Target 2004 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2004 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

|

|

1919

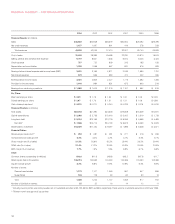

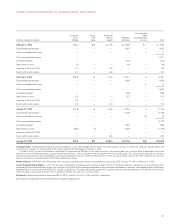

Net Interest Expense

In 2004, net interest expense was $570 million, $14 million higher

than 2003. This increase was due to a $74 million higher loss on debt

called or repurchased and a higher average portfolio interest rate

resulting from the unfavorable mix effect of higher balances of short-

term investments and higher market rates. This increase was partially

offset by significantly lower average debt, net of investments, due to

cash received from the dispositions of Marshall Field’s and Mervyn’s.

The average portfolio interest rate was 5.5 percent in 2004 and 4.9

percent in 2003. The $542 million of debt called or repurchased during

2004 resulted in a loss of $89 million (approximately $.06 per share)

and had an average interest rate of 7.0 percent and an average

remaining life of 24 years.

In 2003, net interest expense was $556 million, $28 million lower

than 2002. The decrease was due to a lower average portfolio interest

rate and a smaller loss on debt called or repurchased, partially offset

by higher average debt outstanding. The average portfolio interest rate

in 2003 was 4.9 percent compared with 5.6 percent in 2002. The

$297 million of debt called or repurchased during 2003 resulted in a

loss of $15 million (approximately $.01 per share) and had an average

interest rate of 7.8 percent and an average remaining life of 20 years.

Excluding any effect of future debt repurchases, we expect net

interest expense in 2005 to be lower than 2004 due to lower loss on

debt repurchase and lower average net debt balances in the first half

of the year. Additionally, the majority of our credit card receivables will

be assessed finance charges at a prime-based floating rate instead

of a fixed rate in 2005. In order to protect our credit card economics in

light of future changes in the prime rate, we plan to maintain a sufficient

level of floating-rate debt to achieve parallel changes in our finance

charge revenue and interest expense.

