Safeway 2004 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

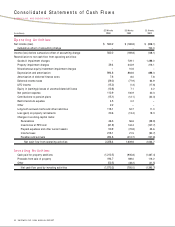

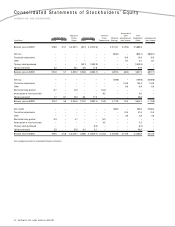

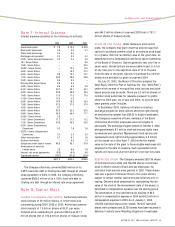

SAFEWAY INC. 2004 ANNUAL REPORT 41

SAFEWAY INC. AND SUBSIDIARIES

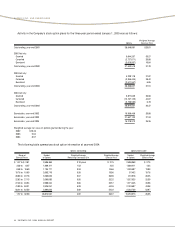

Store lease exit costs are included as a component of

operating and administrative expense and the liability is

included in accrued claims and other liabilities.

Store lease exit costs related to the Furr’s and Homeland

bankruptcies are not included above but are discussed in

Note L.

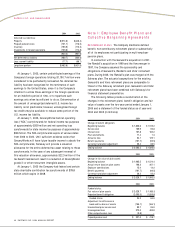

Note D: Financing

Notes and debentures were composed of the following at

year-end (in millions):

2004 2003

Commercial paper $ 105.0 $1,210.6

Bank credit agreement, unsecured ––

Other bank borrowings, unsecured 18.2 8.0

Mortgage notes payable, secured 26.1 33.7

9.30% Senior Secured Debentures due 2007 24.3 24.3

6.85% Senior Notes due 2004, unsecured –200.0

7.25% Senior Notes due 2004, unsecured –400.0

2.50% Senior Notes due 2005, unsecured 200.0 200.0

Floating Rate Senior Notes due 2005, unsecured 150.0 150.0

3.80% Senior Notes due 2005, unsecured 225.0 225.0

6.15% Senior Notes due 2006, unsecured 700.0 700.0

4.80% Senior Notes due 2007, unsecured 480.0 480.0

7.00% Senior Notes due 2007, unsecured 250.0 250.0

4.125% Senior Notes due 2008, unsecured 300.0 300.0

6.50% Senior Notes due 2008, unsecured 250.0 250.0

7.50% Senior Notes due 2009, unsecured 500.0 500.0

4.95% Senior Notes due 2010, unsecured 500.0 –

6.50% Senior Notes due 2011, unsecured 500.0 500.0

5.80% Senior Notes due 2012, unsecured 800.0 800.0

5.625% Senior Notes due 2014, unsecured 250.0 –

7.45% Senior Debentures due 2027, unsecured 150.0 150.0

7.25% Senior Debentures due 2031, unsecured 600.0 600.0

9.65% Senior Subordinated Debentures

due 2004, unsecured –81.2

9.875% Senior Subordinated Debentures

due 2007, unsecured 24.2 24.2

Other notes payable, unsecured 13.8 16.5

6,066.6 7,103.5

Less current maturities (596.9) (699.5)

Long-term portion $5,469.7 $6,404.0

COMMERCIAL PAPER The amount of commercial paper

borrowings is limited to the unused borrowing capacity under

the bank credit agreement. Commercial paper is classified as

long-term because the Company intends to and has the ability

to refinance these borrowings on a long-term basis through

either continued commercial paper borrowings or utilization of the

bank credit agreement, which matures in 2006. The weighted

average interest rate on commercial paper borrowings was

1.22% during 2004 and 2.28% at year-end 2004.

BANK CREDIT AGREEMENT Safeway’s total borrowing

capacity under the bank credit agreement is $2.4 billion. Of

the $2.4 billion credit line, $1.25 billion matures in 2006 and

has a one-year extension option requiring lender consent.

Another $1.15 billion is renewable annually through 2006

and can be extended by the Company for an additional year

through a term-loan conversion feature or through a one-year

extension option requiring lender consent. The restrictive

covenants of the bank credit agreement limit Safeway with

respect to, among other things, creating liens upon its assets

and disposing of material amounts of assets other than in

the ordinary course of business. Safeway is also required to

maintain a minimum Adjusted EBITDA to interest expense

ratio of 2.0 to 1 and not exceed a total debt to Adjusted

EBITDA ratio of 4.0 to 1. As part of the second amendment

to the bank credit agreement dated May 20, 2004, the Debt

to Adjusted EBITDA ratio was temporarily increased to 4.0

to 1 from 3.5 to 1 for a period of one year. At year-end

2004, the Company had total unused borrowing capacity

under the bank credit agreement of $2.25 billion.

U.S. borrowings under the bank credit agreement carry

interest at one of the following rates selected by the Company:

(i) the prime rate; (ii) a rate based on rates at which Eurodollar

deposits are offered to first-class banks by the lenders in the

bank credit agreement plus a pricing margin based on the

Company’s debt rating or interest coverage ratio (the “Pricing

Margin”); or (iii) rates quoted at the discretion of the lenders.

Canadian borrowings denominated in U.S. dollars carry

interest at one of the following rates selected by the

Company: (a) the Canadian base rate or (b) the Canadian

Eurodollar rate plus the Pricing Margin. Canadian borrowings

denominated in Canadian dollars carry interest at one of the

following rates selected by the Company: (i) the Canadian

prime rate or (ii) the rate for Canadian bankers acceptances

plus the Pricing Margin.

During 2004, the Company had no outstanding borrowing

under its bank revolving credit agreement. During the year,

the Company paid facility fees ranging from 0.08% to 0.145%

on the total amount of the credit facility.

OTHER BANK BORROWINGS Other bank borrowings at

year-end 2004 have remaining terms ranging from two days

to two years and a weighted average interest rate of 4.0%.