Safeway 2011 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2011 Safeway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

SAFEWAY INC. AND SUBSIDIARIES

Notes to Consolidated Financial Statements

Store lease exit costs are included as a component of operating and administrative expense, and the liability is included in

accrued claims and other liabilities.

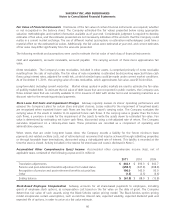

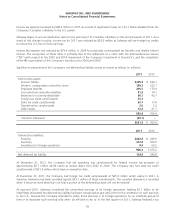

Note D: Financing

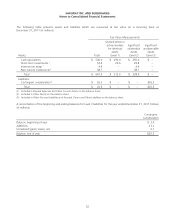

Notes and debentures were composed of the following at year end (in millions):

2011 2010

Commercial paper $–$–

Bank credit agreement, unsecured 39.5 –

Other bank borrowings, unsecured 1.6 2.4

Mortgage notes payable, secured 10.1 11.3

6.50% Senior Notes due 2011, unsecured –500.0

5.80% Senior Notes due 2012, unsecured 800.0 800.0

3.00% Second Series Notes due 2014, unsecured 296.9 –

6.25% Senior Notes due 2014, unsecured 500.0 500.0

5.625% Senior Notes due 2014, unsecured 250.0 250.0

3.40% Senior Notes due 2016, unsecured 400.0 –

6.35% Senior Notes due 2017, unsecured 500.0 500.0

5.00% Senior Notes due 2019, unsecured 500.0 500.0

3.95% Senior Notes due 2020, unsecured 500.0 500.0

4.75% Senior Notes due 2021, unsecured 400.0 –

7.45% Senior Debentures due 2027, unsecured 150.0 150.0

7.25% Senior Debentures due 2031, unsecured 600.0 600.0

Other notes payable, unsecured 23.8 24.1

Interest rate swap fair value adjustment 4.4 11.6

4,976.3 4,349.4

Less current maturities (811.3) (505.6)

Long-term portion $ 4,165.0 $ 3,843.8

Commercial Paper The amount of commercial paper borrowings is limited to the unused borrowing capacity under the

bank credit agreement. Commercial paper is classified as long term because the Company intends to and has the ability

to refinance these borrowings on a long-term basis through either continued commercial paper borrowings or utilization

of the bank credit agreement, which matures in 2015. During 2011, the average commercial paper borrowing was

$395.8 million and had a weighted-average interest rate of 0.39%. During 2010, the average commercial paper

borrowing was $393.5 million which had a weighted-average interest rate of 0.36%.

Bank Credit Agreement The Company has a $1,500.0 million credit agreement with a syndicate of banks which has a

termination date of June 1, 2015 and provides for two additional one-year extensions of the termination date. The credit

agreement provides (i) to Safeway a $1,250.0 million revolving credit facility (the “Domestic Facility”), (ii) to Safeway and

Canada Safeway Limited a Canadian facility of up to $250.0 million for U.S. Dollar and Canadian Dollar advances and

(iii) to Safeway a $400.0 million sub-facility of the Domestic Facility for issuance of standby and commercial letters of

credit. The credit agreement also provides for an increase in the credit facility commitments up to an additional $500.0

million, at the option of the lenders and subject to the satisfaction of certain conditions. The restrictive covenants of the

credit agreement limit Safeway with respect to, among other things, creating liens upon its assets and disposing of

material amounts of assets other than in the ordinary course of business. Additionally, the Company is required to

maintain a minimum Adjusted EBITDA, as defined in the credit agreement, to interest expense ratio of 2.0 to 1 and is

required to not exceed an Adjusted Debt (total consolidated debt less cash and cash equivalents in excess of $75.0

million) to Adjusted EBITDA ratio of 3.5 to 1. As of December 31, 2011, the Company was in compliance with these

covenant requirements. As of December 31, 2011, there were $39.5 million in borrowings, and letters of credit totaled

$43.5 million under the Credit Agreement. Total unused borrowing capacity under the credit agreement was $1,417.0

million as of December 31, 2011.

49