Sprint - Nextel 2014 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2014 Sprint - Nextel annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

|

|

Table of Contents

57

$2.8 billion of borrowing capacity available under the revolving bank credit facility as of March 31, 2015. As of March 31,

2015, there is approximately $460 million of available funding under the Receivables Facility. In addition, after including

draws made in April 2015, we had available borrowing capacity of up to $574 million under our Finnvera secured equipment

credit facility and an aggregate $840 million under our K-sure and D/D secured equipment credit facilities. However,

utilization of these new facilities depends on the amount and timing of network-related equipment purchases from the

applicable suppliers as well as the timing of fund availability per tranche.

To meet our short- and long-term liquidity requirements, we look to a variety of funding sources. Our existing

liquidity balance and cash generated from operating activities is our primary source of funding. In addition to cash flows

from operating activities, we rely on the ability to issue debt and equity securities, the ability to issue other forms of

financing, proceeds from the sale of certain accounts receivable under the Receivables Facility and the borrowing capacity

available under our credit facilities to support our short- and long-term liquidity requirements. We believe our existing

available liquidity and cash flows from operations will be sufficient to meet our funding requirements through the next

twelve months, including debt service requirements and other significant future contractual obligations. To maintain an

adequate amount of available liquidity and execute according to the timeline of our current business plan, which includes

network deployment and maintenance, subscriber growth, data usage capacity needs and the expected achievement of a cost

structure intended to achieve more competitive margins, we may need to raise additional funds from external resources. If we

are unable to fund our remaining capital needs from external resources on terms acceptable to us, we would need to modify

our existing business plan, which could adversely affect our expectation of long-term benefits to results from operations and

cash flows from operations.

In determining our expectation of future funding needs in the next twelve months and beyond, we have made

several assumptions regarding:

• projected revenues and expenses relating to our operations;

• cash needs related to our installment billing and leasing programs;

• current availability of up to $1.4 billion in funding under the amended Receivables Facility, which terminates in

March 2017 unless extended;

• continued availability of a revolving bank credit facility, which expires in February 2018, in the amount of $3.3

billion, less any letters of credit;

• availability up to $1.4 billion of the new secured equipment credit facilities, all of which is available through

2018 for eligible capital expenditures, and any corresponding principal, interest and fee payments;

• the use of cash and cash equivalents in the near-term;

• anticipated levels and timing of capital expenditures, including the capacity and upgrading of our networks and

the deployment of new technologies in our networks, FCC license acquisitions, and purchases of leased devices

from our indirect dealers;

• any additional contributions we may make to our pension plan;

• any scheduled principal payments on debt, including approximately $12.5 billion coming due over the next five

fiscal years plus interest due on all outstanding debt; and

• other future contractual obligations and general corporate expenditures.

Our ability to fund our capital needs from external sources is ultimately affected by the overall capacity and terms

of the banking and securities markets, the availability of other financing alternatives, as well as our performance and our

credit ratings. Given our recent financial performance as well as the volatility in these markets, we continue to monitor them

closely and to take steps to maintain financial flexibility at a reasonable cost of capital.

The outlooks and credit ratings from Moody's Investor Service, Standard & Poor's Ratings Services, and Fitch

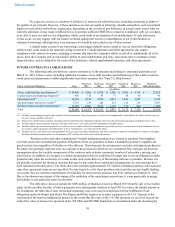

Ratings for certain of Sprint Corporation's outstanding obligations were:

Rating

Rating Agency Issuer

Rating Unsecured

Notes Guaranteed

Notes Bank Credit

Facility Outlook

Moody's B1 B2 Ba2 Ba1 Negative

Standard and Poor's B+ B+ BB BB Negative

Fitch B+ B+ BB BB Stable