Target 2004 Annual Report Download - page 19

Download and view the complete annual report

Please find page 19 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

1717

Executive Summary

Target Corporation operates large-format general merchandise

discount stores in the United States and a much smaller, rapidly

growing on-line business. We drive incremental merchandise sales

and profitability through increases in our comparable-store sales and

through contributions from new stores. Additionally, our credit card

operations represent an integral component of our retail business.

We focus on delighting our guests by offering both everyday essentials

and fashionable, differentiated merchandise at exceptional prices.

Our ability to deliver a shopping experience that is preferred by our

guests is supported by our strong supply chain and technology

network, a devotion to innovation which is ingrained in our organization

and culture, and our disciplined approach to managing our current

business and investing in future growth. Although our industry is highly

competitive and subject to macro-economic conditions, we believe

we are well-positioned to deliver continued profitable market share

growth for many years to come.

In 2004, we completed the disposition of two segments of our

business, Marshall Field’s and Mervyn’s, and recorded a total gain on

the sale of $1,999 million ($1.36 per share). As a result, our current

and prior year financial statements have been restated to reflect the

results of these businesses as discontinued operations. See Notes to

Consolidated Financial Statements on page 29. Also during 2004, we

elected to adopt the provisions of Statement of Financial Accounting

Standards No.123R, “Share-Based Payment” (SFAS No.123R) under

the modified retrospective transition method. All prior period financial

statements have been restated to recognize compensation cost in the

amounts previously reported in the Notes to Consolidated Financial

Statements under the provisions of SFAS No. 123, “Accounting for

Stock-Based Compensation.”

Management’s Discussion and Analysis is based on our

Consolidated Financial Statements as shown on pages 24-27.

Analysis of Continuing Operations

Revenues and Comparable-store Sales

Sales include merchandise sales, net of expected returns, from our

stores and our on-line business. Total revenues include sales and net

credit card revenues. Net credit card revenues represent income

derived from finance charges, late fees and other revenues from use

of our Target Visa and proprietary Target Card. Comparable-store

sales are sales from stores open longer than one year, including stores

that were moved to a new location or remodeled as a general mer-

chandise store. General merchandise stores that are converted to a

SuperTarget store format are removed from the comparable-store

sales calculation until they are open longer than one year. Sales from

our on-line business are not included in comparable store sales.

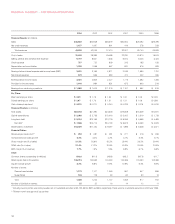

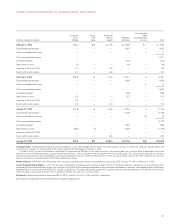

Factors Affecting Revenue Growth

2004 2003 2002

Sales growth 11.6% 12.1% 12.0%

Net credit card revenue growth 5.5% 23.2% 112.6%

Total revenue growth 11.5% 12.3% 13.3%

Estimated impact of deflation on sales (1.4%) (4.2%) (3.8%)

The revenue increases in both 2004 and 2003 were driven by

new store expansion, growth in comparable-store sales and increases

in net credit revenues. In 2005, we expect these same factors to con-

tribute to a low double digit percentage increase in revenues. Inflation/

deflation is not expected to have a significant effect on sales growth.

Gross Margin Rate

Gross margin rate represents gross margin (sales less cost of sales)

as a percent of sales. Cost of sales primarily include purchases, mark-

downs, shortage, and other costs associated with our merchandise.

These costs are partially offset by various forms of consideration

earned from our vendors, which we refer to as “vendor income.” Refer

to the Critical Accounting Estimates section on page 21 for further

discussion of retail inventory accounting and vendor income.

In 2004, our consolidated gross margin rate increased 0.6

percentage points to a rate of 31.2 percent primarily due to an increase

in markup. We have continued to lower our product costs through

strategic sourcing initiatives such as increasing our direct import

penetration.

In 2003, our consolidated gross margin rate increased by 0.4

percentage points to a rate of 30.6 percent. The growth was attrib-

utable to the adoption of Emerging Issues Task Force (EITF) Issue

No. 02-16 “Accounting by a Customer (Including a Reseller) for Certain

Consideration Received from a Vendor.” The adoption resulted in a

reclassification of a portion of our vendor income from selling, general

and administrative expenses to cost of sales and had a slight nega-

tive impact on net earnings. See further discussions in the Notes to

Consolidated Financial Statements on page 28.

Consolidated gross margin rate in 2005 is expected to be

approximately equal to or slightly greater than 2004.

Selling, General and Administrative Expense Rate

Our selling, general and administrative (SG&A) expense rate represents

payroll, benefits, advertising, distribution, buying and occupancy,

start-up and other expenses as a percentage of sales. SG&A expense

excludes depreciation and amortization and expenses associated

with our credit card operations, which are reflected separately in our

Consolidated Results of Operations. In 2004 and 2003 approximately

$72 million and $58 million, respectively, of vendor income was recorded

as an offset to SG&A expenses as it met the specific, incremental and

identifiable criteria of EITF No. 02-16. In 2002, approximately $195

million of vendor income was recorded as an offset to SG&A expenses.

This vendor income primarily represented advertising reimbursements.

MANAGEMENT’S DISCUSSION AND ANALYSIS