003 and 2002 primarily due to lower operating

results and changes in working capital.

Cash flow used by investing activities was $1,070.3

million in 2004, $795.0 million in 2003 and $1,395.7 million

in 2002. Cash flow used by investing activities increased

in 2004 compared to 2003 because of higher capital

expenditures. Cash flow used by investing activities

decreased in 2003 compared to 2002 because of reduced

capital expenditures in 2003. Cash flow used by investing

activities declined in 2002 compared to 2001 primarily

because of cash used to acquire Genuardi’s in 2001, as well

as reduced capital expenditures.

Capital expenditures were gradually scaled back in 2003

and 2002 as the economy softened. Capital expenditures

increased in 2004 as the Company focused on remodeling

its existing stores under its new “Lifestyle Store” prototype.

In 2004, Safeway opened 33 new stores and completed 115

remodels. In 2003, Safeway opened 40 new stores and

remodeled 75 stores. In 2005, Safeway expects to spend

approximately $1.4 billion in cash capital expenditures,

open approximately 30 to 35 new stores and complete

approximately 275 to 285 remodels.