Starbucks 2015 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2015 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

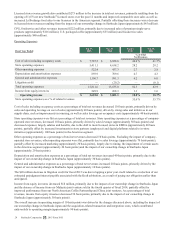

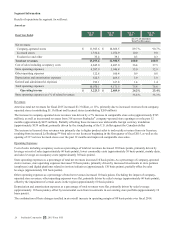

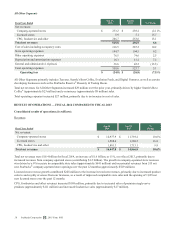

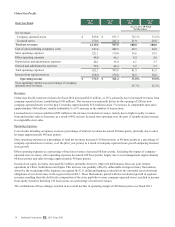

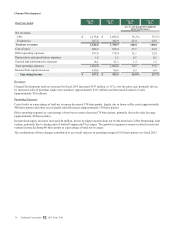

Depreciation and amortization expenses as a percentage of total revenues increased 220 basis points, primarily due to the

impact of our ownership change in Starbucks Japan (approximately 210 basis points).

General and administrative expenses as a percentage of total revenues decreased 20 basis points, primarily due to sales leverage

(approximately 40 basis points) and the impact of the sale of our Australia retail operations in the fourth quarter of fiscal 2014

(approximately 20 basis points), which includes lapping professional fees associated with the sale. The impact of our ownership

change in Starbucks Japan contributed unfavorably (approximately 60 basis points).

Income from equity investees decreased $44 million, primarily due to the impact of our ownership change in Starbucks Japan

and absence of income from our Malaysia joint venture sold in the fourth quarter of fiscal 2014, partially offset by improved

performance from our China joint venture. As a percentage of total net revenues, income from equity investees declined 950

basis points, primarily due to the impact of our ownership change in Starbucks Japan (approximately 870 basis points).

The overall decrease in operating margin of 1,210 basis points over fiscal 2014 was primarily driven by the impact of our

ownership change in Starbucks Japan (approximately 1,410 basis points), partially offset by 200 basis points of margin

expansion driven by the other items discussed above.

