Target 2004 Annual Report Download - page 37

Download and view the complete annual report

Please find page 37 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44

|

|

35

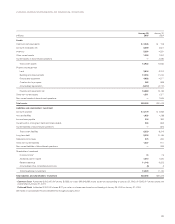

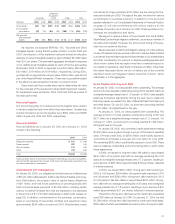

Pension and Postretirement Health Care Benefits

We have a qualified defined benefit pension plan that covers all U.S.

employees who meet certain age, length of service and hours worked

per year requirements. We also have unfunded non-qualified pension

plans for employees who have qualified plan compensation restric-

tions. Benefits are provided based upon years of service and the

employee’s compensation. Retired employees also become eligible

for certain health care benefits if they meet minimum age and service

requirements and agree to contribute a portion of the cost. Prior to

the end of 2004, but after the measurement date, we merged our

three qualified U.S. pension plans into one plan. The expected impact

of this merger on future accounting results is immaterial.

The Medicare Prescription Drug, Improvements and Modernization

Act of 2003 (the Act) was signed into law in December 2003. As a

result of the Act we recorded a reduction in our accumulated post-

retirement benefit obligation of $7 million in 2004. In addition, the

expense amounts shown in the table below reflect a $1 million reduc-

tion due to the amortization of the actuarial gain and reduction in

interest cost due to the effects of the Act.

Obligations and Funded Status at October 31, 2004

Pension Benefits Postretirement

Non-qualified Health Care

Qualified Plans Plans Benefits

(millions) 2004 2003 2004 2003 2004 2003

Change in Benefit

Obligation

Benefit obligation

at beginning of

measurement period $1,333 $1,078 $29 $23 $123 $116

Service cost 78 73 1132

Interest cost 82 74 2278

Actuarial loss 68 164 46(6) 7

Benefits paid (65) (56) (3) (3) (13) (10)

Plan amendments 19 —1—(7) —

Settlement ——————

Benefit obligation

at end of

measurement period $1,515 $1,333 $34 $29 $107 $123

Change in Plan Assets

Fair value of plan assets

at beginning of

measurement period $1,405 $1,058 $— $— $ — $ —

Actual return on

plan assets 157 203 ————

Employer contribution 201 200 3313 10

Benefits paid (65) (56) (3) (3) (13) (10)

Fair value of plan

assets at end of

measurement period $1,698 $1,405 $— $— $ — $ —

Funded status $183$72 $(34) $(29) $(107) $(123)

Unrecognized

actuarial loss 584 587 15 12 612

Unrecognized prior

service cost (39) (65) 23—1

Net amount recognized $ 728 $ 594 $(17) $(14) $(101) $(110)

Amounts recognized in the Statements of Financial Position

consist of:

Pension Benefits Postretirement

Non-qualified Health Care

Qualified Plans Plans Benefits

(millions) 2004 2003 2004 2003 2004 2003

Prepaid benefit cost $733 $600 $— $— $ — $ —

Accrued benefit cost (11) (6) (24) (20) (101) (110)

Intangible assets ——23n/a n/a

Accumulated OCI 6—53n/a n/a

Net amount recognized $728 $594 $(17) $(14) $(101) $(110)

The accumulated benefit obligation for all defined benefit pension

plans was $1,501 million and $1,237 million at October 31, 2004 and

2003, respectively. The projected benefit obligation, accumulated

benefit obligation and fair value of plan assets for the pension plans

with an accumulated benefit obligation in excess of plan assets were

$49 million, $45 million and $5 million, respectively, as of October 31,

2004 and $34 million, $30 million and $1 million, respectively, as of

October 31, 2003.

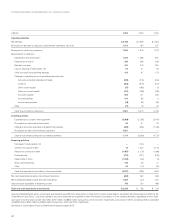

Net Pension and Postretirement Health Care Benefits Expense

Postretirement

Pension Benefits Health Care Benefits

(millions) 2004 2003 2002 2004 2003 2002

Service cost benefits

earned during

the period $ 79 $ 74 $ 58 $3 $2 $2

Interest cost on

projected benefit

obligation 84 75 75 788

Expected return

on assets (122) (114) (108) ———

Recognized losses 36 18 10 111

Recognized prior

service cost (7) (7) 1 ———

Settlement/curtailment

charges 1— (12) (7) ——

Tot al $ 71 $ 46 $ 24 $ 4 $11 $11

The amortization of any prior service cost is determined using a

straight-line amortization of the cost over the average remaining service

period of employees expected to receive benefits under the plan.

Curtailment gains recorded in 2004 were a result of the sale of Marshall

Field’s and Mervyn’s. These curtailment gains are included in the gain

on disposal of discontinued operations as a result of freezing the

benefits for Marshall Field’s and Mervyn’s employees and retaining the

related assets and obligations of the plans.