Sprint - Nextel 2014 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2014 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

|

|

Table of Contents

Index to Consolidated Financial Statements

CLEARWIRE CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS —(CONTINUED)

F-95

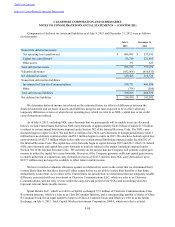

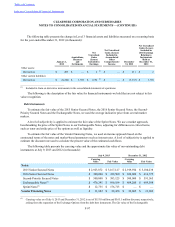

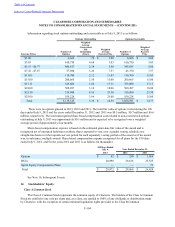

10. Derivative Instruments

The holders’ exchange rights contained in the Exchangeable Notes constitute embedded derivative instruments

that are required to be accounted for separately from the debt host instrument at fair value. As a result, upon the

issuance of the Exchangeable Notes, we recognized Exchange Options, with an estimated fair value of $231.5

million as a derivative liability. As a result of the Exchange Transaction, $100.0 million in par value of the

Exchangeable Notes were retired and the related Exchange Options, with a notional amount of 14.1 million shares,

were settled at fair value. The Exchange Options are indexed to Class A Common Stock, have a notional amount of

88.9 million shares at July 9, 2013 and December 31, 2012 and mature in 2040.

We do not apply hedge accounting to the Exchange Options. Therefore, gains and losses due to changes in fair

value are reported in our consolidated statements of operations. At July 9, 2013, the Exchange Options' estimated

fair value was $0. At December 31, 2012, the Exchange Options’ estimated fair value of $5.3 million was reported

in Other current liabilities on our consolidated balance sheets. For the 190 days ended July 9, 2013 and the years

ended December 31, 2012 and 2011, we recognized gains of $5.3 million, $1.4 million and $159.7 million,

respectively, from the changes in the estimated fair value in Gains on derivative instruments in our consolidated

statements of operations. See Note 11, Fair Value, for information regarding valuation of the Exchange Options.

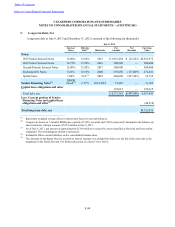

11. Fair Value

The following is a description of the valuation methodologies and pricing assumptions we used for financial

instruments measured and recorded at fair value on a recurring basis in our financial statements and the

classification of such instruments pursuant to the valuation hierarchy.

Cash Equivalents and Investments

Where quoted prices for identical securities are available in an active market, we use quoted market prices to

determine the fair value of investment securities and cash equivalents, and they are classified in Level 1 of the

valuation hierarchy. Level 1 securities include U.S. Government Treasury Bills, actively traded U.S. Government

Treasury Notes and money market mutual funds for which there are quoted prices in active markets or quoted net

asset values published by the money market mutual fund and supported in an active market.

Investments are classified in Level 2 of the valuation hierarchy for securities where quoted prices are available

for similar investments in active markets or for identical or similar investments in markets that are not active and we

use "consensus pricing" from independent external valuation sources. Level 2 securities include U.S. Government

Agency Discount Notes and U.S. Government Agency Notes.

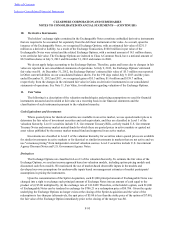

Derivatives

The Exchange Options are classified in Level 3 of the valuation hierarchy. To estimate the fair value of the

Exchange Options, we used an income approach based on valuation models, including option pricing models and

discounted cash flow models. We maximized the use of market-based observable inputs in the models and

developed our own assumptions for unobservable inputs based on management estimates of market participants’

assumptions in pricing the instruments.

Upon the consummation of the Sprint Acquisition, each $1,000 principal amount of Exchangeable Notes was

changed into a right to exchange such principal amount of Exchange Notes into an amount of cash equal to the

product of (i) $5.00 multiplied by (ii) the exchange rate of 141.2429. Therefore, at the holder's option, each $1,000

of Exchangeable Notes can be tendered in exchange for $706.21 or a redemption price of $0.706. Given the equity

underlying the Exchange Options no longer exists at the closing of the Sprint Acquisition and the value of the

redemption is less than par (alternatively, the spot price of $5.00 is less than the strike price of the option of $7.08),

the fair value of the Exchange Option immediately prior to the closing of the merger was $0.