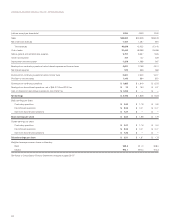

Analysis of Financial Condition

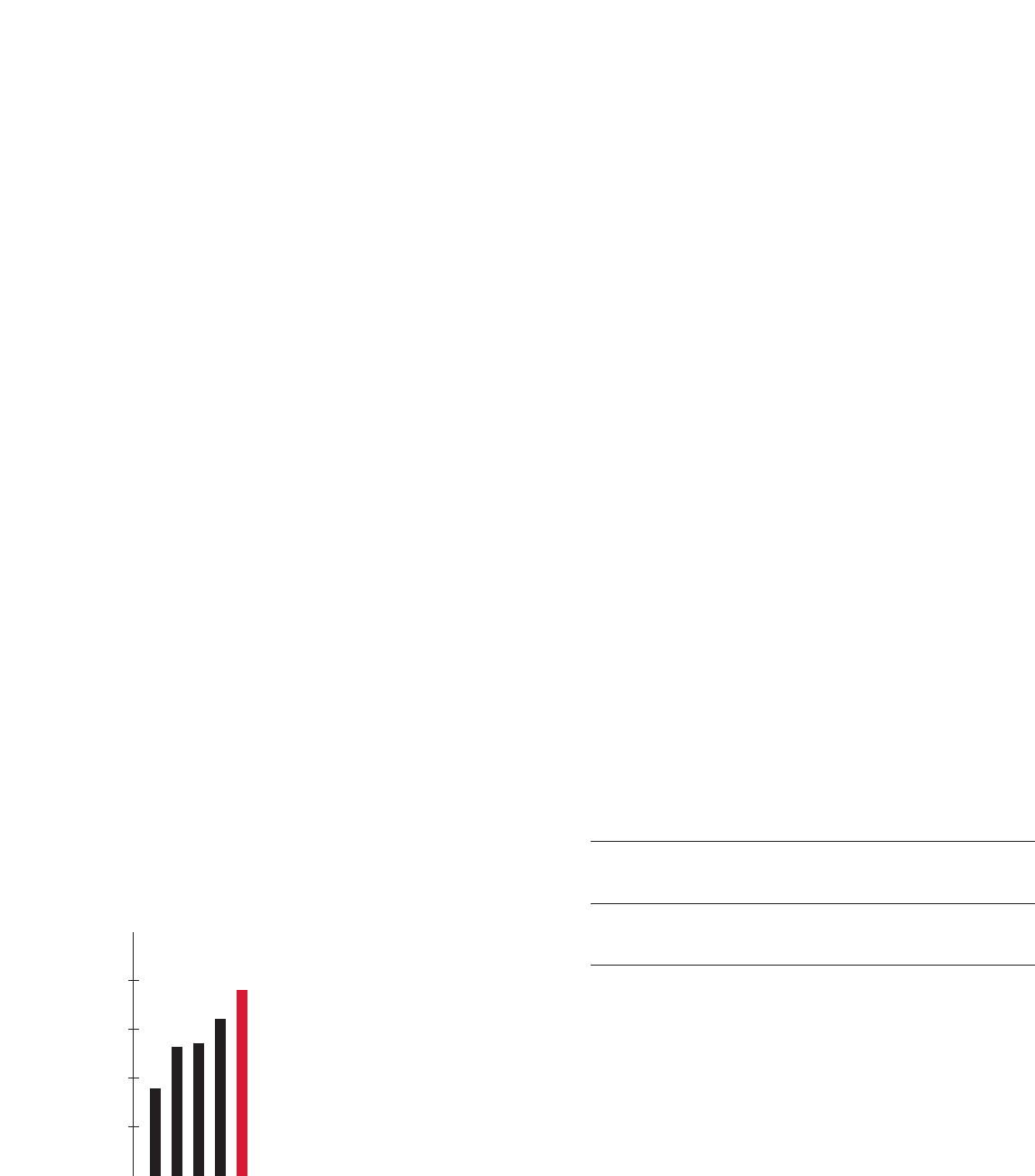

Liquidity and Capital Resources

Our financial condition remains strong.

In assessing our financial condition, we

consider factors such as cash flows

provided or used by operations, capital

expenditures and debt service obliga-

tions. Cash flow provided by operations

increased to $3,821 million in 2004 from

$3,213 million in 2003, primarily due to

higher net income. During 2004, cash

provided from the divestiture of Marshall

Field’s and Mervyn’s (before consider-

ation of associated taxes) was $4,881

million.

Our year-end receivables (before allowance) increased 9.7

percent, or $483 million, to $5,456 million. The growth in year-end

receivables was driven by growth in issuance and usage of the Target

Visa credit card during 2004. Average receivables in 2004 increased

5.7 percent.

Year-end inventory levels increased $853 million, or 18.8 percent.

The increase in inventory was a result of additional square footage and

same store sales growth, as well as the refinement of our measure-

ment of the point in our supply chain at which effective ownership of

direct imports occurs. This growth was primarily funded by an $823

million increase in accounts payable over the same period.

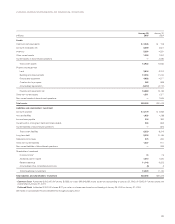

In June 2004, our Board of Directors authorized the repurchase

of $3 billion of our common stock which we expect to complete over

two to three years. This authorization replaced our previous repurchase

programs that were authorized by our Board of Directors in January

1999 and March 2000. During 2004, we repurchased 29 million shares

at a total cost of $1,290 million ($44.68 per share).

Our financing strategy is to ensure liquidity and access to capital

markets, to manage our net exposure to floating rates and to maintain

a balanced spectrum of debt maturities. Within these parameters,

we seek to minimize our cost of borrowing.

Management believes that cash flows from operations, together

with current levels of cash equivalents, proceeds from long-term

financing activities and issuance of short-term debt will be sufficient to

fund capital expenditures, share repurchases, growth in receivables,

maturities of long-term debt, and other cash requirements, including

seasonal buildup in inventories.

A key to our liquidity and access to capital markets is maintaining

strong investment-grade debt ratings.

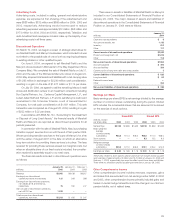

Credit Ratings

Standard

Moody’s and Poor’s Fitch

Long-term debt A2 A+ A+

Commercial paper P-1 A-1 F1

Securitized receivables Aaa AAA n/a

Further liquidity is provided by $1,600 million of committed lines

of credit obtained through a group of 25 banks. Of these credit lines,

an $800 million credit facility expires in June 2005 and includes a one-

year term-out option to June 2006. The remaining $800 million credit

facility expires in June 2008. There were no balances outstanding at

any time during 2004 or 2003 under these agreements. These com-

mitted credit lines, as well as most of our long-term debt obligations,

contain certain financial covenants. We are, and expect to remain,

in compliance within these covenants. No material debt instrument

contains provisions requiring acceleration of payment upon a debt

rating downgrade.

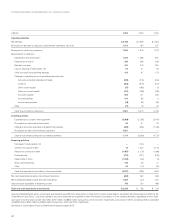

’00 ’01 ’02 ’03 ’04

$1,789

$2,657

$2,725

$3,213

$3,821

4,000

3,000

2,000

1,000

Cash Flow

from Operations

(millions)