Starbucks 2015 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2015 Starbucks annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

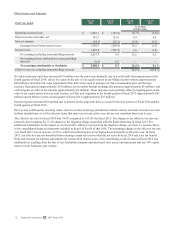

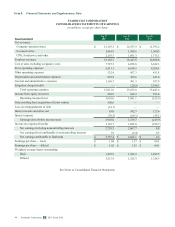

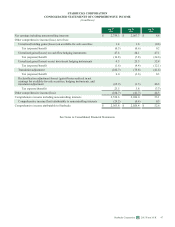

Interest Rate Risk

Long-term Debt

We utilize short-term and long-term financing and may use interest rate hedges to manage our overall interest expense related

to our existing fixed-rate debt, as well as to hedge the variability in cash flows due to changes in the benchmark interest rate

related to anticipated debt issuances. See Note 3, Derivative Financial Instruments and Note 9, Debt, to the consolidated

financial statements included in Item 8 of Part II of this 10-K for further discussion of our interest rate hedge agreements and

details of the components of our long-term debt, respectively, as of September 27, 2015.

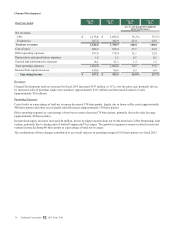

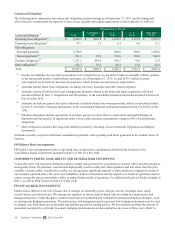

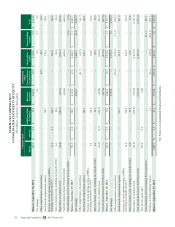

The following table summarizes the impact of a change in interest rates as of September 27, 2015 on the fair value of Starbucks

debt (in millions):

Change in Fair Value

Stated Interest

Rate Fair Value

100 Basis Point Increase in

Underlying Rate

100 Basis Point Decrease in

Underlying Rate

2016 notes 0.875% $ 400 $ (5) $ 5

2018 notes 2.000% $ 354 $ (11) $ 11

2022 notes 2.700% $ 503 $ (31) $ 31

2023 notes 3.850% $ 790 $ (54) $ 54

2045 notes 4.300% $ 355 $ (61) $ 61

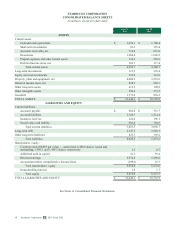

Available-for-Sale Securities

Our available-for-sale securities comprise a diversified portfolio consisting mainly of fixed-income instruments. The primary

objective of these investments is to preserve capital and liquidity. Available-for-sale securities are recorded on the consolidated

balance sheets at fair value with unrealized gains and losses reported as a component of accumulated other comprehensive

income. We do not hedge the interest rate exposure on our available-for-sale securities. We performed a sensitivity analysis

based on a 100 basis point change in the underlying interest rate of our available-for-sale securities as of September 27, 2015,

and determined that such a change would not have a significant impact on the fair value of these instruments.

APPLICATION OF CRITICAL ACCOUNTING POLICIES

Critical accounting policies are those that management believes are both most important to the portrayal of our financial

condition and results and require the most difficult, subjective or complex judgments, often as a result of the need to make

estimates about the effect of matters that are inherently uncertain. Judgments and uncertainties affecting the application of those

policies may result in materially different amounts being reported under different conditions or using different assumptions.

Our significant accounting policies are discussed in Note 1, Summary of Significant Accounting Policies, to the consolidated

financial statements included in Item 8 of Part II of this 10-K. We believe that of our significant accounting policies, the

following policies involve a higher degree of judgment and/or complexity.

We consider financial reporting and disclosure practices and accounting policies quarterly to ensure that they provide accurate

and transparent information relative to the current economic and business environment. During the past three fiscal years, we

have not made any material changes to the accounting methodologies used to assess the areas discussed below, unless noted

otherwise.

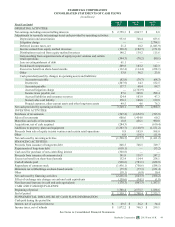

Property, Plant and Equipment and Other Finite-Lived Assets

We evaluate property, plant and equipment and other finite-lived assets for impairment when facts and circumstances indicate

that the carrying values of such assets may not be recoverable. When evaluating for impairment, we first compare the carrying

value of the asset to the asset’s estimated future undiscounted cash flows. If the estimated undiscounted future cash flows are

less than the carrying value of the asset, we determine if we have an impairment loss by comparing the carrying value of the

asset to the asset's estimated fair value and recognize an impairment charge when the asset’s carrying value exceeds its

estimated fair value. The adjusted carrying amount of the asset becomes its new cost basis and is depreciated over the asset's

remaining useful life.

Long-lived assets are grouped with other assets and liabilities at the lowest level for which identifiable cash flows are largely

independent of the cash flows of other assets and liabilities. For company-operated store assets, the impairment test is

performed at the individual store asset group level. The fair value of a store’s assets is estimated using a discounted cash flow

model. For other long-lived assets, fair value is determined using an approach that is appropriate based on the relevant facts and

circumstances, which may include discounted cash flows, comparable transactions, or comparable company analyses.

42 Starbucks Corporation 2015 Form 10-K