Safeway 2004 Annual Report Download - page 28

Download and view the complete annual report

Please find page 28 of the 2004 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

|

|

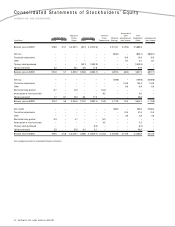

SAFEWAY INC. AND SUBSIDIARIES

should not be considered as an alternative to net income or

cash flows from operating activities (which are determined

in accordance with GAAP) and is not being presented as an

indicator of operating performance or a measure of liquidity.

Other companies may define Adjusted EBITDA differently

and, as a result, such measures may not be comparable to

Safeway’s Adjusted EBITDA.

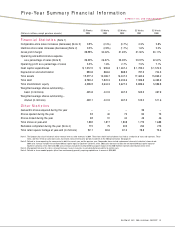

52 weeks

(Dollars in millions) 2004

Adjusted EBITDA:

Net income $ 560.2

Add (subtract):

Income taxes 233.7

LIFO income (15.2)

Interest expense 411.2

Depreciation and amortization 894.6

Equity in earnings of unconsolidated affiliates (12.6)

Total Adjusted EBITDA $2,071.9

Adjusted EBITDA as a multiple of interest expense 5.04x

Total debt at year-end 2004 $6,763.4

Debt to Adjusted EBITDA 3.26x

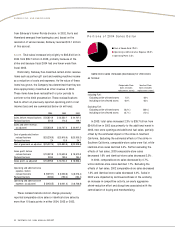

Total debt, including capital leases, was $6.76 billion in

2004, $7.82 billion in 2003 and $8.44 billion in 2002. Total

debt declined in 2004 and 2003 as Safeway used cash flow

from operations to pay down debt. Annual debt maturities

over the next five years are set forth in Note D of the

Company’s 2004 consolidated financial statements.

Based upon the current level of operations, Safeway

believes that net cash flow from operating activities and

other sources of liquidity, including borrowing under the

Company’s commercial paper program and bank credit

agreement, will be adequate to meet anticipated

requirements for working capital, capital expenditures,

interest payments and scheduled principal payments for the

foreseeable future. There can be no assurance, however,

that Safeway’s business will continue to generate cash flow

at or above current levels or that the Company will be able

to maintain its ability to borrow under the commercial paper

program and bank credit agreement.

If the Company’s credit rating were to decline below its

current level of Baa2/BBB, the ability to borrow under the

commercial paper program would be adversely affected.

Safeway’s ability to borrow under the bank credit agreement

is unaffected by Safeway’s credit rating. However, if

Safeway’s 2004 Adjusted EBITDA to interest ratio of 5.04 to

1 were to decline to 2.0 to 1, or if Safeway’s year-end 2004

debt to Adjusted EBITDA ratio of 3.26 to 1 were to grow to

4.0 to 1, Safeway’s ability to borrow under the bank credit

agreement would be impaired. The computation of Adjusted

EBITDA, as defined by the bank credit agreement, is

provided below solely to provide an understanding of the

impact that Adjusted EBITDA has on Safeway’s ability to

borrow under the bank credit agreement. Adjusted EBITDA

26 SAFEWAY INC. 2004 ANNUAL REPORT

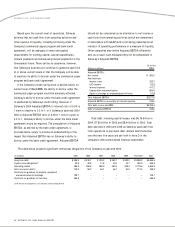

The table below presents significant contractual obligations of the Company at year-end 2004:

(In millions) 2005 2006 2007 2008 2009 Thereafter Total

Long-term debt $ 596.9 $ 818.7 $ 785.2 $ 553.7 $ 502.2 $2,809.9 $6,066.6

Capital lease obligations(1) 42.8 40.8 41.8 42.5 43.7 485.2 696.8

Operating leases 405.9 396.8 380.9 362.5 328.3 2,778.6 4,653.0

Self-insurance liability 142.9 96.2 66.1 46.7 34.5 112.5 498.9

Contracts for purchase of property, equipment

and construction of buildings 139.7 –––––139.7

Contracts for purchase of inventory 486.9 –––––486.9

(1) Minimum lease payments, less amounts representing interest