Safeway 2004 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

SAFEWAY INC. AND SUBSIDIARIES

Fair value is determined by estimating net future cash flows,

discounted using a risk-adjusted rate of return. The Company

calculates impairment on a store-by-store basis. These

provisions are recorded as a component of operating and

administrative expense and are disclosed in Note C.

For stores to be closed that are under long-term leases,

the Company records a liability for the future minimum lease

payments and related ancillary costs, from the date of closure

to the end of the remaining lease term, net of estimated

cost recoveries that may be achieved through subletting

properties or through favorable lease terminations, discounted

using a risk-adjusted rate of interest. This liability is

recorded at the time the store is closed. Activity included in

the reserve for store lease exit costs is disclosed in Note C.

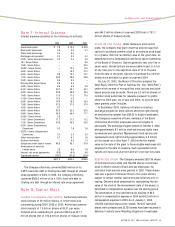

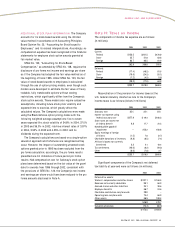

STOCK-BASED COMPENSATION Safeway accounts for

stock-based awards to employees using the intrinsic value

method in accordance with Accounting Principles Board

Opinion (“APB”) No. 25, “Accounting for Stock Issued to

Employees.” The following table illustrates the effect on net

income (loss) and earnings (loss) per share if the Company

had applied the fair value recognition provisions of SFAS

No. 123, as amended by SFAS No. 148:

(In millions, except per-share amounts) 2004 2003 2002

Net income (loss) – as reported $560.2 $(169.8) $(828.1)

Add:

Stock-based employee

compensation expense included

in reported net income, net of

related tax effects 2.8 0.1 –

Less:

Total stock-based employee

compensation expense

determined under fair value

based method for all awards,

net of related tax effects (47.6) (51.2) (49.6)

Net income (loss) – pro forma $515.4 $(220.9) $(877.7)

Basic earnings (loss) per share:

As reported $1.26 $(0.38) $(1.77)

Pro forma 1.16 (0.50) (1.88)

Diluted earnings (loss) per share:

As reported $1.25 $(0.38) $(1.77)

Pro forma 1.15 (0.50) (1.88)

NEW ACCOUNTING STANDARDS In December 2003, the

FASB revised SFAS No. 132, “Employer’s Disclosures about

Pensions and Other Postretirement Benefits.” This revised

statement requires new annual disclosures about the types

of plan assets, investment strategy, measurement date, plan

obligations and cash flows as well as components of the

net periodic benefit cost recognized in interim periods. The

new annual disclosure requirements apply to fiscal years

ending after December 15, 2003, except for the disclosure

of expected future benefit payment, which must be

disclosed for fiscal years ending after June 15, 2004.

Interim period disclosures are generally effective for interim

periods beginning after December 15, 2003. The Company

has included the disclosures required by SFAS No. 132 in its

financial statements for the year ended January 1, 2005.

In January 2004, the FASB issued SFAS No. 106-1,

“Accounting and Disclosure Requirements Related to the

Medicare Prescription Drug, Improvement and Modernization

Act of 2003.” This statement permits a sponsor to make a

one-time election to defer accounting for the effects of the

Medicare Prescription Drug, Improvement and Modernization

Act of 2003, or the Prescription Drug Act. The Prescription

Drug Act, signed into law in December 2003, establishes a

prescription drug benefit under Medicare (Medicare Part D)

and a federal subsidy to sponsors of retiree health care

benefit plans that provide a benefit that is at least actuarially

equivalent to Medicare Part D. SFAS No. 106-1 does not

provide specific guidance as to whether a sponsor should

recognize the effects of the Prescription Drug Act in its

financial statements. The Prescription Drug Act introduces

two new features to Medicare that must be considered when

measuring accumulated postretirement benefit costs. The

new features include a subsidy to the plan sponsors that is

based on 28% of an individual beneficiary’s annual

prescription drug costs between $250 and $5,000 and an

opportunity for a retiree to obtain a prescription drug benefit

under Medicare. The Prescription Drug Act is not expected to

reduce Safeway’s net postretirement benefit costs.

Safeway has elected to defer adoption of SFAS No. 106-1

due to the lack of specific guidance. Therefore, the net

postretirement benefit costs disclosed in the Company’s

financial statements do not reflect the impacts of the

Prescription Drug Act on the plans. The deferral will continue

to apply until specific authoritative accounting guidance for

the federal subsidy is issued. Authoritative guidance on the

accounting for the federal subsidy is pending and, when

issued, could require information previously reported in the

Company’s financial statements to change. Safeway is

currently investigating the impacts of SFAS No. 106-1’s

initial recognition, measurement and disclosure provisions

on its financial statements.

38 SAFEWAY INC. 2004 ANNUAL REPORT