Target 2004 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

21

Market Risk

Our exposure to market risk results primarily from changes in interest

rates on our debt obligations, as well as the effect of market returns

on our non-qualified defined contribution and qualified defined benefit

pension plans. We hold derivative instruments primarily to manage

our exposure to these risks, and all derivative instruments are matched

against specific debt obligations or other liabilities. There have been

no material changes in the primary risk exposures or management

of the risks since the prior year. See further discussions in the Notes

to Consolidated Financial Statements on pages 31-36.

The annualized effect of a one percentage point increase in

floating interest rates on our interest rate swap agreements and other

floating-rate debt obligations, net of floating-rate cash equivalents,

at January 29, 2005 would be to increase interest expense by

approximately $19 million. The annualized effect of a one percentage

point change in equity market returns on our non-qualified defined

contribution plans (inclusive of the effect of derivative instruments

used to hedge or manage these exposures) would not be significant.

The annualized effect of a one percentage point decrease in the

return on pension plan assets would be to decrease plan assets by

$17 million. The resulting impact on net pension expense would be

determined consistent with the provisions of SFAS No. 87, “Employers’

Accounting for Pensions.” In 2005, the majority of our credit card

receivables will be assessed finance charges at a prime-based floating

rate instead of a fixed rate. The impact of this change to our revenue

will be determined by future changes in the prime rate. In order to

protect our credit card economics in light of future changes in the

prime rate, we plan to maintain a sufficient level of floating-rate debt

to achieve parallel changes in our finance charge revenue and

interest expense.

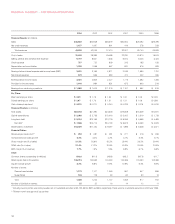

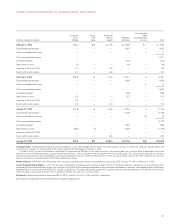

Analysis of Discontinued Operations

In 2004, revenues and earnings from discontinued operations were

lower than prior years due to only a partial year of results, which

excluded the holiday season.

The financial results included in discontinued operations were

as follows:

January 29, January 31, February 1,

(millions) 2005 2004 2003

Revenue $3,095 $6,138 $6,507

Earnings from discontinued

operations before income taxes 121 306 399

Earnings from discontinued operations,

net of $46, $116 and $152 tax,

respectively 75 190 247

Gain on sale of discontinued operations,

net of $761 tax 1,238 ——

Total income from discontinued

operations, net of tax $1,313 $ 190 $ 247

Critical Accounting Estimates

Our analysis of operations and financial condition is based upon our

consolidated financial statements, which have been prepared in

accordance with accounting principles generally accepted in the

United States. The preparation of these financial statements requires

us to make estimates and assumptions that affect the reported

amounts of assets and liabilities at the date of the financial statements,

the reported amounts of revenues and expenses during the reporting

period and the related disclosures of contingent assets and liabilities.

In the Notes to Consolidated Financial Statements, we describe our

significant accounting policies used in preparation of the consolidated

financial statements. We evaluate our estimates on an ongoing basis.

We base our estimates on historical experience and on other assump-

tions that we believe to be reasonable under the circumstances.

Actual results could differ from these estimates under different

assumptions or conditions.

The following items in our consolidated financial statements

require significant estimation or judgment:

Inventory and cost of sales We account for substantially all of our

inventory and the related cost of sales under the retail inventory

method. Under the retail inventory method, inventory is stated at cost,

which is determined by applying a cost-to-retail ratio to each mer-

chandise grouping’s ending retail value. Since this inventory value

is adjusted regularly to reflect market conditions, our inventory

methodology reflects the lower of cost or market. We reduce inventory

for estimated losses related to shortage and markdowns. Shortage

is based upon historical losses verified by prior physical inventory

counts. Markdowns designated for clearance activity are recorded

when the salability of the merchandise has diminished. Inventory is

at risk of obsolescence if economic conditions change, such as

shifting consumer demand, changing consumer credit markets, or

increasing competition. These risks are mitigated because substantially

all of our inventory sells in less than six months. Inventory is described

in the Notes to Consolidated Financial Statements on page 30.

Vendor income receivable Cost of sales is partially offset by various

forms of consideration earned from our vendors. We receive income for

a variety of vendor-sponsored programs such as volume rebates,

markdown allowances, promotions and advertising, and for our com-

pliance programs. We establish a receivable for the vendor income

that is earned but not yet received from our vendors. This receivable is

based on provisions of the programs in place, and is computed by

estimating the point at which we’ve completed our performance under

the agreement and the amount is earned. Due to the complexity and

diversity of the individual agreements with vendors, we perform detailed

analyses and review historical trends to determine an appropriate level

of the receivable in aggregate. See further discussions in the Notes to

Consolidated Financial Statements on page 28.