Safeway 2004 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

40 SAFEWAY INC. 2004 ANNUAL REPORT

SAFEWAY INC. AND SUBSIDIARIES

The Company adopted SFAS No. 142, “Goodwill and

Other Intangible Assets,” on December 30, 2001. Under the

transitional provisions of SFAS No. 142, the Company’s

goodwill was tested for impairment as of December 30,

2001. Each of the Company’s reporting units were tested for

impairment by comparing the fair value of each reporting

unit with its carrying value. Fair value was determined

based on a valuation study performed by an independent

third party who primarily considered the discounted cash

flow, guideline company and similar transaction methods.

As a result of the Company’s impairment test, the Company

recorded an impairment loss to reduce the carrying value of

goodwill at Dominick’s by $589.0 million and Randall’s by

$111.0 million to its implied fair value. Impairment in both

cases was due to a combination of factors including

acquisition price, post-acquisition capital expenditures and

operating performance. In accordance with SFAS No. 142,

the impairment charge was reflected as a cumulative effect

of accounting change in the Company’s statement of

operations.

As required by SFAS No. 142, Safeway tested goodwill

for impairment again in the fourth quarter of 2002, which

represents the annual impairment testing date selected by

Safeway. Fair value was determined based on a valuation

study performed by an independent third party which

primarily considered the discounted cash flow and guideline

company method. As a result of this annual review, Safeway

recorded an impairment charge for Dominick’s goodwill of

$583.8 million and for Randall’s goodwill of $704.2 million.

These additional charges reflect declining multiples in the

retail grocery industry and operating performance.

Also in the fourth quarter of 2003, Safeway performed

its annual review of goodwill. Fair value was determined

based on a valuation study performed by an independent

third party which primarily considered the discounted cash

flow and guideline company method. As a result of this

annual review, Safeway recorded an impairment charge for

Randall’s goodwill of $447.7 million. The additional charges

reflect declining multiples in the retail grocery industry and

operating performance. There was no remaining goodwill

for Dominick’s or Randall’s on Safeway’s consolidated

balance sheet at year-end 2003.

Safeway completed its annual impairment test in the

fourth quarter of 2004. Fair value was determined based on

a valuation study performed by an independent third party

which primarily considered the discounted cash flow and

guideline company method. As a result of this annual review,

Safeway concluded that no impairment charge was required.

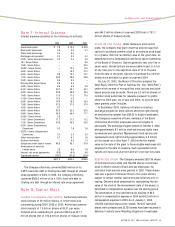

Note C: Store Closing and

Impairment Charges

IMPAIRMENT WRITE-DOWNS Safeway recognized

impairment charges on the write-down of long-lived assets

of $39.4 million in 2004, $344.9 million in 2003 and $213.1

million in 2002. This includes Dominick’s impairment

charges of $311.4 million in 2003 and $201.3 million in

2002. These charges are included as a component of

operating and administrative expense.

In November 2002, Safeway announced the decision to

sell Dominick’s and exit the Chicago market due to labor

issues. In accordance with SFAS No. 144, Safeway recorded

a pre-tax charge for the impairment of long-lived assets of

$201.3 million in the fourth quarter of 2002 to adjust

Dominick’s to its estimated fair market value less cost to sell.

In the first 36 weeks of 2003, Safeway reduced the

carrying value of Dominick’s in part by writing down an

additional $120.7 million of long-lived assets, based on

indications of value received during the sale process. In

November 2003, Safeway announced that it was taking

Dominick’s off the market. Safeway reclassified Dominick’s

from an “asset held for sale” to “asset held and used” and

adjusted Dominick’s individual long-lived assets to the

lower of cost or fair value. As a result, in the fourth quarter

of 2003, Safeway incurred a pre-tax, long-lived asset

impairment charge of $190.7 million.

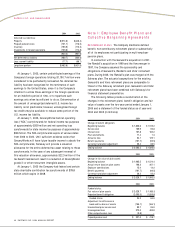

STORE LEASE EXIT COSTS The reserve for store lease

exit costs includes the following activity for 2004, 2003 and

2002 (in millions):

2004 2003 2002

Beginning balance $129.1 $132.1 $132.4

Provision for estimated

net future cash flows of

additional closed stores(1) 55.1 3.7 30.6

Net cash flows, interest accretion,

changes in estimates of net

future cash flows (17.1) (6.7) (30.9)

Ending balance $167.1 $129.1 $132.1

(1) Estimated net future cash flows represents future minimum lease payments and

related ancillary costs from the date of closure to the end of the remaining lease

term, net of estimated cost recoveries that may be achieved through subletting

properties or through favorable lease terminations.