Safeway 2004 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

In December 2004, the FASB issued FASB Staff Position

SFAS No. 109-2, “Accounting Disclosure Guidance for the

Foreign Earnings Repatriation Provision within the American

Jobs Creation Act of 2004,” which provides accounting and

disclosure guidance for the repatriation provisions of the

American Jobs Creation Act of 2004 (the “Act”). The Act

provides for a special one-time tax deduction of certain

earnings repatriated in 2005. The Company is evaluating

whether to take advantage of this provision with respect to

its Canadian subsidiary, and expects to complete the

evaluation by the fourth quarter of 2005. The Company

anticipates that it could repatriate between zero and $734

million, and that the tax cost of the repatriation would be

between zero and $75 million.

In December 2004, the FASB issued FASB Staff Position

SFAS No. 109-1, “Application of FASB Statement No. 109,

Accounting for Income Taxes, to the Tax Deduction on

Qualified Production Activities Provided by the American

Jobs Creation Act of 2004,” which provides accounting and

disclosure guidance on the Act’s qualified production

activities deduction. The Company is currently evaluating

the impact of this guidance on its effective tax rate for 2005

and subsequent periods.

In December 2004, the FASB issued SFAS No. 123

(Revised 2004), “Share-Based Payment” (“SFAS No. 123R”),

which replaces SFAS No. 123, supersedes APB 25 and

related interpretations and amends SFAS No. 95,

“Statement of Cash Flows.” The provisions of SFAS No. 123R

are similar to those of SFAS No. 123; however, SFAS No.

123R requires all share-based payments to employees,

including grants of employee stock options, to be recognized

in the financial statements as compensation cost based on

their fair value on the date of grant. Fair value of share-

based awards will be determined using option-pricing

SAFEWAY INC. 2004 ANNUAL REPORT 39

SAFEWAY INC. AND SUBSIDIARIES

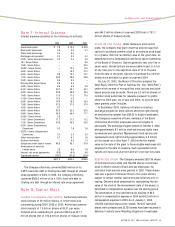

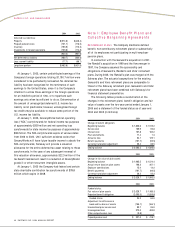

Note B: Goodwill

A summary of changes in Safeway’s goodwill during 2004 and 2003 by geographic area is as follows:

(In millions) 2004 2003

U.S. Canada Total U.S. Canada Total

Balance – beginning of the year $2,328.3 $76.6 $2,404.9 $3,062.9 $62.8 $3,125.7

Impairment charges –––(729.1) –(729.1)

Other adjustments (2.7)(1) 4.4(2) 1.7 (5.5)(1) 13.8(2) 8.3

Balance – end of year $2,325.6 $81.0 $2,406.6 $2,328.3 $76.6 $2,404.9

(1) Primarily represents revised estimate of pre-acquisition tax accrual.

(2) Represents foreign currency translation adjustments in Canada.

models (e.g. Black-Scholes or binomial models) and

assumptions that appropriately reflect the specific circum-

stances of the awards. Compensation cost will be

recognized over the vesting period based on the fair value

of awards that actually vest.

The Company will be required to choose between the

modified-prospective and modified-retrospective transition

alternatives in adopting SFAS No. 123R. Under the modified-

prospective-transition method, compensation cost will be

recognized in financial statements issued subsequent to the

date of adoption for all shared-based payments granted,

modified or settled after the date of adoption, as well as for

any unvested awards that were granted prior to the date of

adoption. Under the modified-retrospective-transition method,

prior period financial statements will also be restated by

recognizing compensation cost as previously reported in the pro

forma disclosures under SFAS No. 123. The restatement

provisions can be applied to either a) all periods presented or b)

to the beginning of the fiscal year in which SFAS No. 123R is

adopted. As the Company previously adopted only the pro

forma disclosure provisions of SFAS No. 123, Safeway will

recognize compensation cost relating to the unvested portion of

awards granted prior to the date of adoption using the same

estimate of the grant-date fair value and the same attribution

method used to determine the pro forma disclosures under

SFAS No. 123.

SFAS No. 123R is effective at the beginning of the first

interim or annual period beginning after June 15, 2005, and

early adoption is encouraged. Safeway has elected to early

adopt this pronouncement beginning in the first quarter of

2005. The Company is in the process of evaluating the use

of certain option-pricing models as well as the assumptions

to be used in such models. When that evaluation is complete,

Safeway will select a transition method.