Target 2004 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

|

|

29

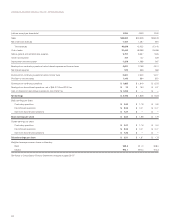

Advertising Costs

Advertising costs, included in selling, general and administrative

expense, are expensed at first showing of the advertisement and

were $888 million, $872 million and $666 million for 2004, 2003 and

2002, respectively. Advertising vendor income used to reduce

advertising expenses was approximately $72 million, $58 million and

$173 million for 2004, 2003 and 2002, respectively. Television and

radio broadcast and newspaper circulars make up the majority of our

advertising costs in all three years.

Discontinued Operations

On March 10, 2004, we began a review of strategic alternatives for

our Marshall Field’s and Mervyn’s businesses, which included but was

not limited to the possible sale of one or both as ongoing businesses

to existing retailers or other qualified buyers.

On June 9, 2004, we agreed to sell Marshall Field’s and the

Mervyn’s stores located in Minnesota to The May Department Store

Company (May). We completed the sale of Marshall Field’s on July 31,

2004 and the sale of the Minnesota Mervyn’s stores on August 24,

2004. May acquired total assets and liabilities with a net carrying value

of $1,563 million in exchange for $3,240 million cash consideration,

resulting in a gain on the sale of $1,677 million or $1.14 per share.

On July 29, 2004, we agreed to sell the remaining Mervyn’s retail

stores and distribution centers to an investment consortium including

Sun Capital Partners, Inc., Cerberus Capital Management, L.P., and

Lubert-Adler/Klaff and Partners, L.P. and to sell Mervyn’s credit card

receivables to GE Consumer Finance, a unit of General Electric

Company, for total cash consideration of $1,641 million. This sale

transaction was completed as of August 28, 2004, resulting in a gain

of $322 million or $.22 per share.

In accordance with SFAS No.144, “Accounting for the Impairment

or Disposal of Long-Lived Assets,” the financial results of Marshall

Field’s and Mervyn’s are reported as discontinued operations for all

periods presented.

In connection with the sale of Marshall Field’s, May is purchasing

transition support services from us until the end of first quarter 2005.

We are providing transition services to the buyer of Mervyn’s for a fee

until the earlier of August 2007 or the date on which an alternative

long-term solution for providing these services is in place. The fees

received for providing these services exceed our marginal costs, but

when an allocable share of our fixed costs is included, the consider-

ation received is essentially equal to our total costs.

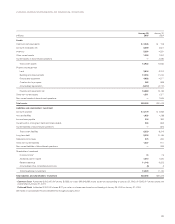

The financial results included in discontinued operations were

as follows:

January 29, January 31, February 1,

(millions) 2005 2004 2003

Revenue $3,095 $6,138 $6,507

Earnings from discontinued

operations before income taxes 121 306 399

Earnings from discontinued operations,

net of $46, $116 and $152 tax,

respectively 75 190 247

Gain on sale of discontinued operations,

net of $761 tax 1,238 ——

Total income from discontinued

operations, net of tax $1,313 $ 190 $ 247

There were no assets or liabilities of Marshall Field’s or Mervyn’s

included in our Consolidated Statements of Financial Position at

January 29, 2005. The major classes of assets and liabilities of

discontinued operations in the Consolidated Statements of Financial

Position on January 31, 2004 were as follows:

January 31,

(millions) 2004

Cash and cash equivalents $8

Accounts receivable, net 1,155

Inventory 812

Other 117

Current assets of discontinued operations $2,092

Property and equipment, net $1,816

Other 118

Non-current assets of discontinued operations $1,934

Accounts payable $ 492

Accrued liabilities 330

Current portion of long-term debt and notes payable 3

Current liabilities of discontinued operations $ 825

Long-term debt $62

Deferred income taxes —

Other 204

Non-current liabilities of discontinued operations $ 266

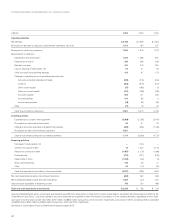

Earnings per Share

Basic earnings per share (EPS) is net earnings divided by the average

number of common shares outstanding during the period. Diluted

EPS includes the incremental shares that are assumed to be issued

on the exercise of stock options.

Basic EPS Diluted EPS

(millions, except

per share data) 2004 2003 2002 2004 2003 2002

Net earnings $3,198 $1,809 $1,623 $3,198 $1,809 $1,623

Basic weighted

average

common shares

outstanding 903.8 911.0 908.0 903.8 911.0 908.0

Stock options ———8.3 8.2 6.3

Weighted average

common shares

outstanding 903.8 911.0 908.0 912.1 919.2 914.3

Earnings per share $ 3.54 $ 1.99 $ 1.79 $3.51 $ 1.97 $ 1.78

The shares related to stock options shown above do not include shares issuable

upon exercise of approximately 4.5 million and 13.2 million at January 31, 2004 and

February 1, 2003, respectively, because the effect would have been antidilutive.

There were no antidilutive shares issuable upon exercise at January 29, 2005.

Other Comprehensive Income

Other comprehensive income includes revenues, expenses, gains

and losses that are excluded from net earnings under GAAP. In 2004

and 2003, other comprehensive income primarily included gains and

losses on certain hedge transactions and the change in our minimum

pension liability, net of related taxes.