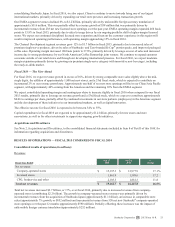

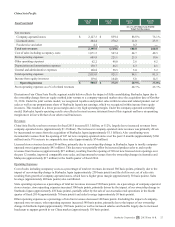

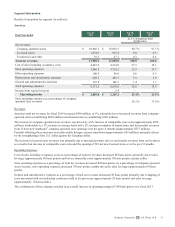

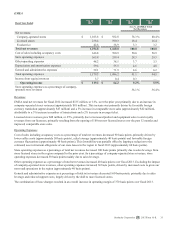

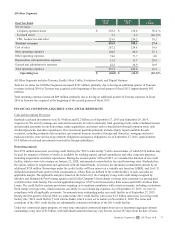

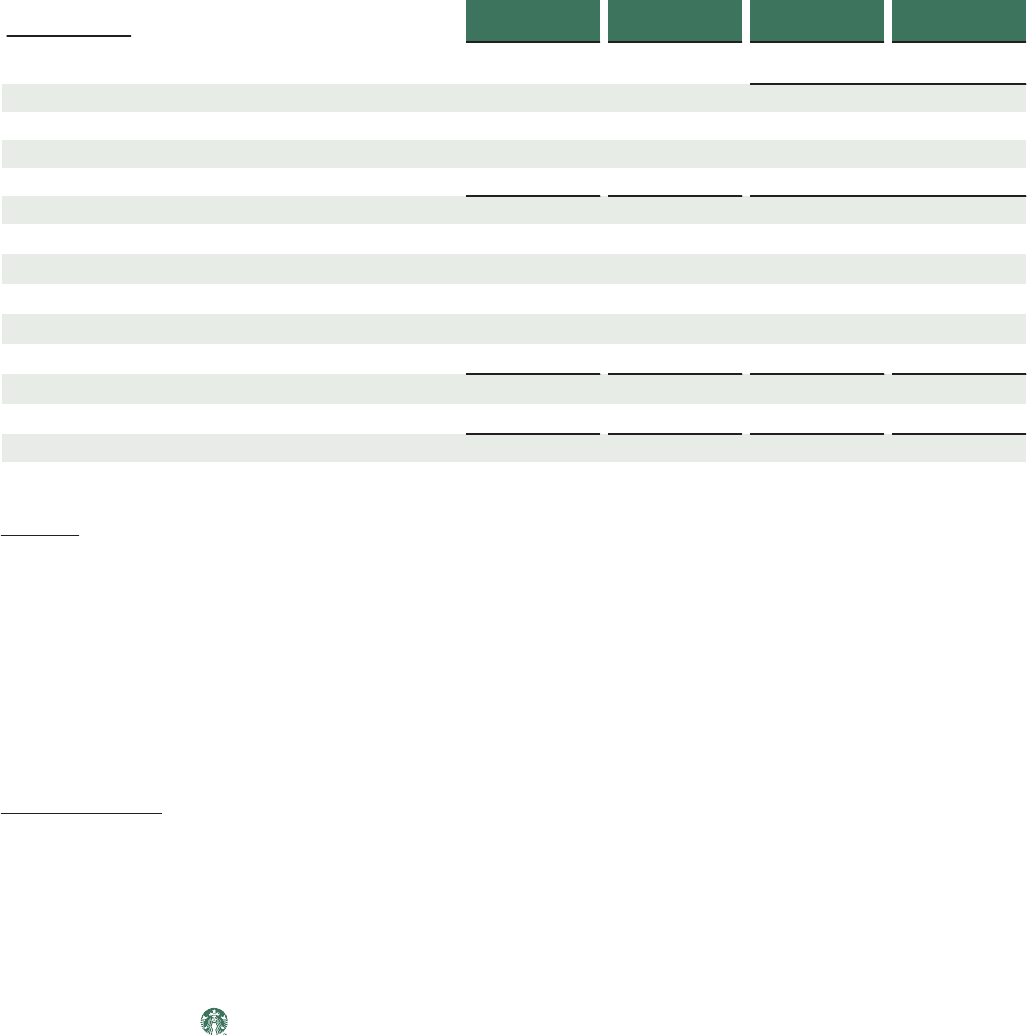

EMEA

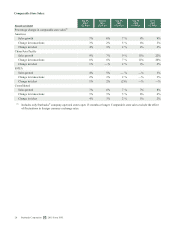

Fiscal Year Ended

Sep 27,

2015

Sep 28,

2014

Sep 27,

2015

Sep 28,

2014

As a % of EMEA

Total Net Revenues

Net revenues:

Company-operated stores $ 911.2 $ 1,013.8 74.9 % 78.3 %

Licensed stores 257.2 238.4 21.1 18.4

Foodservice 48.3 42.6 4.0 3.3

Total net revenues 1,216.7 1,294.8 100.0 100.0

Cost of sales including occupancy costs 582.5 646.8 47.9 50.0

Store operating expenses 308.7 365.8 25.4 28.3

Other operating expenses 51.8 48.2 4.3 3.7

Depreciation and amortization expenses 52.0 59.4 4.3 4.6

General and administrative expenses 56.6 59.1 4.7 4.6

Total operating expenses 1,051.6 1,179.3 86.4 91.1

Income from equity investees 3.1 3.7 0.3 0.3

Operating income $ 168.2 $ 119.2 13.8% 9.2%

Store operating expenses as a % of related revenues 33.9 % 36.1 %

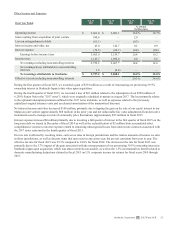

Revenues

EMEA total net revenues for fiscal 2015 decreased $78 million, or 6%. The decrease was primarily due to a decline in

company-operated store revenues (approximately $103 million), which was largely due to unfavorable foreign currency

translation (approximately $94 million). Also contributing to the decrease in company-operated revenues was the shift to more

licensed stores in the region, which includes net store closures as well as the absence of revenues from the conversion of certain

stores in the U.K. from company-operated to licensed. This decline was partially offset by 4% growth in comparable store

sales.

Licensed store revenues increased $19 million, or 8%, primarily due to higher product sales to and royalty revenues from our

licensees (approximately $45 million), resulting from the opening of 238 net new licensed stores over the past 12 months and

improved comparable store sales, partially offset by unfavorable foreign currency translation (approximately $22 million).

Operating Expenses

Cost of sales including occupancy costs as a percentage of total net revenues decreased 210 basis points, primarily due to

favorable foreign currency exchange (approximately 130 basis points). We buy and sell products, primarily roasted coffee, in

multiple currencies throughout the region depending on the functional currency of each market. Differences in those rates

generated favorable foreign currency exchange for fiscal 2015 resulting in a benefit in cost of sales. Sales leverage

(approximately 40 basis points) also contributed to the decrease.

28 Starbucks Corporation 2015 Form 10-K